42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Nomura: Gamma Shock RIP

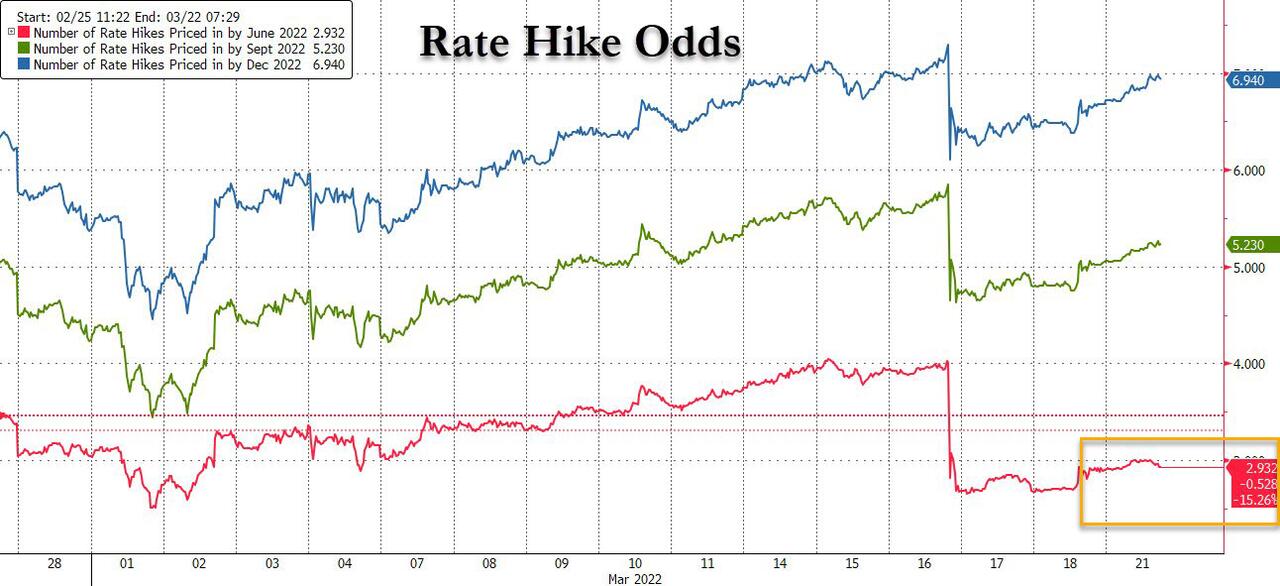

After a breathless week, which saw stocks plunge then soar even as Powell unveiled a hawkish hike and a near-record quad witch a few days later led to a continuation of the meltup, the torrid trading continued on Monday with Fixed-Income positioning today remaining quite bearish hawkish, as markets shift their attention to an avalanche of Fed speakers ratchet up their hawkish forward guidance which has seen Fed hike forwards pick up further pace (75bps by June!) as markets brace for more inflation upside volatility.

{kind=link}

Of note, the market is still focusing on Friday’s remarkably hawkish commentary from Bullard, Wallard and even uber-dove Kashkari

Bullard was on the tape recommending Fed Funds rising above 3% this year — i.e. multiple 50bps hikes in 2022!

Waller stated that he’d like rates slightly above “neutral” (2.5%) by YE and strongly hinted at the potential for a 50bps hike at upcoming meeting(s)

We also learned that Kashkari’s dot-plot projected rates at 1.75% – 2.00% by end 2022—i.e. seven hikes in ‘22 from a mega-dove—while also advocating a balance-sheet unwind pace running 2x’s prior roll-off, which would equate to max caps of $100B ($60B UST / $40B MBS).

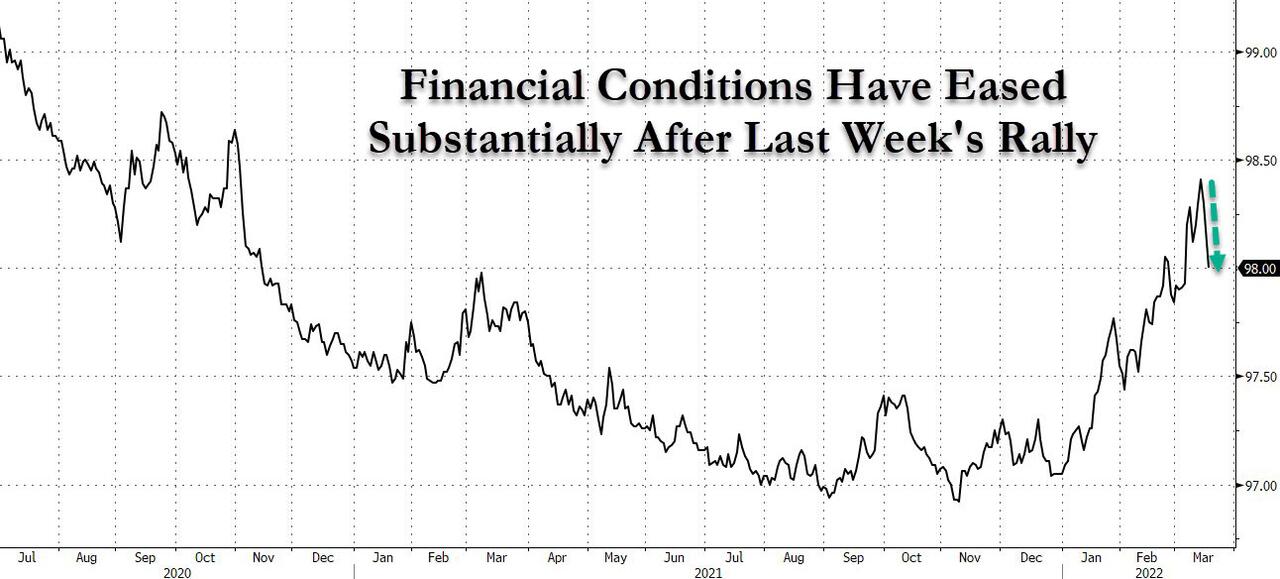

A separate catalyst for the resumption in higher rate hike odds is that financial conditions eased substantially in the past week as a result of the market rally.

{kind=link}

Of course, as we have been hammering every day last week, and as Nomura’s Chalir McElligott again notes in his morning note today, with all this front-loaded hawkishness being projected from Fed speakers, “the Market is already saying that the Fed will have to cut in late ’23 / early ’24 as the hiking will cause market trouble and / or Recession after being pushed into “restrictive policy” territory.”

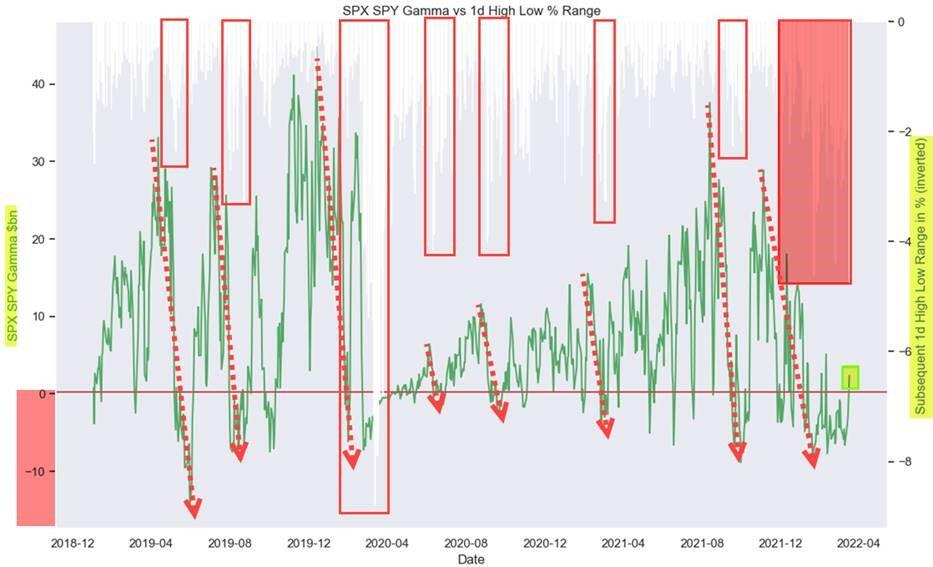

Meanwhile, in addition to this potential “Fed will soon ease” tailwind, equities are also in the midst of a burgeoning “virtuous” regime change, where after last week’s iVol crush/Spot rally, McElligott sees the aggregate options Dealer positioning back to a stabilizing/ shock-absorbing “Long Gamma vs Spot” location in SPX / SPY, QQQ and IWM just as Goldman noted late on Sunday.

According to the Nomura x-asset strategist, this should mean greater market stability with smaller intraday trading ranges, as Dealer hedging flows will now tend to insulate from large price swings (buying dips / selling strength), which suppresses realized Volatility (great “RIP Gamma Shock” chart below).

{kind=link}

Fast forwarding to today, we had Bostic state that getting inflation under control is the “top priority” for 2022, while Powell has prepared text at noon/Q&A thereafter. And, as noted above, markets are currently pricing in 57% odds of a 50bps hike in May, and 75bps by June—so a 50bps and 25bps somewhere, regardless of month, according to McElligott.

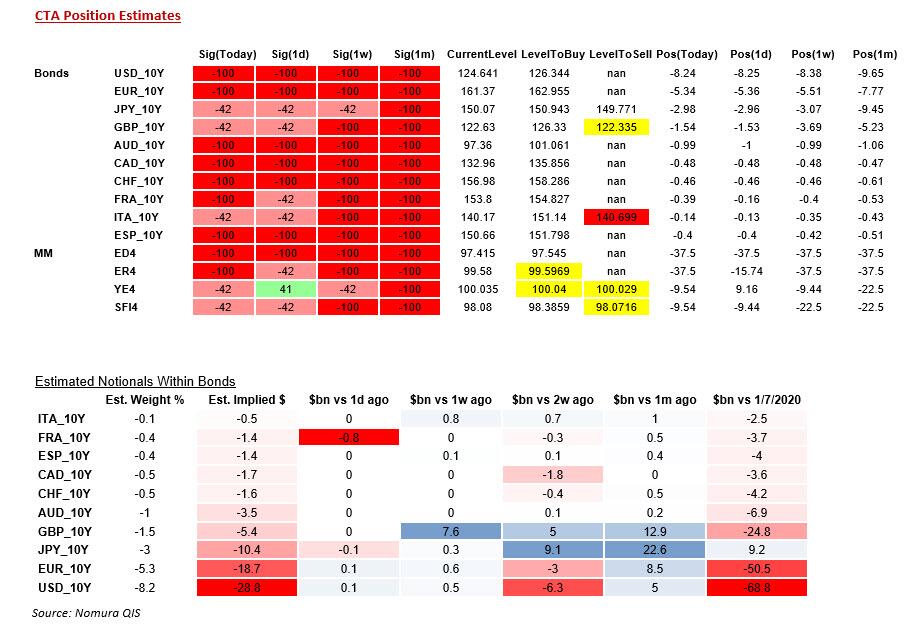

All this takes place with Charlie noting that rates positioning is still very short/hawkish:

TFF data showed that Leveraged Funds were hammering Eurodollars ahead of the Fed, increasing net Shorts by 440k contracts, with Net Shorts now -2.64mm contracts (-$87.8B TY Futs equiv) which is the largest “Short” since Q3 2018

Leveraged were lumpy buyers of the belly, however, ~$14mm / 01 btwn FV and TY

Asset Managers continued to aggressively reduce longs, selling ~$20mm / 01 of cumulative FV & TY

CFTC data showed Specs sold another -$4.4B on UXY (3 weeks in a row, 9th of the past 11 as sellers); there have only been two other periods when the Spec Net Positioning on UXY was at a deeper Short: Jan / Feb 2019 (when the Fed concluded their last hiking cycle) and March 2020 (pandemic / easing commencement)…both versus the current period, as we have just now commenced “lift-off”

{kind=link}

Meanwhile, the Nomura CTA model sees the aggregate G10 Bond Net (Short) Exposure currently -20.9% (10.3%ile), but well off of the “most short” level of -50.5% made back on Oct 20th, 2021, after recent bits of covering in Gilts, EGBs and JGBs over the past month. That said, the CTA Trend model remains “Short” across the board to varying degrees in both G10 Bonds (-100% Short for USD 10Y, EUR, AUD, CAD, CHF, FRA and ESP, while JPY 10Y, GBP and ITA are all -42% Short) and Money Markets (-100% Short in ED$ and Euribor, -42% Short in Euroyen and SONIA futs).

{kind=link}

Of course, as noted above, with all this front-loaded hawkishness being projected from Fed speakers, the Market is already saying that the Fed will have to cut in late ’23 / early ’24 as the hiking will cause market trouble and / or Recession after pushing us into “restrictive policy” territory.

{kind=link}

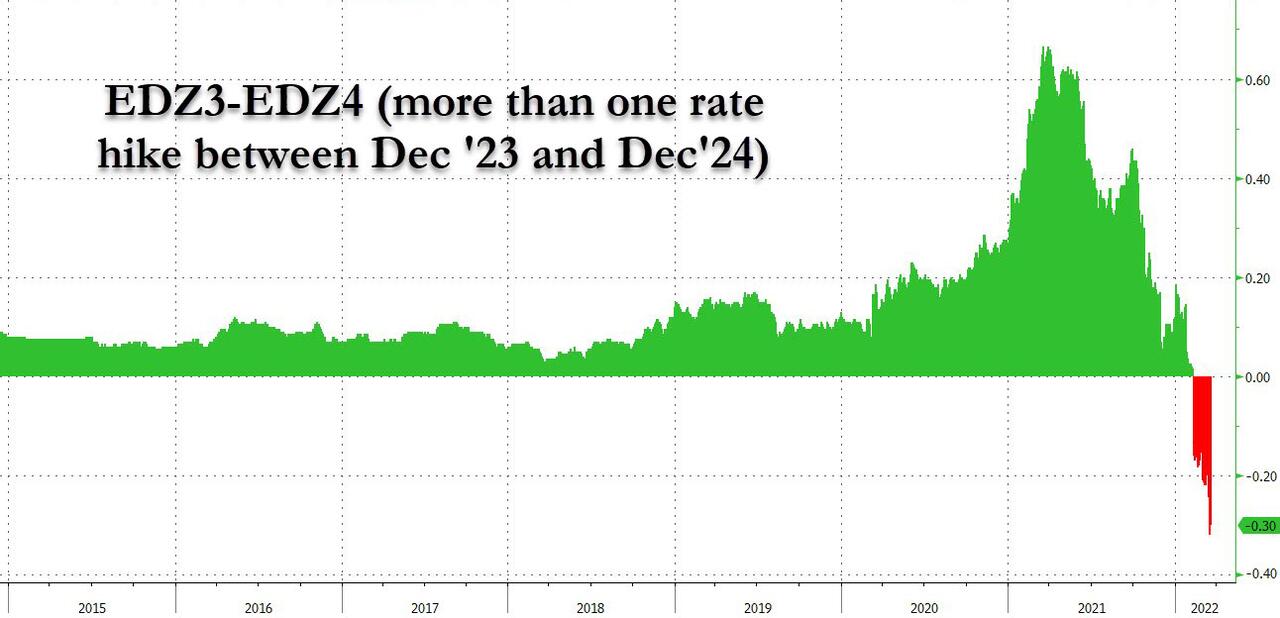

… while EDZ3-Z4 is now pricing in 31bps of cuts, as SPX “GAMMA SHOCK” (NOV 21 – MAR 22) R.I.P.? the market now agrees with our long-held view that the Fed is “hiking into a recession.”

{kind=link}

Looking at stocks, the equity rally today is tentatively trying to extend gains, thanks to options dealer “long gamma vs spot” stabilization. As noted late last night, and as McElligott writes today, after this past Friday’s Serial Op-Ex, we find ourselves in an entirely new world vs where Equities have been for much of the prior 5 months, as the iVol crush / Spot rally has now seen the Dealer Gamma position move back to “Long Gamma vs Spot” for key Equities indices and ETFs SPX / SPY, QQQ and IWM.

Commenting on this “Long Gamma vs Spot” inversion, the Nomura strategist notes that it is “a wholesale regime change back towards greater market stability with smaller intraday trading ranges, as Dealer hedging flows will now tend to insulate from large price swings (buying dips / selling strength) which suppresses realized Volatility, as opposed to prior “Short / Negative Gamma vs Spot” positioning, where Dealer index / ETF options hedging flows instead accelerated market momentum (buying highs / selling lows) which created constant overshoots and higher rVol, and which had predominately been the case since Nov ’21.”

In short, it will take a far greater shock to send stocks careening lower this time.

Finally, for those asking what the source of McElligott’s title “Let them eat lentils”, the answer is what may have been the most tone-deaf Bloomberg op-ed ever published over the weekend…

Inflation stings most if you earn less than $300K. Here’s how to deal:

➡️ Take the bus

➡️ Don’t buy in bulk

➡️ Try lentils instead of meat

➡️ Nobody said this would be fun https://t.co/HGJEoXL5ZZ

— Bloomberg Opinion (@bopinion) March 19, 2022

Tyler Durden

Mon, 03/21/2022 – 12:35