Hedges: The Slow-Motion Execution Of Julian Assange Continues Authored by Chris Hedges via Scheerpost.com, The decision by the High Court...

Read More

NY Fed Survey Finds Broad Improvement In Economic Sentiment As Inflation Expectations Slide

One month after the October NY Fed consumer expectations survey showed a rebound in stagflation dynamics as inflation expectations at both the 3 and 5 year horizon increased while perceptions about the broader economy deteriorated (especially as debt delinquency expectations hit a 4 year high), the deterioration in sentiment reversed substantially in the latest, November survey, which saw inflation expectations decline at the short-, medium-, and longer-term horizons. At the same time, labor market expectations improved with households reporting a lower likelihood of higher unemployment and job loss, and a higher likelihood of finding a job if they were laid off. Perceptions of credit access and expectations for future credit access both improved in October, and households reported a lower likelihood of missing a minimum debt payment over the next three months. In short: Trump becomes president and sentiment about the economy immediately turns more favorable.

Here are the details from the NY Fed’s survey (which is an internet-based survey of a rotating panel of approximately 1,300 household heads. Respondents participate in the panel for up to 12 months, with a roughly equal number rotating in and out of the panel each month).

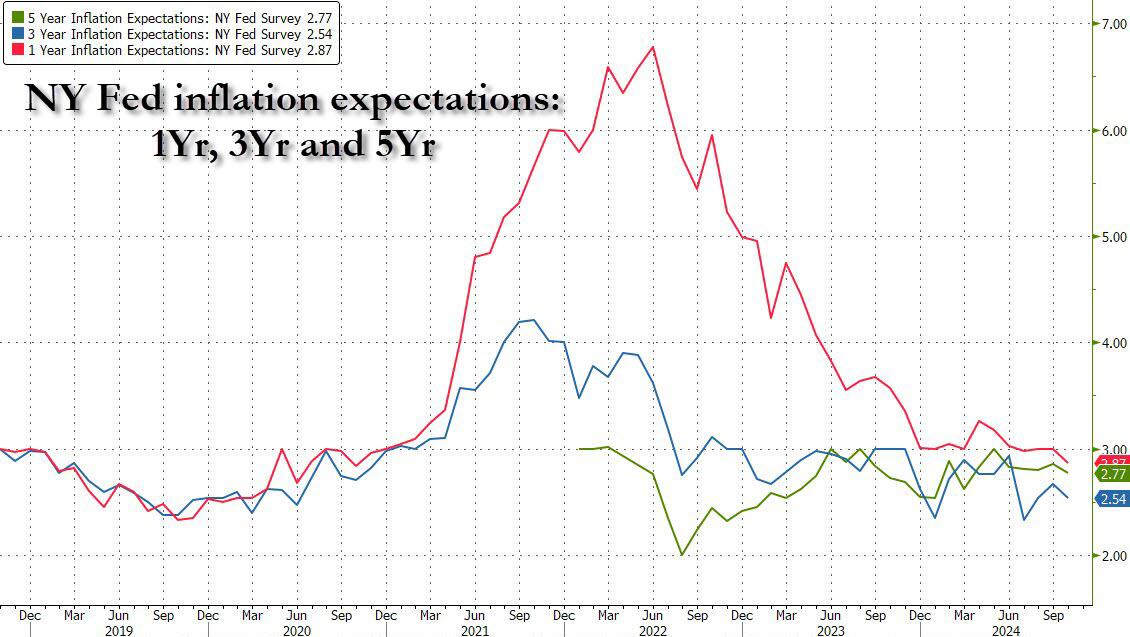

One day ahead of the October CPI report, one-year ahead inflation expectations declined from 3.0% to 2.87%, the lowest since October 2020; three-year-ahead inflation expectations declined by 0.2% point to 2.5%, and five-year-ahead inflation expectations declined by 0.1% point to 2.8%. The survey’s measure of disagreement across respondents (the difference between the 75th and 25th percentile of inflation expectations) declined at all three horizons, while median inflation uncertainty declined at the three- and five-year horizons.

Over the next five years, lower-income and less-educated consumers were most inclined to see a drop in long-term inflation (suggesting educated consumers realize that prices are set to rise). Among respondents with a high-school education or less, the expected rate five years ahead dropped to 2.4%, from 2.9% in September. The drop was even steeper for consumers with incomes below $50,000, falling to 2.1% from 2.7%.

The report will provide the Fed will comfort that consumer inflation expectations continue to be anchored – an economic signal the Fed is monitoring as it decides how quickly to lower interest rates. Such surveys of moods aren’t scientific predictions, but they can help inform about future behavior because expectations can be self-fulfilling since consumers who anticipate higher inflation are typically more apt to demand higher pay. That can lead to what economists call a wage-price spiral, where employers facing higher wage bills seek to increase prices to maintain their margins.

Yet while consumers expect inflation to taper, inflation expectations among US business leaders increased in the fourth quarter of 2024, according to the Cleveland Fed’s Center for Inflation Research. Its latest survey found that CEOs expect inflation to be 3.8% over the next 12 months, up from 3.4% in July.

Back to the household survey, median home price growth expectations were unchanged at 3.0% in October. This series has been moving in a narrow range between 3.0% and 3.3% since August 2023.

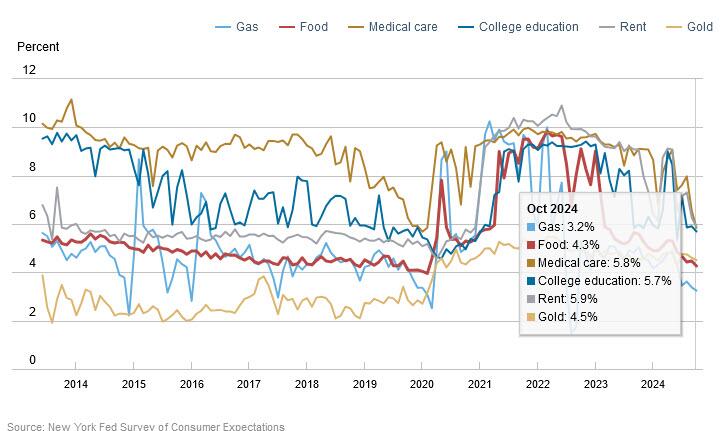

Year-ahead commodity price expectations declined by 0.2% for gas to 3.2% (the least in two years) decline by 0.2% for food to 4.3% the lowest since before the pandemic, 0.2% for the cost of college education to 5.7%, and 0.4% for rent to 5.9%. The expected cost of medical care also declined by 0.8% to 5.8%, the measure’s lowest reading since January 2020.

Labor market expectations, meanwhile, improved with households reporting a lower likelihood of higher unemployment and job loss, and a higher probability of finding a job if they were laid off.

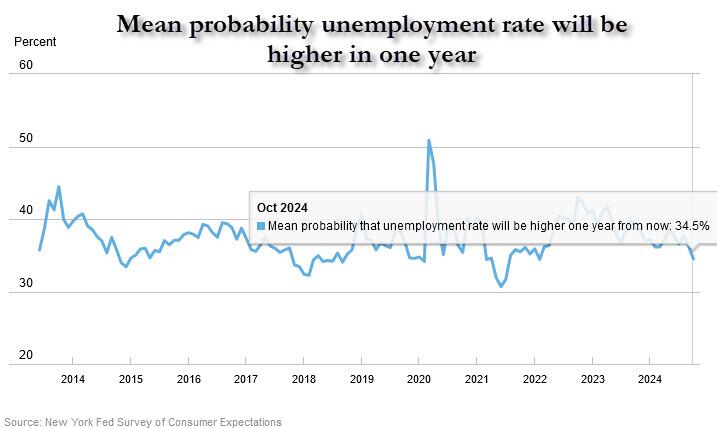

Mean unemployment expectations—or the mean probability that the U.S. unemployment rate will be higher one year from now—decreased by 1.7% to 34.5%, the measure’s lowest reading since February 2022.

There were more employment green shoots: the mean perceived probability of losing one’s job in the next 12 months decreased by 0.3 percentage point to 13.0%. This decrease was most pronounced for respondents under the age of 40 and those with a college degree. The mean probability of leaving one’s job voluntarily in the next 12 months increased by 0.1 percentage point to 20.5%.

The mean perceived probability of finding a job (if one’s current job was lost) increased by 3.3% points to 56.0%, the measure’s highest reading since October 2023. This increase was most pronounced for respondents with a high school education or less.

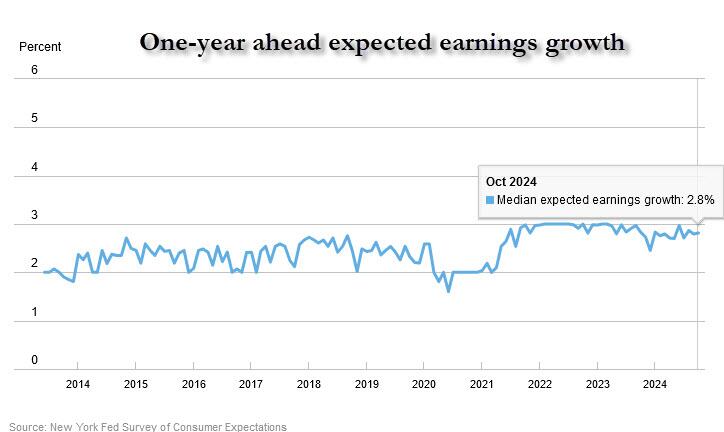

Turning to earnings, the median year-ahead earnings growth expectations were unchanged at 2.8% in October. The figure has moving within a narrow range between 2.7% and 3% this year, providing employers some certainty in their anticipated labor cost projections.

Household finance expectations were also broadly solid with modest improvements in the latest report:

- The median expected growth in household income was unchanged at 3.0% in October. The series has been moving in a narrow band between 2.9% and 3.3% since January 2023.

- Median household spending growth expectations were unchanged at 4.9% but remain well above pre-pandemic levels.

- Perceptions of credit access compared to a year ago improved in October, with a decreasing (increasing) net share of households reporting it is harder (easier) to obtain credit than one year ago. Expectations for future credit availability also improved in October.

- The average perceived probability of missing a minimum debt payment over the next three months decreased by 0.3 percentage point to 13.9%, the first decrease since May 2024. The decrease was most pronounced for those under the age of 40. This series remains above its 12-month trailing average of 12.6%.

- The median expected year-ahead change in taxes at households’ current income level was unchanged at 4.0%.

- Median year-ahead expected growth in government debt increased by 0.5 percentage point to 8.5%.

- The mean perceived probability that the average interest rate on saving accounts will be higher in 12 months decreased by 0.5 percentage point to 24.6%.

- The mean perceived probability that U.S. stock prices will be higher 12 months from now decreased by 1.2 percentage points to 39.1%.

Putting it all together, perceptions about households’ current financial situations compared to a year ago improved in October, with a rising share of households reporting a better situation relative to those reporting a worse situation.

Similarly, year-ahead expectations about households’ financial situations improved in October.

And all it took was Trump’s blowout victory in the presidential elections.

Tyler Durden

Tue, 11/12/2024 – 14:00

Recent Comments