42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Amazon Jumps On Record AWS Profit Margin, Solid Holiday Quarter Guidance

As we noted in our preview earlier, Hedge Funds are getting picky into the quarter. While most were short as given a perceived miss below Street for Q4 EBIT, some have covered as downside (if any) would be short-lived with investors having messaged a “buy-the-dip” mentality. Investors are starting to understand the variability of operating income and there is a general agreement that this is the best capital allocator in the space, so would rather Amazon invest than harvest profit dollars. The bull case continues to center around

- prospects for faster gross merchandise value growth and share gains on higher level of service amidst ongoing fulfillment regionalization efforts in the US and eventual global rollout;

- ongoing margin expansion in Amazon’s ecommerce franchise due to improving unit economics;

- new high margin revenue stream from Prime Video with ads – although still in its early innings it should become a meaningful contributor over time, especially as content costs are already incorporated in the model.

Investors are also focused on the payouts through the investment cycle with AWS penciled in for next year; ecommerce a constant; NBA cash doesn’t go out the door until 2025 so should see return on investment after that; Kuiper spending money on R&D now, but equipment and launch capitalization and depreciation are on the other side, which doesn’t come in until 2H25. The most important things will be:

- directional commentary around AWS growth/optimization;

- signals of retail margin improvement as suggested by management commentary on “cost to serve”;

- progress with fulfillment regionalization and broader cost containment efforts;

- directional commentary on fiscal year capex for ecommerce (up with business) and ongoing AWS investments;

- commentary on adoption of Prime Video with ads and ad industry broadly and;

- positioning around GenAI investments.

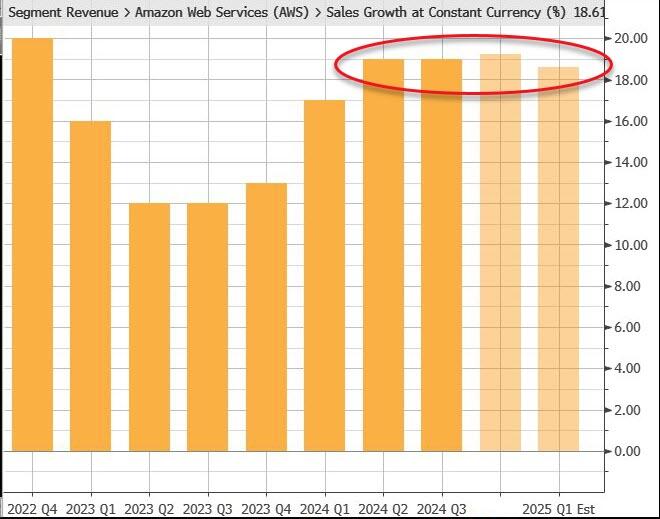

The AWS bogey is 21% and reaching AWS growth of 21% in 3Q24 implies sequential revenue growth of $1.62 bn, well above the 3Q23 (depressed) level of $920 mn and the second-best quarter ever, apart from the 4Q21 (boom period) sequential revenue growth level of $1.67 bn. While doable, this isn’t a slam dunk.

With that in mind, this is what AMZN reported for Q3:

- EPS $1.43 vs. $1.26 q/q, beating estimate $1.16

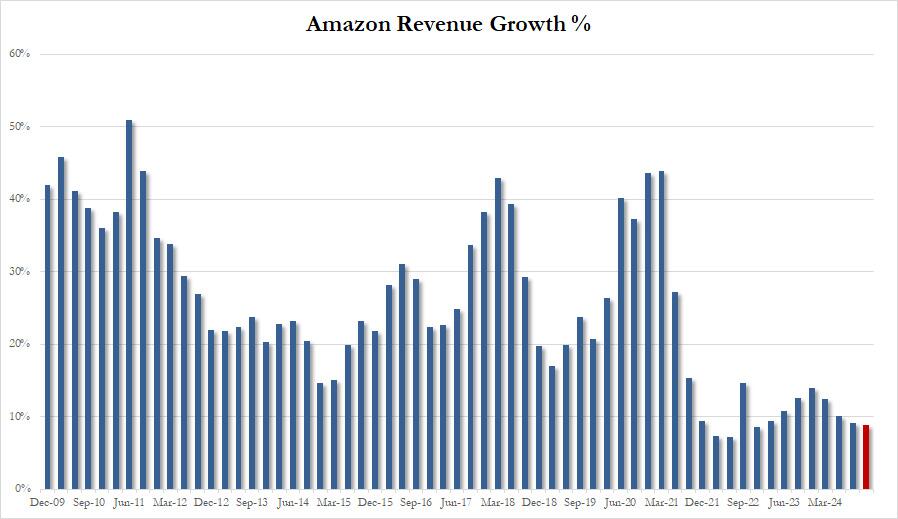

- Net sales $158.88 billion, +11% y/y, beating estimates $157.29 billion

- Online stores net sales $61.41 billion, +7.2% y/y, beating estimate $59.64 billion

- Physical Stores net sales $5.23 billion, +5.4% y/y, beating estimate $5.17 billion

- Subscription Services net sales $11.28 billion, +11% y/y, beating estimate $11.17 billion

- Subscription services net sales excluding F/X +11% vs. +13% y/y, beating estimate +9.86%

- North America net sales $95.54 billion, +8.7% y/y, beating estimate $95.22 billion

- International net sales $35.89 billion, +12% y/y, beating estimate $34.55 billion

- Third-Party Seller Services net sales $37.86 billion, +10% y/y, missing estimate $38.22 billion

- Third-party seller services net sales excluding F/X +10% vs. +18% y/y, missing estimate +11.8%

- Amazon Web Services net sales $27.45 billion, +19% y/y, missing estimate $27.49 billion

- Amazon Web Services net sales excluding F/X +19% vs. +12% y/y, missing estimate +19.2%

Turning to operating results we find the following:

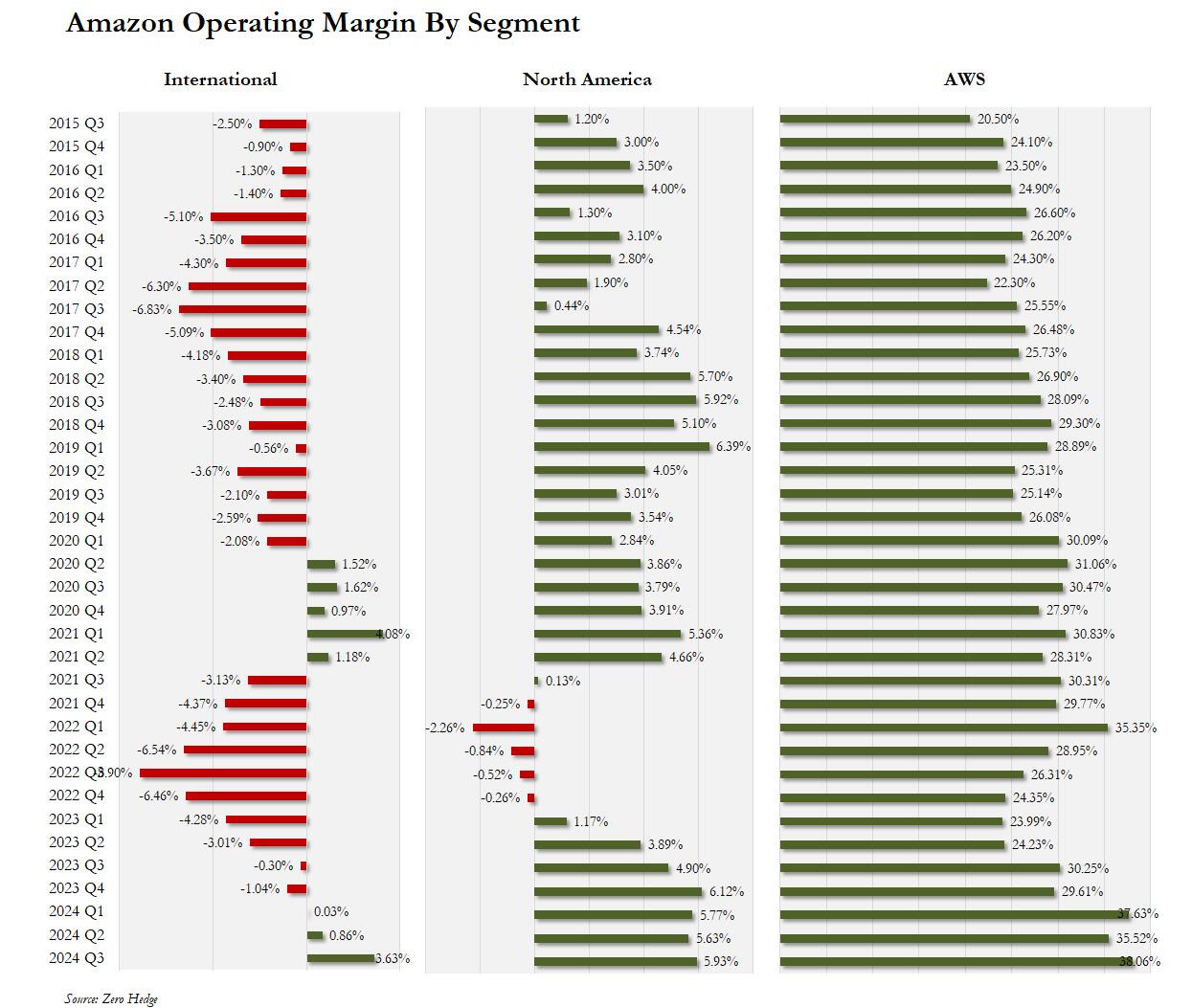

- AWS operating profit $10.4BN, beating estimates of $9.12BN

- North America operating margin +5.9% vs. +4.9% y/y, beating estimate +5.58%

- International operating margin 3.6% vs. -0.3% y/y, beating estimate 1.23%

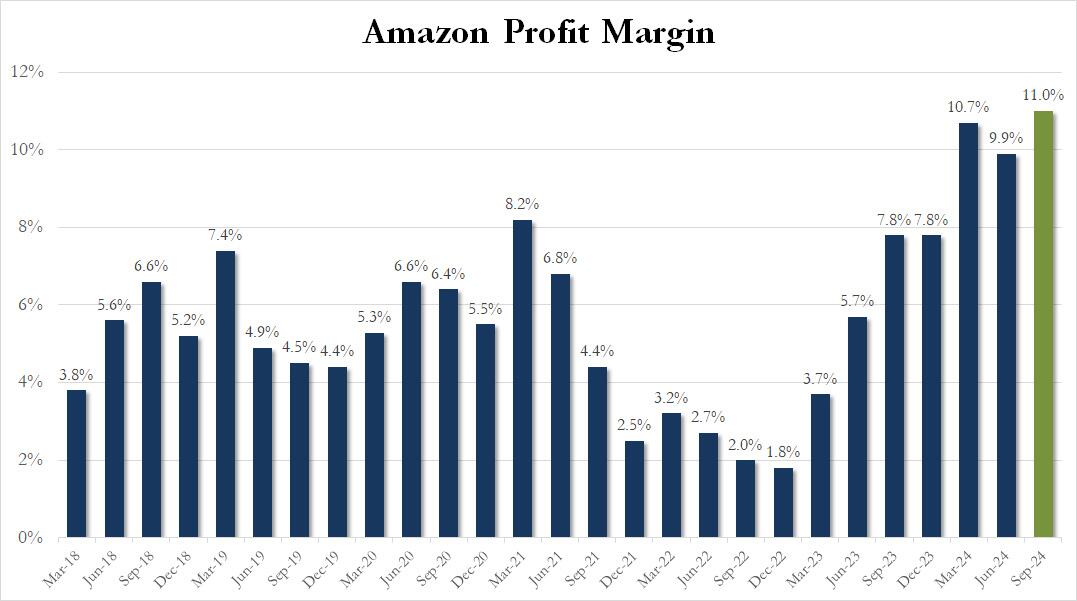

- Operating income $17.41 billion, +56% y/y, beating estimates $14.75 billion

- Operating margin 11% vs. 7.8% y/y, beating estimates 9.34%, and an all time high

As for expenses, these were slightly above estimates suggesting the company can use some more cost optimizations:

- Fulfillment expense $24.66 billion, +11% y/y, higher than estimates of $24.35 billion

- Seller unit mix 60% vs. 60% y/y,

Of the above, the most notable highlight – as per our preview – was AWS which grew revenue by a whopping 19% to $27.45BN, which however was just below the sellside estimate of $27.49BN. Furthermore, ex FX, the growth was also 19.0%, below the 19.2% bogey. So maybe a little weakness here similar to Microsoft.

But if revenue growth for AWS was a bit light, the margin more than offset it, rising from 35.5% to 38.1%, a record for the segment. This was thanks to AWS operating income of $10.4 billion, exceeding analysts’ average projection of $9.12 billion. The fact that international margins also surged to 3.63%, the highest since Covid, certainly helped.

As a result of the surge in international and AWS profits, Amazon’s consolidated operating margin rebounded strongly, and after dipping modestly in Q2 from the Q1 record of 10.7%, rose to a new all time high of 11.0% in Q3!

Looking ahead, the company projected profit and revenue in the current quarter that exceeded analysts’ estimates on optimism for a strong holiday shopping season:

- Revenues for Q4 are expected to be between $181.5 billion and $188.5 billion, or to grow between 7% and 11% compared with fourth quarter 2023, with the midline of 185 billion just below consensus estimate of $186.36 billion.

- Operating income for Q4 is expected to be between $16 billion and $20 billion, compared with $13.2 billion in fourth quarter 2023. and in line with the median estimate of $17.5 billion.

If accurate, that would mean Q4 revenue will grow at the slowest pace sine Dec 2022.

“As we get into the holiday season, we’re excited about what we have in store for customers,” Chief Executive Officer Andy Jassy said in the statement.

In response to the solid results, which saw revenues beat and guidance in line, despite a mixed report from AWS, the stock surged, and was last trading around $195, up about 4% on the day, and basically where it was to close Wednesday.

Tyler Durden

Thu, 10/31/2024 – 16:34