42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

SEC Slip-Up Hints At Fresh Financial Fears

Authored by Adam Sharp via DailyReckoning.com,

Oops. Last week the SEC accidentally published internal commentary along with a speech by Chair Gary Gensler.

Here’s one of the comments which was mistakenly included.

I strongly recommend that a sentence be placed here (or somewhere [sic] in the first part of the speech) to reassure markets that you are not making the speech because you think there is an imminent crisis.

{kind=link}

These internal comms were quickly deleted from SEC.gov, but not before the page was archived for posterity. The slip-up reveals anxiety among regulators over messaging.

Mr. Gensler’s speech addressed financial crises, bank restructurings, and the importance of public disclosures. In it, the SEC Chair rightly argued that depositors need transparency to make good decisions.

If a large financial institution is restructured, the market’s need for disclosure doesn’t go away. Indeed, I believe the market’s need for robust disclosure becomes all the more critical. First, it is the best way to ensure that investors, counterparties, and depositors will have sufficient confidence to remain with the firm.

It’s a solid point, transparency does need to improve. But there’s something else missing here that we need to discuss.

Back in June, Daily Reckoning’s Jim Rickards warned that the banking crisis may still have legs.

Investors are relaxed because they believe the banking crisis is over. That’s a huge mistake. History shows that major financial crises unfold in stages and have a quiet period between the initial stage and the critical stage.

In the article, Mr. Rickards pointed out a key flaw with Mr. Gensler’s argument that transparency should allow depositors to make wise decisions. That flaw is the speed at which money moves in today’s world.

On the other hand, this crisis could reach the acute stage faster. That’s because of technology that makes a bank run move at the speed of light. With an iPhone, you can initiate a $1 billion wire transfer from a failing bank while you’re waiting in line at McDonald’s. No need to line up around the block in the rain waiting your turn.

When a crisis hits, rational analysis is often the first casualty. In this world where money moves in a blink, if you hear about potential issues at your bank, most of us aren’t going to pull up its financial filings, spend hours analyzing them, and then make a decision. We’re going to move it to a safer bank (or a mattress, or into gold) ASAP.

So while it is good to hear that the SEC Chair favors more transparency, it doesn’t do much to allay our concerns. More disclosure could actually accelerate a crisis due to the velocity of information and money today. If a crisis hits, things can happen fast.

Why The ‘Imminent’ Concern?

Let’s get back to those accidentally-published internal comments. An SEC staffer was concerned that Mr. Gensler’s speech might give the impression of an “imminent crisis”. Whenever regulators discuss the solvency of financial institutions there’s a risk that it is interpreted negatively by markets. It’s a valid worry.

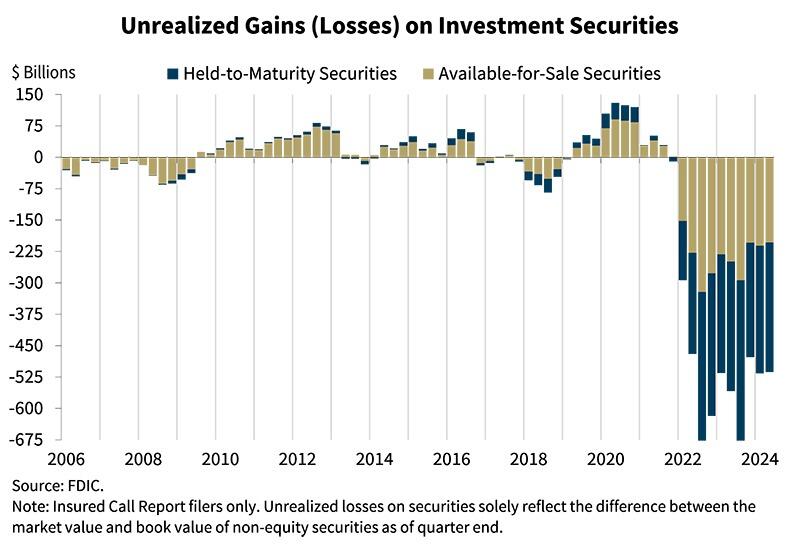

Unfortunately, in this market, there are some excellent reasons to interpret the remarks in a cautious light. Let’s start with the latest data on unrealized losses at banks.

{kind=link}

Remember when this chart was making the rounds in 2022 and 2023?

The updated FDIC data continues to show an unprecedented and sustained rise in unrealized losses at banks. Notice how small the losses during the global financial crisis appear in comparison.

These are unrealized losses on banks’ bond portfolios, primarily caused by the Fed’s rapid interest rate hikes. When rates rise, the value of existing bonds (with lower yields than new bonds) falls. This is what caused the failure of Silicon Valley Bank.

Unrealized losses stand at $512 billion as reported by the FDIC, down from a peak of around $655 billion. The data has improved a bit, but bank balance sheets remain stressed at historic levels.

Ongoing interest rate cuts should help stem the unrealized bleeding at banks. As rates fall, the price of bonds will rise. But lower rates should also mean lower profitability for the lending side of the business, so it’s somewhat of a double-edged sword for banks.

Even if the unrealized loss situation gets resolved, there are other potential black swans to monitor. After all, why is the Fed planning to cut rates, apparently with haste? Are they simply trying to get ahead of bank losses and soaring debt servicing costs? Or do they potentially see a recession or financial crisis in the near future?

Let’s review our situation.

The Fed is preparing for economic turbulence. Gold is trying to tell us something as it powers to new all-time highs. Job growth for the year was recently revised sharply downward. And now regulators are making speeches about restructuring large financial institutions.

{kind=link}

It sure feels like something’s brewing. If you want to be proactive and check your bank’s unrealized loss ratio, you can use this free tool by Florida Atlantic University. This screener isn’t perfect and doesn’t tell you everything about a bank’s health, but it’s a start.

Besides moving to a better bank, gold and silver remain an excellent way to prepare for potential calamities.

Tyler Durden

Mon, 09/23/2024 – 07:20