Musk Announces X To Sue 'Perpetrators And Collaborators' Behind Advertising Censorship Cartel Elon Musk announced on Thursday that social media...

Read More

Exxon Reports Blowout Earnings, Record Output Thanks To Pioneer Deal

Two weeks ago when Exxon previewed its upcoming earnings, there was some disappointment amid what was viewed as weakness in upstream prices and energy product margins.

{kind=link}

Which is why much to everyone’s surprise, today’s Q2 report by the largest US energy major blew away estimates, revealing the second-best Q2 earnings in company history thanks to the recent closing of the $63 billion Pioneer acquisition, which made Exxon into the second biggest energy player in the world after Aramco (while closest competitor Chevron is still choking on its Hess acquisition).

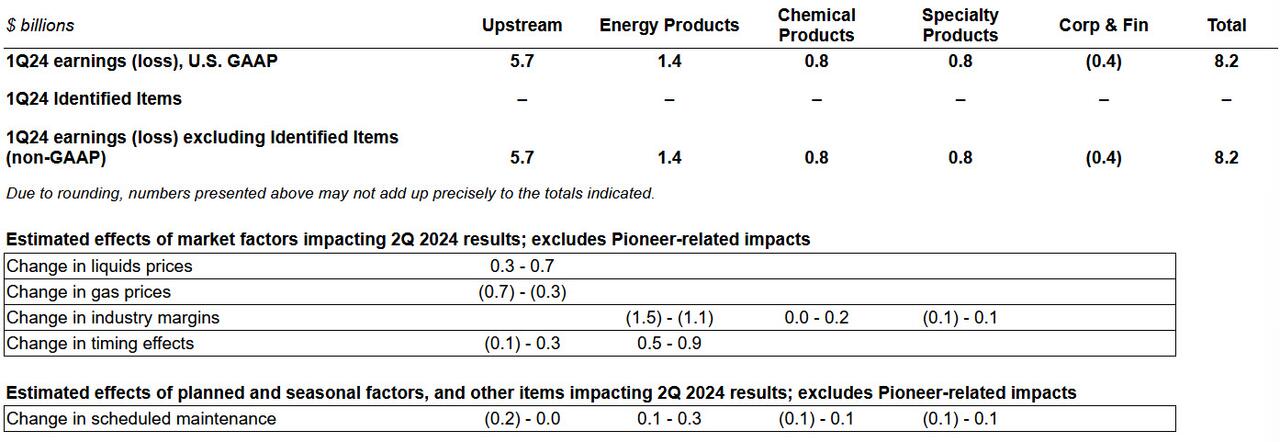

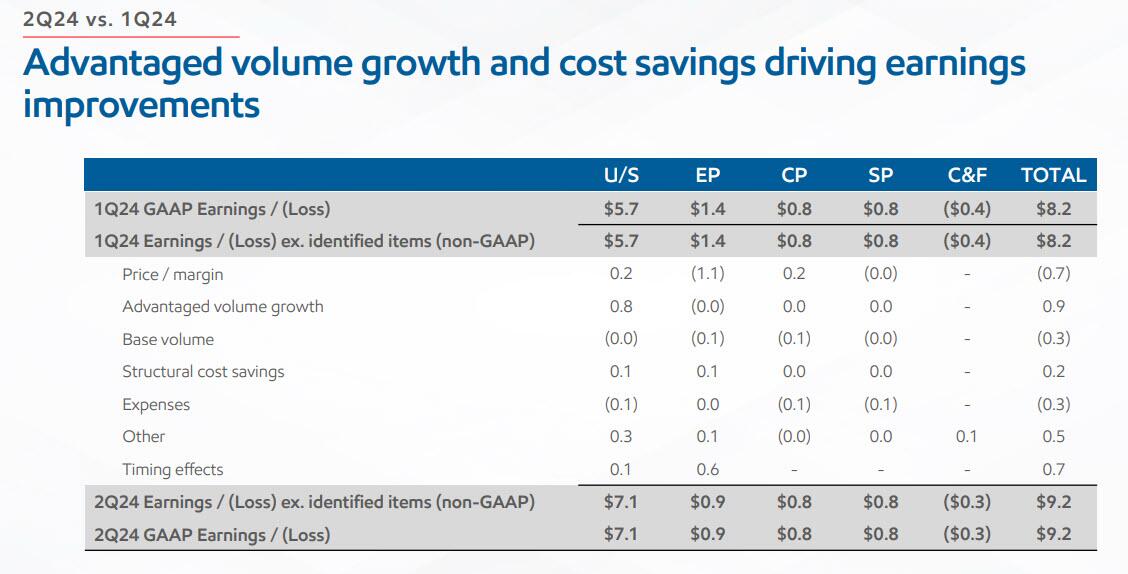

For those who missed it, here is a snapshot of what XOM reported:

Q2 EPS $2.14 (or GAAP earnings of $9.2BN) beating est. $2.02., and up from $2.06 YoY, with E&P (both US and International) drove the beat vs estimates.

Q2 revenue $93.06bn, beating est. $90.09bn.

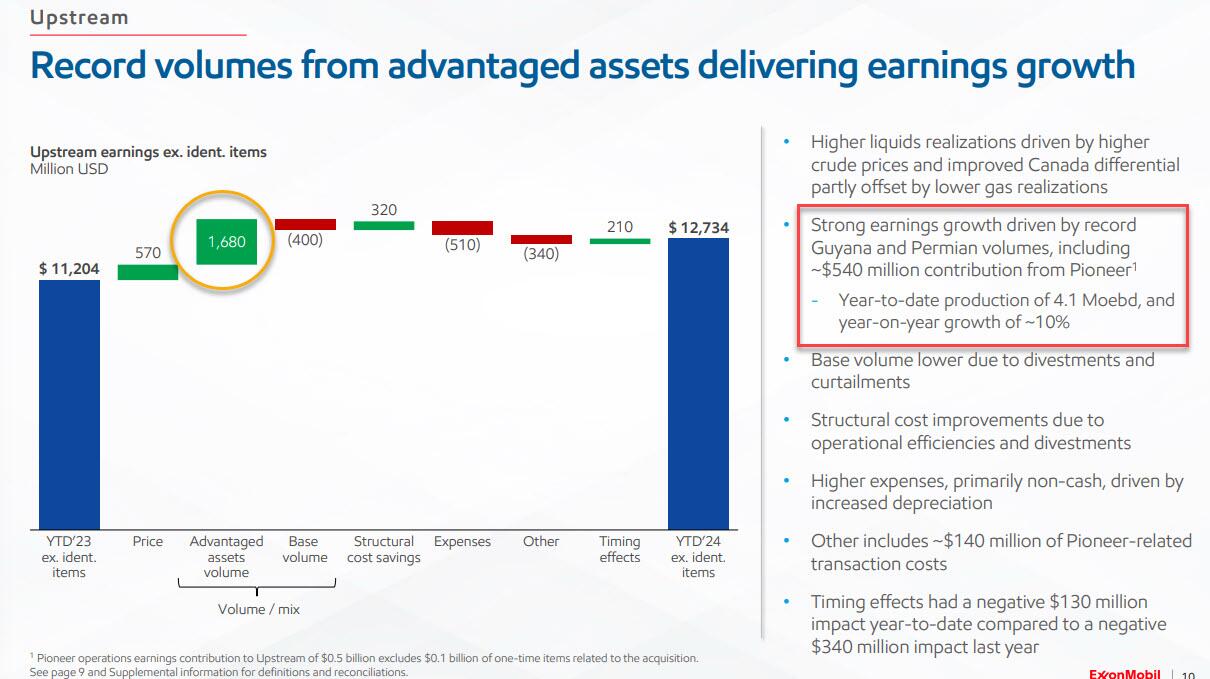

Production higher at 4358 Mboe/d vs. Cons 4242.2 Mboe/d, with stronger US and International liquids and higher International gas production vs estimates on the quarter. Notably, during the quarter, the company achieved record production from both Permian and Guyana assets.

The Pioneer takeover, which closed in early May, helped lift Exxon’s overall production by 15% on a sequential basis, and setting the stage for daily output to average more than 4 million barrels this year.

Capex in quarter came in at $7.04bn vs. Cons $6.23bn; Guided FY capex to ~$28bn, including $3bn for Pioneer.

Cash flow from operations was $10.6bn, cash from operations excluding working capital movements was $15.2 billion.

Shareholder distributions of $9.5 billion included $4.3 billion of dividends and $5.2 billion of share repurchases, consistent with the company’s announced plans.

Expects over $19bn of share buybacks in 2024. Annual buyback pace of $20bn expected through 2025.

XOM delays Golden Pass LNG to late 2025 on contractor dispute.

{kind=link}

Regarding the recently closed acquisition of shale giant Pioneer, Exxon said that the deal closed “50% faster than similar deals in recent years”, the “Integration and synergy execution exceeding expectations”, the combined company has already achieved record production levels of “792 Koebd in June and 782 Koebd in second quarter”, and finally Pioneer has already contributed $0.5 billion in earnings from two months of operations (excluding $0.2 billion of one-time items, primarily transaction costs).

{kind=link}

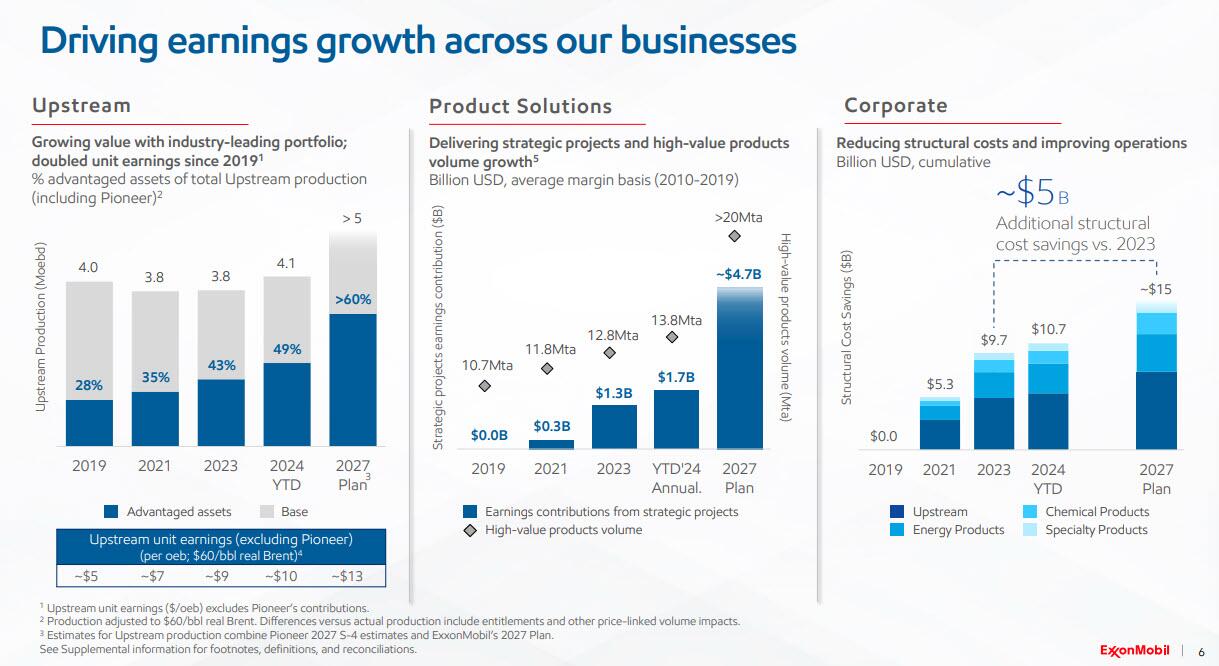

While YTD earnings were $17.5 billion down from $19.3 billion in the first half of 2023, this profit was generated with oil prices much lower, confirming that XOM’s breakeven price continues to drop and the company will be solidly profitable even if oil were to drop dramatically from here.

Additionally, XOM remains on track to achieving cumulative structural cost savings of $5 bn through year-end 2027 (vs 2023 levels). XOM has already achieved $10.7 billion of cumulative Structural Cost Savings versus 2019, including an additional $1.0 billion of savings during the year and $0.6 billion during the quarter.

{kind=link}

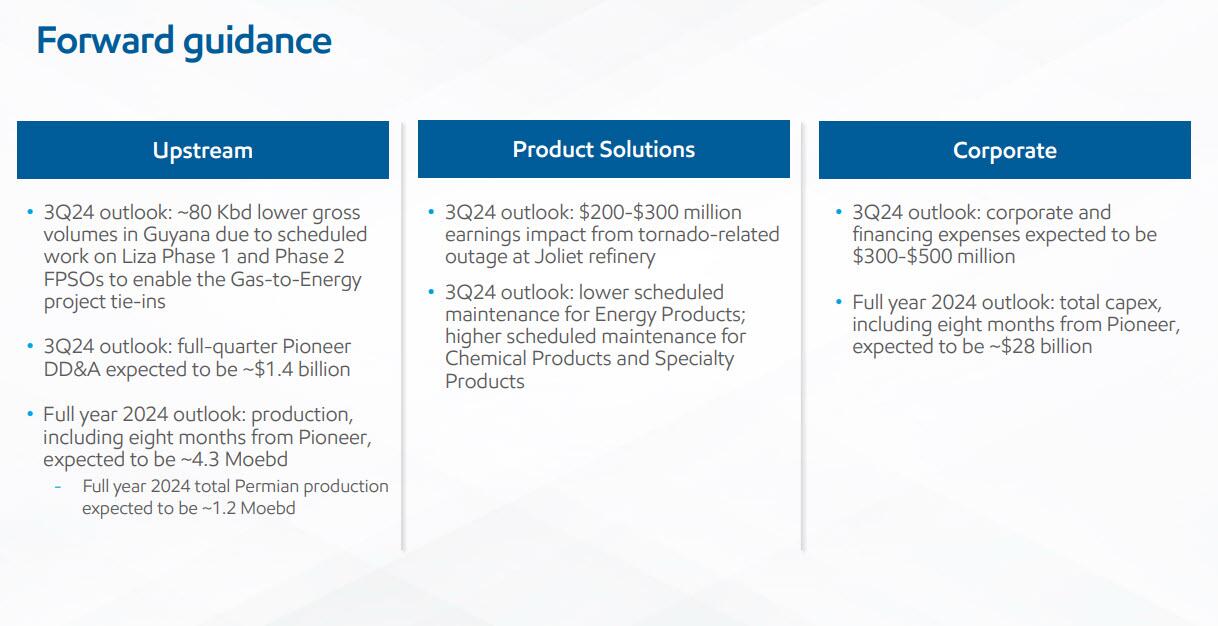

Looking ahead, the company forecasts that production, including eight months from Pioneer, expected to be ~4.3 Moebd, with full year 2024 total Permian production (most Pioneer) expected to be ~1.2 Moebd. In other words, Exxon is now not only the biggest and most important energy company in the world after Aramco, but it is now certainly too big to ever fail in the context of even a Kamala Harris administration. While the market may not appreciate the premium value such a designation entails, it will sooner or later.

{kind=link}

“We delivered our second-highest 2Q earnings of the past decade as we continue to improve the fundamental earnings power of the company,” said CEO Darren Woods; he went on: “We achieved record quarterly production from our low-cost-of-supply Permian and Guyana assets, with the highest oil production since the Exxon and Mobil merger. We also achieved a record in high-value product sales, growing by 10% versus the first half of last year. We closed on our transformative merger with Pioneer in about half the time of similar deals. And we’re continuing to build businesses such as ProxximaTM, carbon materials and virtually carbon-free hydrogen, with approximately 98% of CO2 removed, that will create value long into the future.”

Many oil explorers ramped up cash returns to shareholders as commodity prices soared in 2022 and 2023, and had plenty of cash left over to invest in low-carbon alternatives. But with many renewable bets fizzling, especially among the more virtue-signaling oil majors (mostly in Europe) oil executives have been forced to refocus much of their attention on traditional fossil-fuel projects that can generate long-term cash flows.

Here, Exxon was an exception, having never turned its back on fossil fuels which is why the Kamala/Deep State administration hates it so much. It’s been able to increase production and returns, particularly through fast-growing projects in Guyana and the Permian Basin.

Production in Guyana and the Permian Basin reached all-time highs during the second quarter. Exxon is now the biggest producer in the Permian after closing the Pioneer transaction, its biggest deal since buying Mobil.

“It gives us a really big boost,” CFO Kathy Mikells said during an interview.

Exxon plans to increase annual capital spending by 12% to $28 billion this year as a result of the combination with Pioneer. The boost is “consistent” with what Pioneer was previously spending, Mikells said. Cost savings through the integration process have come in ahead of expectations, she added.

Oil refining, in which Exxon has a bigger footprint than peers, has been a weak performer this year amid lower-than-expected gasoline and diesel demand. Fuel-making margins were compressed by higher prices for heavy crudes, such as those from Canada.

Long story short, the take home message here is that Exxon has become increasingly lean and efficient (largely thanks to the belligerence of the Obama admin) to the point where it now generates the kind of results at $75 oil, that it once needed $90 oil to achieve.

{kind=link}

It is this operational leverage that will push the stock to all time highs soon, and certainly as soon as a new middle east conflict or a massive Chinese stimulus pushes oil back to $100 or over.

Exxon’s investor presentation is below (pdf link)

Tyler Durden

Fri, 08/02/2024 – 15:05