42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

“Aberrative Silliness” – Stocks Are Dismissing Fed Hawkishness, Hoping For Next Round Of QE

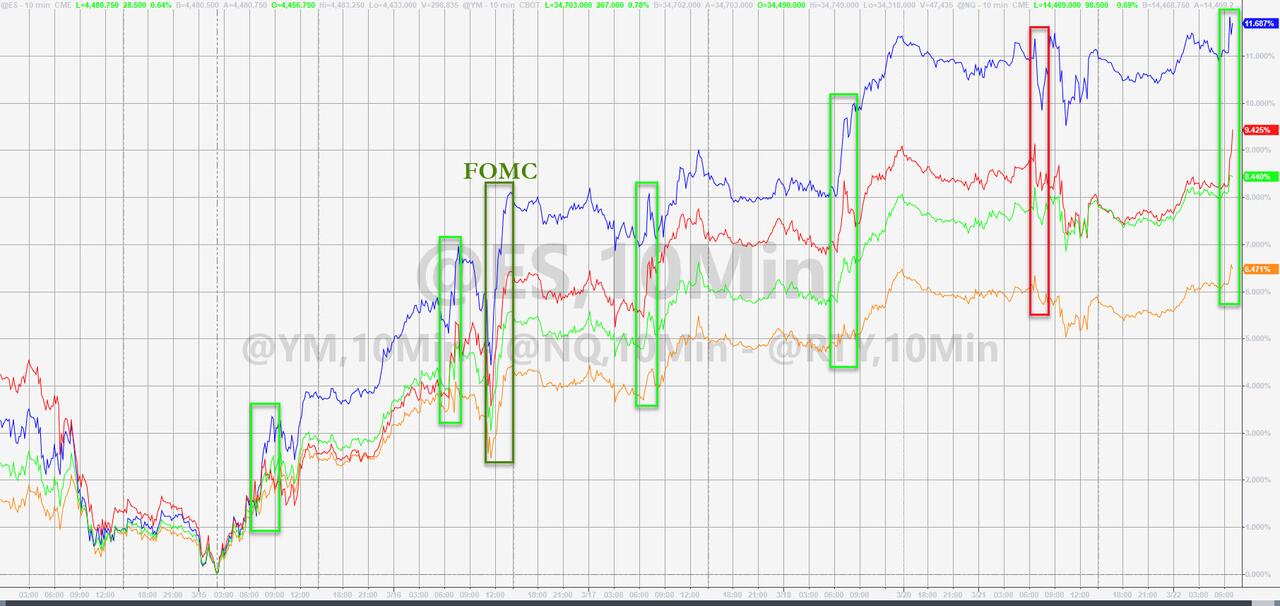

US equity markets are up 5 of the last 6 days, with Nasdaq soaring 12% off the lows from last Tuesday…

{kind=link}

The US cash opening has been a catalyst for panic-buying most of those days as traders unwind the massive negative-delta hedges that had been placed ahead of The Fed’s rate-hike and into last Friday’s sizable options expiration.

Even after yesterday’s post-OpEx ‘gamma unclenching’ and Powell’s notably hawkish comments, stocks (S&P) managed to scramble back to unchanged, apparently shrugging off the front-loaded tightening to come and ignoring Powell’s Volcker-esque warnings that The Fed will do ‘whatever it takes’ to quell inflation?

So what is going on?

The Fed is wrongly interpreting equity strength as ‘support’ for its aggressive tightening plan – when in fact it is just more negative-delta unwinds – and is thus emboldened to do more, sooner. As Goldman noted earlier, the recent shift in wording from “steadily” in January to“expeditiously” today is a signal that a 50bp rate hike is coming. And not just one but two, because according to Goldman, the Fed will raise interest rates by 50 basis points at both its May and June policy meetings, and by 25 basis points in the four remaining meetings in the second half of the year

As Rabobank’s Michael Every succinctly notes, “stocks are generally holding up on the view that this hawkishness is aberrative silliness that will soon give way to the usual QE and money on a plate for those who never have to worry about what’s on their plate, even as hundreds of millions literally risk having nothing on theirs.”

But you can’t have it both ways – rallying on easing and rallying on tightening.

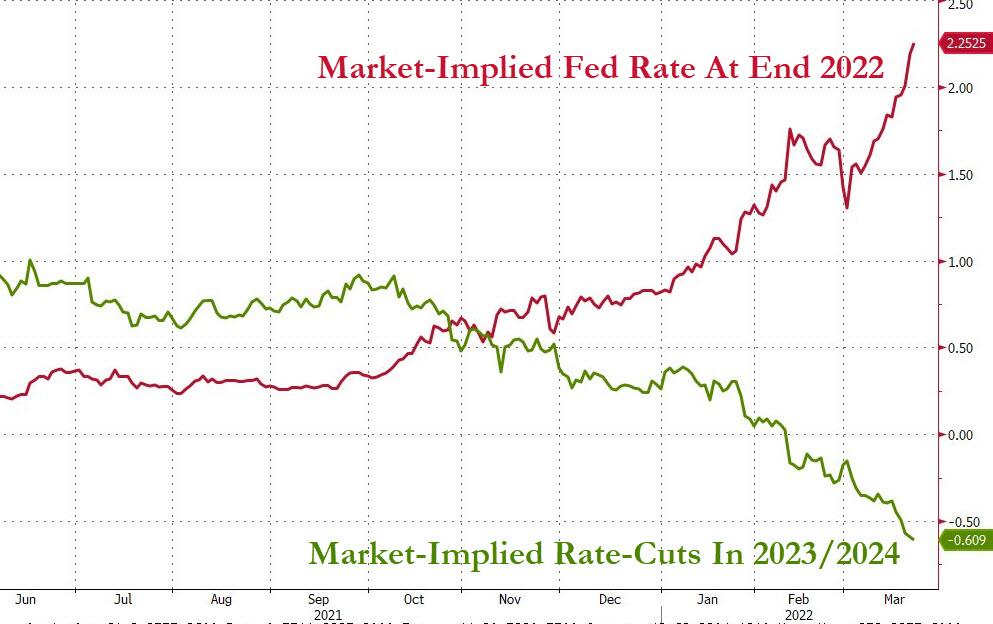

As an increasingly aggressive Fed rate-hike trajectory is priced into markets, so is an increasingly aggressive U-turn to easing and rate-cuts priced in for next year (with over 2 rate-cuts now being forecast from June 2023 through the end of 2024).

{kind=link}

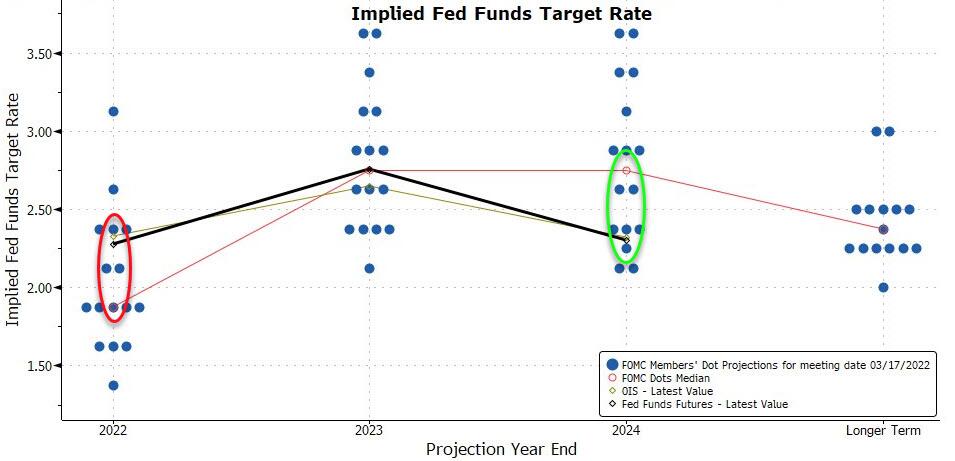

Simply put, traders are kidding themselves that – for the first time ever – The Fed will engineer a ‘soft landing’, even as we noted earlier, the bond market suggests that “the chance the Federal Reserve can engineer a soft landing is fading by the week, with the war in Ukraine exacerbating the inflationary pressures.”

So, as Nomura’s Charlie McElligott besides this next “acute” 1-3 month window of “peak” upside inflation data volatility risk, alongside this immediate post- Fed “front-loaded liftoff” period aligning as the Equities “peak drawdown window” (per our backtest shown multiple times), the REAL downside for Equities comes when the Fed STOPS hiking – because it confirms the slowdown / recession is imminent (coming to you in midyear / 2H ‘23!).

So the question is simple – what happens when the ‘negative-delta’ unwind is complete and reality sets in? Will the market ‘look through’ to what a shift to QE really means – as McElligott notes, something economically terrible must have happened to prompt such an immediate U-turn by a credibility-crushing Federal Reserve.

{kind=link}

Tactically, SpotGamma notes that if the market does drift higher into 4500 Call Wall, then positive gamma & resistance should increase. Therefore vanna would shift neutral but gamma would start to act as resistance.

As long as the market holds >=4400 then vanna, or the delta hedging impact due to a change in implied volatility, is still supplying a bit of support.

Should markets sell off, we still see little material support below.

{kind=link}

We see little support because of the put-hedge destruction over the last week. If traders elect to purchase puts (which adds to dealer negative delta) this could coincide with a spike in IV. Both of these factors would add speed to any drawdown.

Tyler Durden

Tue, 03/22/2022 – 12:25