42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

The Contest Against Inflation Is Being Lost Despite Rate-Hikes

By Ven Ram, Bloomberg Markets Live commentator and analyst

So the Federal Reserve just pushed the button that says “a little less accommodative” on its dashboard. The Bank of England has been at it for three months now.

On Wednesday the Fed sounded as hawkish as it has ever done in a long time, outlining six more rate increases this year and an intent to trim its balance sheet. The BOE brought its benchmark flush with levels that prevailed before the pandemic first struck.

{kind=link}

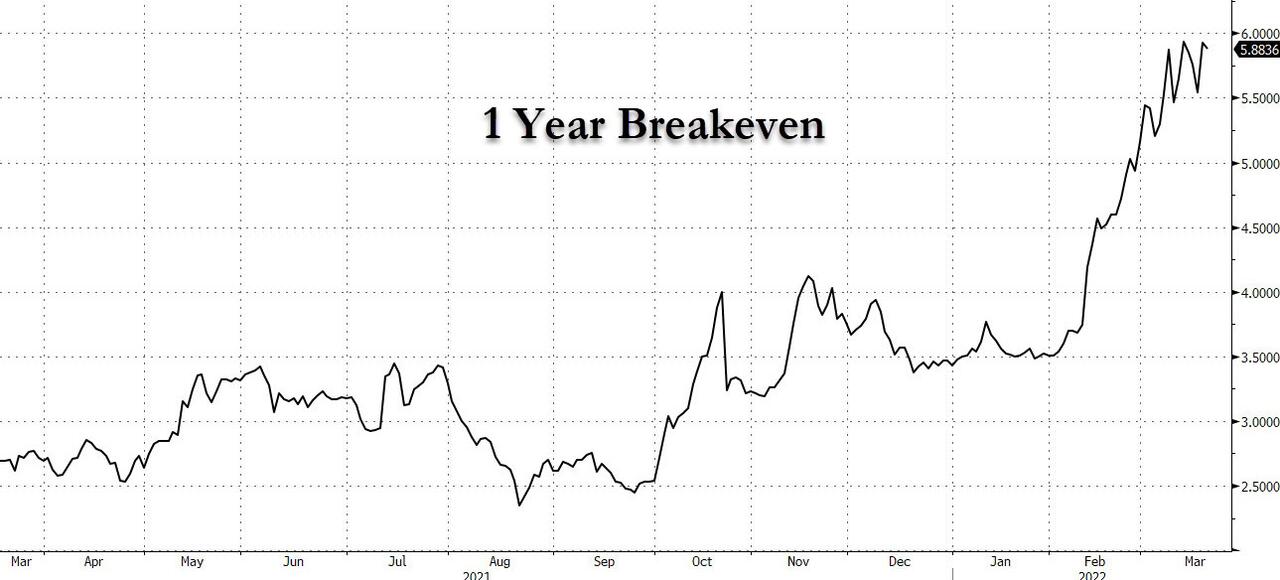

You would expect those moves to ease concerns about inflation. But that’s not quite what’s happening. Expectations about price pressures aren’t even staying put. In fact, they are marching higher. In the U.S., the one-year inflation breakeven rate is fast approaching 6% and shot up a phenomenal 38 basis points yesterday — ironically, just a day after the Fed raised rates.

{kind=link}

You could attribute the one-year rate being so elevated at least partly to the war, but what about the five-year rate that has surged some 75 basis points so far this quarter alone? You could look at the gamut of inflation derivatives ranging from zeroes to inflation forwards to real rates, and they will all pretty much portray the same story — that the tug-of-war against price pressures is far from being successful and is going the other way.

Over in the U.K., 10-year real rates are so deeply negative that they would be akin to levels of some distressed emerging-market economies. And lest it should be forgotten, the U.K. has long run a considerable current-account deficit — in effect, it depends on the kindness of strangers to fill the gap, thank you. And the central bank is “rewarding” investors with punitive real yields that they would have rejected had it come with an emerging-market label. Yet we saw a dissent vote against raising rates yesterday and the BOE sticking to its “modest tightening” needed yarn.

As Larry Summers put it, “We have gone even further towards losing it (control of inflation) in Britain” — that was in October, and since then retail-price inflation has accelerated to almost 8%. Back in November, former BOE Governor Mervyn King warned that “a satisfactory theory of inflation cannot take the form, ‘inflation will remain low because we say it will’.” Of course, it’s all too easy to raise the recession bogeyman, but a) monetary policy is still way too accommodative and not even in neutral territory yet, let alone in restrictive mode; and b) indicators of recession aren’t exactly heightened yet.

Maybe the smaller central banks in the developed world such as New Zealand and Norway can offer their bigger brethren a lesson or two: they tightened policy right when their economies needed it, and did not look the other way when inflationary fires were raging.

Tyler Durden

Sat, 03/19/2022 – 12:30