42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

The Fiscal And Monetary Problem Is Not Hopeless

Authored by Jeffrey Tucker via The Epoch Times,

A major factor in public ignorance of economics is the manner in which economic forces transcend politics. These days, if something is going on of some major sort that seems either out of the control of politics or involves both major political parties, it is easily disappeared from public life.

{kind=link}

That is the very essence of the inflation problem that has so seriously harmed the American standard of living. In the best estimate, the purchasing power of the dollar has fallen some 20 percent over four years. But depending on what you buy, or decline to buy simply because it is too expensive, the dollar could have lost 30 percent or even 50 percent depending on how one measures these things.

How and why did this happen? Economists for many hundreds of years have attempted to point to the real source. Nobel Prizes have been given out for sweeping and deeply empirical studies trying to show this. Reduced to its very essence, the problem of inflation traces to the money stock. If it expands more quickly than economic output, the value of all existing units of money will decline.

This is a law of nature, like gravity. There are complications within the law, of course, such as the precise mechanism by which newly created money lands in people’s bank accounts and is spent. There are other ways the scenario could unfold. Banks could hold the new money and not lend it out (2008 and following) or people could stuff new money in their mattress (1932 and following) thereby reducing money velocity.

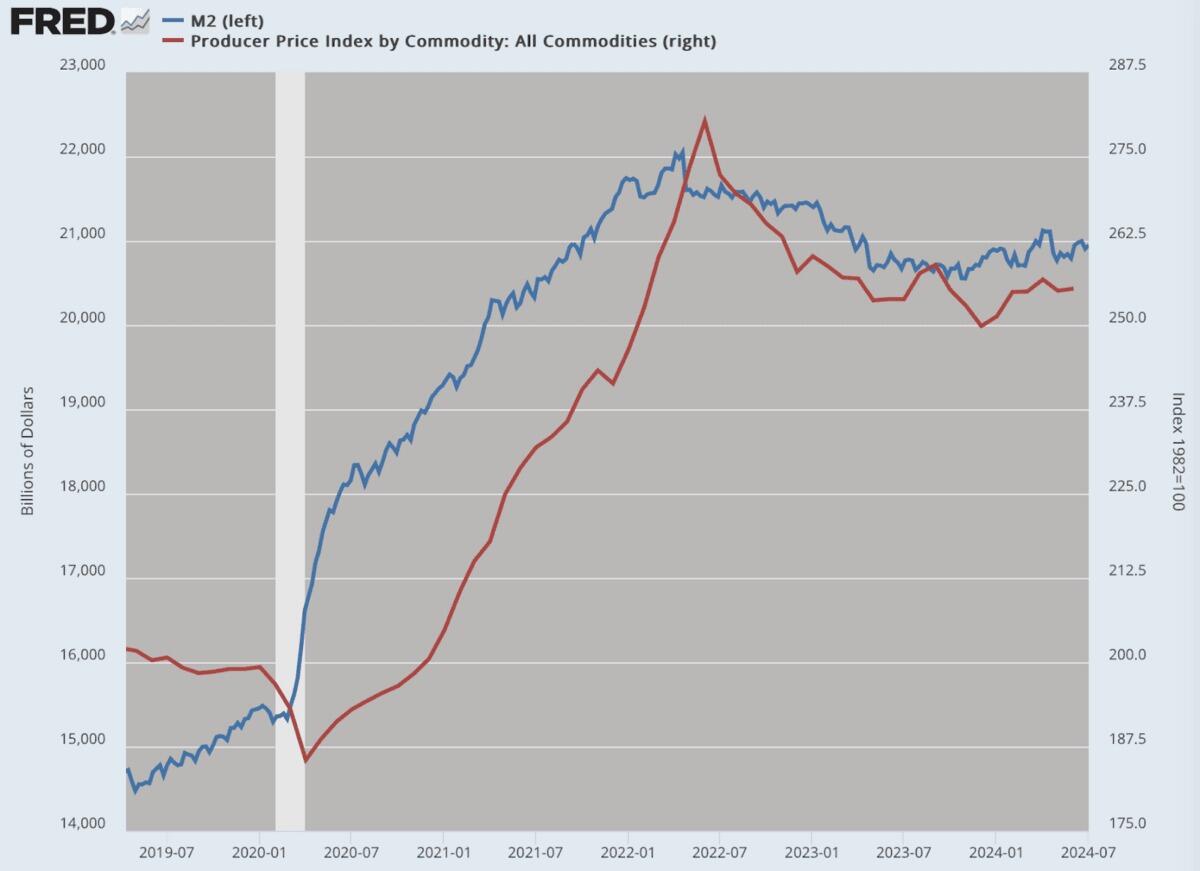

Still, by and large, and over the long term, the price level reflects the money stock. The last four years have provided a near-perfect demonstration of that fact. We can see it by overlaying M2 (the most accurate measure of the stock of money we have) with the price of commodities purchased by producers (which are unchanged in quality and not subjected to crazy adjustment schemes). The result shows the direct relationship: prices respond to the expanded money stock with a time lag.

{kind=link}

(Data: Federal Reserve Economic Data (FRED), St. Louis Fed; Chart: Jeffrey A. Tucker)

To be sure, there are other moving pieces. Deficit spending by Congress is what prompts the Treasury Department to issue the debt that the central bank (Federal Reserve) buys with computer entries (money printing). Without that step, the Fed would likely be called upon to intervene. But when the debt explodes, it cries out for a market of buyers. The Fed is there to pick up the tab. The result is an expansion of the money stock.

Simple, right? I think so. One might suppose that this would be common knowledge. It is not. This is because we have propagandized for many decades that the central bank is the solution and not the cause of inflation. Yes, it is frustrating. But such is the nature of the world around us. Truth usually takes a back seat to political opportunism and institutional protection.

Based on what I’m able to discern from existing data, it appears to be that the inflation problem (for now) has largely stopped getting worse at a fast rate. Writing in the summer of 2024, it does appear that annualized inflation is running at a rate consistent with the pre-lockdown past, at or below 2 percent. That does not mean that money is growing more valuable. It means that it is losing value at a rate far more slowly than in the most recent history.

That said, we all need to disabuse ourselves of the possibility that prices will go back to 2019 levels. The damage is done. The standard of living has been deeply harmed. It is what it is and nothing will change that. To be sure, there are ways to drag the price level back but that would require a dramatic deflation. That would simply never happen, not under present conditions. All we can really do is accept this sad reality and move on with our lives.

People are only now fully realizing what this inflation, even if it is stopped now, has done to their bank balances. The pain arrives every time you go to the store. If you have to replace some household appliance or a car, there is nothing but shock. Things are simply not adding up. A middle class income is now not enough. It’s a shocking reality and just now fully dawning on people. The media has been trumpeting a mythical recovery that does not exist.

That’s not to say that there are no answers to improving our future. In some ways, the Trump team is correct to put the focus on one answer: a freed-up energy sector that enables more drilling and refining. There are oceans of wealth under our feet. Its extraction has been seriously throttled by the Biden administration in the name of climate control, if you can believe it. Reversing those policies will indeed drive down the price of oil and gas and make transportation more affordable.

That will put downward pressure on prices. That would be much welcome. That said, a lower price for oil also reduces profitability and calls forth a reduction in drilling. It’s supply and demand. The only way to overcome this is dramatic deregulation that has some permanence to it, which is to say, a big regime change that becomes the new normal and cannot be reversed in four years by a new administration. That’s not easy.

The only great challenge is the fiscal problem. The reason the Fed swung into action is entirely traceable to Congress and the wild spending that took place from 2020 and following. The resulting debt has to be dealt with somehow.

I’m not among those who say that it can never be paid. Even awful fiscal problems are fixable with the right steps. The problem is that the steps absolutely must include dramatic spending cuts, meaning 1 to 2 percent of GDP for starters or about $280–500 billion, which is not even on the table.

It could happen just like what happened in Argentina. The new president elected only last year slashed the budget and incredibly fixed the fiscal problem almost immediately. If you have high economic growth and a dramatically shrinking federal budget, plus mass deregulation, you inspire investors, lenders, consumers, and everyone. Even seemingly intractable problems can be made to evaporate rather quickly.

The trouble is that there is very little political will in this country right now to cut the budget. And by cut, again, I don’t mean cuts in the rate of increase, like Washington language always says. I mean real cuts with whole agencies being made to disappear, dozens of them instantly. Doing this is entirely possible with political will. But I’ve yet to see any evidence that such will exists in the United States today.

Argentina had to reach the point of full collapse before the population was ready to try radical solutions. But those solutions have so far worked. It would be wise and smart to pursue the solution before the emergency hits.

For now, it seems like the inflation problem is not going to get dramatically worse. The damage is done and you feel it every time you go out shopping. This is our new reality. The money supply is relatively flat to gently rising so we can expect continued low rates of inflation using the existing price structures as the benchmark.

That said, everyone should be worried about this idea of September rate cuts. Yes, everyone would welcome lower rates on mortgages and credit cards. But with that comes a loosening of money aggregates and a genuine risk of restarting the inflationary fires. The Fed still sits on a massively ballooned balance sheet with a monetary base in the range of $6 trillion. This has some serious inflationary potential.

Remember what happened in the 1970s. There were fully three waves before the final horror hit in 1979-80. Is this our future? It does not have to be.

Tyler Durden

Tue, 07/30/2024 – 19:00