42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

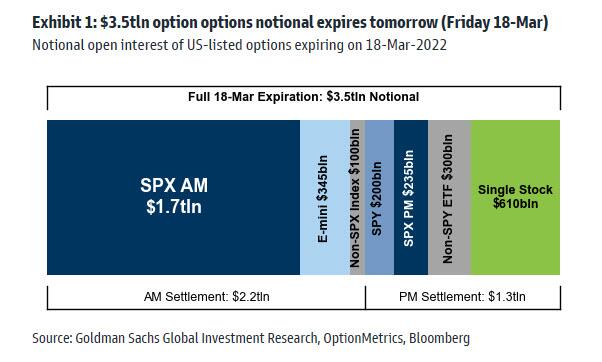

Rally Fizzles As Futures Slide Ahead Of $3.5 Trillion OpEx

After a torrid three days which pushed US stocks up almost 6%, the best 3-day run since the Nov 2020 election..

{kind=link}

… U.S. index futures finally dropped on Friday one day after JPMorgan again said to BTFD, as traders were concerned Washington may take a tougher stance on China for its muted response to Russia’s invasion of Ukraine during a phone call between Xi and Biden set for Friday morning, while bracing for volatility on quad-witching day where $3.5 trillion in options and derivatives are set to expire…

{kind=link}

… as the concurrent rebalancing of benchmark indexes including the S&P 500 sill send volumes soaring. Contracts on the S&P 500 and the Nasdaq 100 both ticked lower about 0.6%. Oil dropped after yesterday’s remarkable surge with WTI trading around $102, while Treasuries and the dollar rose and bitcoin traded just above $40,000.

{kind=link}

In premarket trading, FedEx retreated 2% after missing analysts’ estimates. Morgan Stanley analysts said the magnitude of the misses in the U.S. company’s Express and ground units may be “jarring” for investors. GameStop slumped 7% after reporting quarterly losses that were wider-than-expected, with Baird saying that the video-game retailer’s margins were “significantly” below expectations. Other notable premarket movers include:

Astra Space (ASTR US) drops 5% in premarket trading after the company postponed its fourth-quarter results by two weeks to March 31.

AvePoint (AVPT US) declined 1% in extended trading Thursday after the software company gave a revenue outlook for 2022 that fell short of even the lowest analyst estimate compiled by Bloomberg.

“No clear directional price action will be expected today as traders will also have to brace for a triple witching day in addition to the complicated geopolitical context, which should drive market volatility higher, providing a complicated set-up to very short-term investor,” said Pierre Veyret, a technical analyst at ActivTrades.

“In this environment of tightening monetary policy and higher inflation risks globally, we continue to believe in more downside for risk assets over the medium term,” Mizuho International Plc multi-asset strategist Peter Chatwellwrote in a note to clients.

In the latest developments, Russia’s foreign minister repeated a threat to target arms convoys in Ukraine sent by the U.S. and its allies. President Joe Biden will tell Chinese counterpart Xi Jinping the U.S. will “impose costs” if Beijing backs Russia, in a call planned for 9 a.m. EDT. Here are the key things to watch:

US President Biden will speak with Chinese President Xi at 09:00EDT on Friday, while it was separately reported that President Biden called Russian President Putin a murderous dictator and pure thug.

US President Biden’s administration reportedly hardened its stance towards China ahead of Biden-Xi call on Friday, while officials believe Russia is moving closer to supporting the Kremlin.

Russian Kremlin says that the Russian delegation in peace talks has expressed a readiness to work faster but the Ukraine delegation has not shown a similar readiness, negotiations continue.

Ukraine Deputy PM says nine humanitarian corridors have been agreed for Friday.

Ukrainian Presidential aide Zhovkva says talks with Russia are progressing, but only slowly; will not negotiate an inch of Ukrainian territory.

Russian Foreign Minister Lavrov says Russia’s goal is to remove threats to Russia on Ukrainian soil; any weapons cargo to Ukraine is considered as “fair game” for Russia. A number of countries including China, India, Brazil and Mexico “will not dance to the tune of the United States”, via Sky News Arabia.

Russian President Putin and French President Macron will speak on Friday.

In Europe, the Stoxx Europe 600 Index dropped 0.1% but was set for its best week since November 2020. Retail and miners outperformed, while autos, energy and travel are the worst-performing sectors in European stocks. FTSE MIB outperforms, adding 0.1%, CAC 40 lags, dropping 0.6%. S&P futures decline 0.5%. Investors continued to favor U.S. equity funds in the week to March 16, with $32 billions pouring into the strategy, while all other regions had outflows, according to Bank of America strategists, citing EPFR Global data. U.S. data on Friday include existing home sales, while no major companies are scheduled to report results

Asian stocks steadied after a two-day rally, as investors await the outcome of talks between U.S. President Joe Biden and his Chinese counterpart Xi Jinping on the war in Ukraine later Friday. The MSCI Asia Pacific Index erased earlier losses to trade little changed. The rebound late in the day was led by moves in Chinese stocks, with shares on the mainland ending higher and those in Hong Kong paring declines. China’s benchmark CSI 300 Index flipped from a loss of as much as 1% to gain 0.3% in afternoon trading, with energy and financials leading. The energy subgauge was up 2.6%, financials +2% with Seazen Holdings and Ping An Insurance among the top performers. Walvax and Shanghai Pharmaceuticals top the broader gauge, with sentiment for the sector lifted after Chinese firms signed agreements to make a generic version of Pfizer’s Covid pill. Most other major gauges in the region posted gains.

Investors remain cautious amid concerns Washington may take a tougher stance on China for its muted response to Russia’s invasion of Ukraine, though Beijing denies that it has tacitly backed the war. President Biden is set to speak by phone with Xi on Friday at 9 a.m. in Washington. “I don’t think we can escape from volatility,” said Manishi Raychaudhuri, head of APAC Equity Research at BNP Paribas. “Earlier in the year, we were only dealing with uncertainties surrounding the global central banks’ reaction function to inflation. Now, we also have to deal with geopolitical tensions and we have no visibility how exactly that situation is going to end.” READ: Biden Team Hardens View of China Tilting Toward Putin on Ukraine Japanese stocks gained as the Bank of Japan doubled down on its commitment to continue with stimulus even if inflation continues to accelerate. The rebound in Chinese stocks came as traders speculated the central bank could further ease monetary policy soon, following the authorities’ pledge to stabilize markets. For the week, the MSCI Asia Pacific Index was poised for a 3.9% advance, the best performance in months

In FX, the Bloomberg Dollar Spot Index advanced as the greenback was steady to higher against all Group-of-10 peers apart from the Swiss franc; Treasury yields fell by up to 2bps, led by the long end Commodity-linked currencies apart from the Norwegian krone held up against the dollar while the euro underperformed. Euro options gauges have reached or are very close to the levels seen before Russia’s invasion of Ukraine as traders position for lower geopolitical risks. European benchmark yields fell, led by the short end, and with the core outperforming the periphery. The pound was steady while the Gilts yield curve bull-steepened sharply as money markets pared BOE tightening wagers following Thursday’s dovish hike. The yen headed for a second weekly decline as the Bank of Japan kept its ultra-loose monetary policy while central banks in the U.S. and U.K. raised rates earlier this week. Super-long Japanese government bonds outperformed. Bank of Japan Governor Haruhiko Kuroda doubled down on his commitment to continue with stimulus even if inflation continues to accelerate, in a rebuttal of the need to join a global wave of central banks normalizing policy.

In rates, Treasuries advanced with yields richer by more than 4bp across long-end of the curve, following steeper gains for gilts. 10-year TSY yield was at 2.14% is richer by 3bp vs Thursday’s close vs more than 7bp decline for U.K. 10-year; U.S. 2s10s is flatter by ~2bp with U.K. curve steeper by more than 3bp. The U.K. curve bull-steepened during London session, pricing in lower odds of a 50bp rate hike by Bank of England following yesterday’s dovish turn. Declines for U.S. stock futures also support Treasuries. Three Fed speakers are scheduled during Friday’s session, and St. Louis Fed President Bullard, who dissented from this week’s decision to raise rates by a quarter point in favor of a larger move, said in a statement the policy rate should rise above 3% this year.

In commodities, WTI crude futures fade, trading at around $103 after rising as high as $106.28. Spot gold falls roughly $9 to trade around $1,930/oz. Most base metals trade in the green; LME tin rises 2.3%, outperforming peers.

Looking at today’s calendar, we will get existing home sales and the leading index from the US. In Europe, Italy’s and Eurozone’s trade balances are due. Elsewhere, retail sales for Canada will be published. Now that the Fed blackout period is over, we will hear from Kashkari, Barkin amd Bowman.

Market Snapshot

S&P 500 futures down 0.5% to 4,388.75

STOXX Europe 600 down 0.1% to 449.96

MXAP little changed at 178.10

MXAPJ down 0.1% to 580.94

Nikkei up 0.7% to 26,827.43

Topix up 0.5% to 1,909.27

Hang Seng Index down 0.4% to 21,412.40

Shanghai Composite up 1.1% to 3,251.07

Sensex up 1.8% to 57,863.93

Australia S&P/ASX 200 up 0.6% to 7,294.35

Kospi up 0.5% to 2,707.02

German 10Y yield little changed at 0.39%

Euro down 0.3% to $1.1062

Brent Futures up 1.2% to $107.93/bbl

Gold spot down 0.3% to $1,936.83

U.S. Dollar Index up 0.23% to 98.20

Top Overnight News from Bloomberg

China’s muted response to Russia’s invasion of Ukraine has hardened views within the Biden administration that President Xi Jinping may be moving closer to supporting Moscow as the conflict continues, according to several people familiar with the matter

Chinese President Xi Jinping pledged to reduce the economic impact of his Covid-fighting measures, signaling a shift in a longstanding strategy that has minimized fatalities but weighed heavily on the world’s second-largest economy

Russian President Vladimir Putin told German Chancellor Olaf Scholz that Ukraine is trying to “stall” talks by putting out “more and more new unrealistic demands,” according to the readout of the phone talks from the Kremlin

Russia’s central bank meeting in Moscow on Friday will be little more than a cameo for the Bank of Russia in an economic drama playing out across the world’s biggest country, as the wipeout of household wealth, food shortages and a dash for the exits by foreign companies and Russians shatter three decades of policy making after the Soviet collapse

Russian dollar bonds rose, and the cost of insuring the nation’s debt against default dropped after people familiar with the matter said funds earmarked for interest payments on the Russian government’s dollar notes were sent to the payment agent

China made its biggest push to weaken the yuan through its currency fixings this week as virus-related curbs and rising commodity prices threatened to slow the economy

China sailed its aircraft carrier Shandong through the Taiwan Strait on Friday, Reuters reports, citing an unidentified person with direct knowledge of the matter

Investors in China’s $870 billion of offshore bonds are facing up to the realities of being last in line as borrowers struggle to pay during an unprecedented wave of distress that’s sent defaults to a record

Argentina’s senate approved the government’s $45 billion agreement with the International Monetary Fund on Thursday, clearing the way for its final approval by the lender’s board of directors

Iceland faces a lower risk of speculative money flows because of shifts in global monetary policy after Russia’s invasion of Ukraine, central bank Governor Asgeir Jonsson said

A more detailed look at global markets courtesy of Nesquawk

Asia=Pac stocks eventually traded mostly positive following on from Wall St’s best 3-day gain since 2020. ASX 200 was underpinned by commodity-related sectors including energy after oil rallied over 9% yesterday. Nikkei 225 eked marginal gains amid the lack of fireworks at the BoJ policy announcement Hang Seng and Shanghai Comp. were mixed as tech stocks in Hong Kong faded their mid-week surges and with China said to weigh a Tencent overhaul by separating WeChat Pay from the core business and a new licence requirement. Conversely, the mainland was indecisive with downside cushioned amid further efforts by Chinese press to instill confidence in the equity market and with participants awaiting the Biden-Xi call.

Top Asian News

First Hong Kong-Listed SPAC Has Slow Start In Trading Debut

Taiwanese Crypto Exchange MaiCoin Is Said to Weigh Nasdaq IPO

China Reopening Names Mixed as Pfizer’s Covid Pill Arrives

Shell’s Prelude LNG Export Plant Cleared by Regulator to Restart

European bourses, Euro Stoxx 50 -0.6%, have become incrementally more pressure after a relatively contained cash open, all eyes on the US-China meeting and Fed speak. US futures are similarly pressured, ES -0.6%, but have been somewhat more contained thus far; reminder, today is Quad Witching. Sectors, were initially mixed in Europe but have been drifting lower and are all in negative territory with the exception of some mild support for Defensives.

Top European News

U.K. Regulator Revokes RT’s License to Broadcast in the U.K.

BNP Paribas Upgraded at SocGen on Capital, Shares Decline

Ted Baker Gains as Sycamore Studies Bid for U.K. Fashion Brand

P&O Crew Mutiny After Firing Threatens Biggest U.K. Trade Artery

In FX, Dollar regains poise after post-FOMC demise with DXY pivoting 98.000. Yen still lagging following no change from ultra accommodating BoJ, USD/JPY just shy of 119.00. Euro loses grip of 1.1100 handle where decent option expiry interest starts and ends at 1.1110 (1.44bln). Pound pares some post-dovish BoE hike declines and Rouble was unphased by the CBR keeping rates unchanged after the significant intra-meeting hike; Cable straddles 1.3150 and USD/RUB firmly above 100.0000.

In fixed income, bonds bounced firmly ahead of the weekend as risk sentiment sours and stocks head into quad-witching on a

weak footing. Curves continue to flatten following Fed and BoE tightening. Gilts extend outperformance and recovery gains on a dovish leaning MPC split and guidance.

In commodities, WTI and Brent front-month futures are firmer but off best levels as the complex continues to nurse some of this week’s earlier losses. WTI Apr resides just above USD 104/bbl (vs weekly high 109.72/bbl) whilst Brent May trades hovers around USD 108.00 (vs weekly high 113.15.bbl). UK PM Johnson was unable to secure an agreement with Abu Dhabi and Saudi Arabia to boost oil output after a visit to the region although Downing Street claimed the trip was not about quick fixes, according to Politics Home. LME says some trades have gone through below the Nickel limit, such trades will be cancelled; hit the adjusted limit down of -12%. Spot gold/silver are pressured as the USD retains an underlying bid, eyes on Biden-Xi call.

US Event Calendar

10am: Feb. Existing Home Sales MoM, est. -6.2%, prior 6.7%

10am: Feb. Leading Index, est. 0.3%, prior -0.3%

10am: Feb. Home Resales with Condos, est. 6.1m, prior 6.5m

DB’s Jim Reid concludes the overnight wrap

Morning from Cannes where I want a refund given I haven’t seen the sun yet while it’s apparently barmy hot at home. My hotel is off the beaten track and has a small rooftop pool. I decided to put my gym kit on yesterday and have my lunch sandwich by the side of it as this was a novelty after a long winter at home. Within 2 minutes I was freezing and went back to my room. I should have got the message when no-one else was there. I’m at a big property conference and I have to say the streets were very busy last night as I walked back from giving an after dinner speech. It’s remarkable how quickly normality is returning after Covid.

Talking of normal, we’re running a quick flash poll for a couple more hours this morning as to whether you think this time is different. Normally in first 9-12 months after the start of a Fed hiking cycle equities go up, credit tightens, yields go up and the curve flattens. Will this time be different? We have five one click answers. It took me 7 seconds to complete myself. All help appreciated. The link to the survey is here. Answers in my Chart of the Day (CoTD) later today. If you want to be added to CoTD let me know.

Yesterday was met with a flurry of conflicting headlines about the future prospects of negotiations around the war, with the back and forth reaching frenzied levels after most markets had called it a day. US intelligence warned that President Putin was likely to increase nuclear sabre rattling should the war drag on. This is something that hasn’t come up since three weekends ago so worrying news. Meanwhile, the State Department reported they saw no signs Putin was ready to stop his invasion, dampening hopes of a diplomatic conclusion. On the upside, China’s UN envoy reportedly called for maximum restraint in the Ukraine war, which will hopefully make Russia feel less emboldened.

Earlier in the day the Kremlin and Ukrainian officials had already pushed back on optimistic reports about the state of negotiations. However markets climbed a wall of worry (S&P 500 +1.23%) until the nuclear headlines after the close. As I type, S&P futures are -0.66% down with 10-yr UST yields flattish at 2.174%.

The main moves yesterday centered around crude oil and gilts, which rallied across the curve following the BoE meeting. The Bank Rate was raised another +25bps, but couched in much more dovish communications than we’re used to of late from DM central banks. Meanwhile, oil staged another comeback, with Brent futures gaining +8.79% and advancing another 2% this morning. Finally, Russia’s sovereign bond payments made its way to custodians, which enabled payments to creditors, this helping equities in the US session.

Elsewhere on the conflict, the US is re-upping its military support to Ukraine to the tune of $800 million of new weaponry. President Biden is set to speak with Chinese President Xi Jinping later today about the conflict, where Biden will reportedly emphasize the US will impose costs on China were it to support Russia in the conflict. The US House of Representatives followed through on earlier threats by voting to revoke Russia’s most favored nation status in international trade, enabling the US to impose material tariffs against Russian imports.

Diving into yesterday’s BoE meeting. The central bank hiked by +25bps, as widely expected, becoming the first major central bank to bring its key rate back to the pre-pandemic level and an overview by our UK economist is available here. The lone dissent yesterday was for keeping policy on hold, unlike the February meeting when four dissenters preferred a +50bp rate hike. A big shift. Further, the guidance in the statement implied the MPC was much more concerned about potential drags on growth. That said, the guidance still expects modest further tightening, albeit with risks around that path being much more two-sided than they previously were. Our UK economists maintained their call for further Bank Rate increases at the May, June, and August meetings.

Gilts outperformed across the curve, with 2yrs falling -11.7bps and 10yr gilts dropping -6.6bps to 1.56%, while the pound lost -0.16% versus the dollar and -0.51% versus the euro. Price action in the rest of Europe was more muted, with yields on 10yr bunds (-0.7bps) and OATs (-1.3bps) slightly lower. The commodity rally drove 10yr bund breakevens +3.4bps wider. Nominal Treasury yields were similarly muted, with 10yr yields falling -1.4bps. However, that masks a large pickup in 10yr Treasury breakevens, which gained +13.6bps to 2.94% on the rise in energy costs.

On energy, oil climbed steadily throughout the day, with Brent futures gaining +8.79% and ending their short-lived stint below $100/bbl. No one development discretely drove oil prices, but the negative tone around the conflict as well as heightened volatility in commodity markets contributed. For their part, European natural gas prices gained another +2.56%. French President Macron noted the state may have to take control of some energy firms amid the recent market turmoil. He had backing from the ECB’s Visco who said administered prices would not be a bad idea. Agricultural commodities kept with recent trends and climbed as well, with corn and wheat futures gaining +3.18% and +2.15%, respectively.

Equity markets put in a mixed performance on both sides of the Atlantic. The STOXX 600 gained +0.45%, while the DAX and CAC were mirror images, the DAX falling by -0.36% with the CAC picking up +0.36%. The S&P 500 outperformed, climbing +1.23%, benefitting from the pick up in sentiment following Russia’s bond payment making its way to bond holders. Energy (+3.48%) re-assumed its place as the best performing sector following the jump in oil prices, though every sector ended the day in positive territory.

Overnight in Asia, equity markets are mostly trading lower, after the nuclear headlines. The Hang Seng (-2.43%) is lagging in early trade giving up some of its gains fueled by China’s recent support pledge. In mainland China, the Shanghai Composite (-0.22%) and CSI (-0.89%) are drifting lower, shedding earlier sessions gains while the Kospi (+0.08%) is just above the flatline.

Elsewhere, the Nikkei (+0.28%) is up after the BOJ held steady on monetary policy. In a largely expected decision, the central bank kept its interest rate targets unchanged but warned of heightening growth risks emanating from the Russian-Ukraine war as it stuck with a dovish tone. Additionally, the BOJ downgraded its economic assessment just two months after it was upgraded, due to surging Omicron COVID-19 variant cases.

Earlier today, economic data released showed that Japan’s national consumer price index (CPI) grew +0.9% y/y in February, matching Bloomberg estimates but much higher than January’s +0.5% increase. The strong inflation figures clearly demonstrates signs of growing inflationary pressure from higher energy costs.

If one were looking for evidence of global de-dollarization in oil trade invoicing, yesterday was a setback, as there were reports of Indian refiners buying Russian oil at a deep discount using US dollars, despite speculation a rupee-ruble settlement mechanism would be used. A story to keep an eye on over the longer-term.

Looking at yesterday’s data releases, the Philadelphia Fed business outlook survey showcased a material beat, printing at 27.4 versus expectations of 14.5. US jobless claims came in at 214k, slightly below the expected 220k and lower than the previous revised value of 229k. Housing starts (1769k vs 1700k expected) and building permits (1859k ss 1850k) also beat estimates on the upside. There was no sign of a slowing US economy yesterday.

In today’s data releases, we will get existing home sales and the leading index from the US. In Europe, Italy’s and Eurozone’s trade balances are due. Elsewhere, retail sales for Canada will be published.

Tyler Durden

Fri, 03/18/2022 – 08:06