42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Biden Ouster Sparks Some ‘Trump Trade’ Unwind, Big-Tech & Bond-Yields Bounce

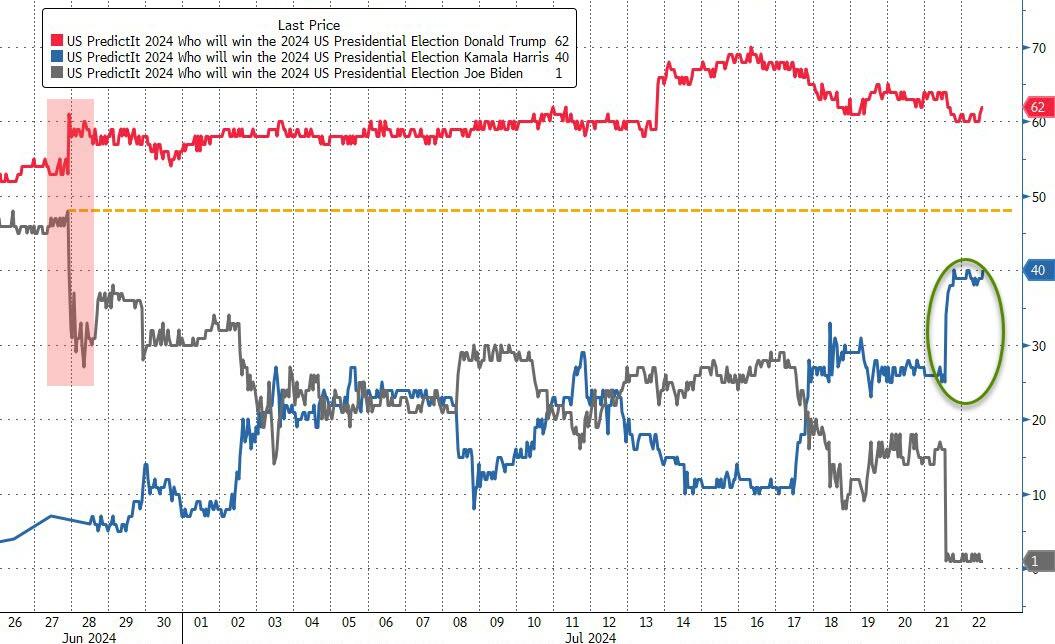

President Biden’s removal from the ticket for the 2024 election sent Kamala Harris odds of winning in November soaring (but we note she remains below the pre-debate levels that Biden had reached)…

{kind=link}

Source: Bloomberg

In response, US Equities are bullishly trading “DC gridlock”, as Nomura’s Charlie McElligott suggests the downstream Democrat elections odds in House races are being perceived as having greatly improved their win probabilities post the party coup removal of Biden…

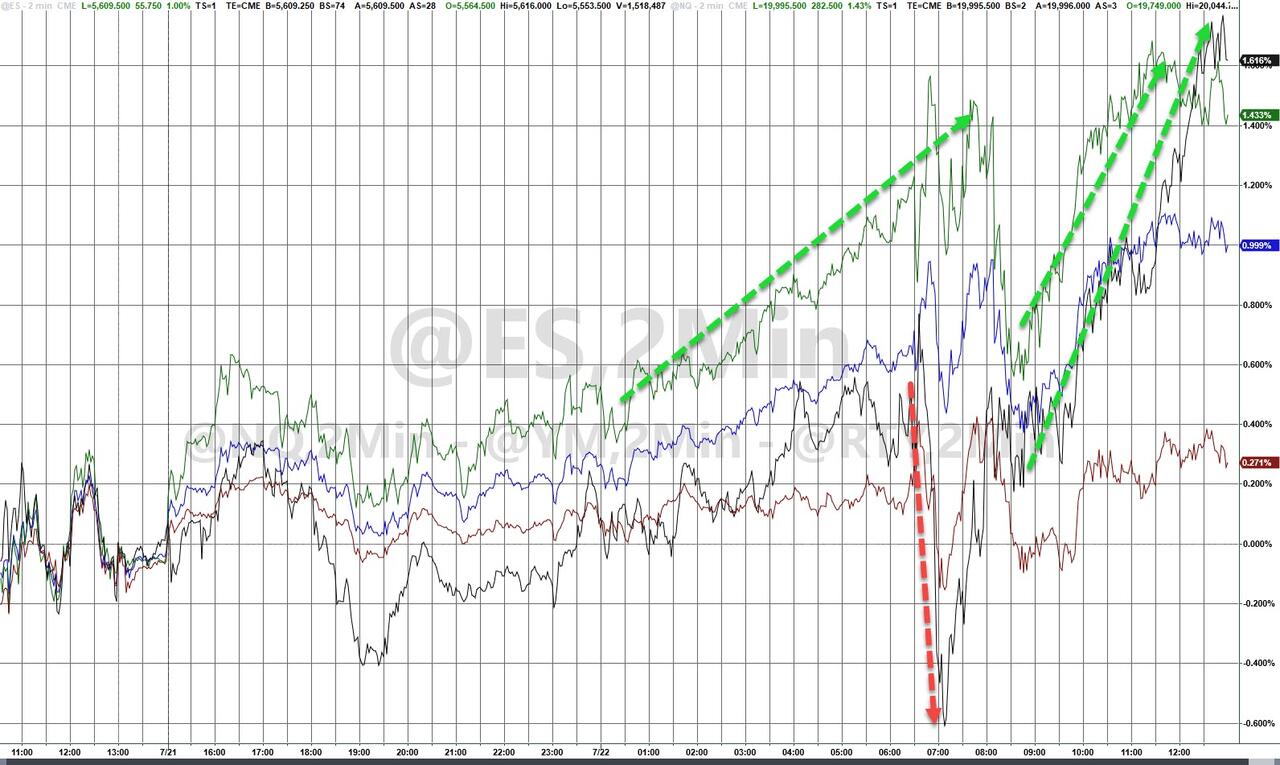

All the majors were higher today led by Small Caps and Mega-Cap tech. The Dow lagged, but ended green…

{kind=link}

…while so-called “Trump trades” like cyclical–type sectors come under some modest pressure (Energy and Materials as S&P’s worst perf sectors)…

{kind=link}

Source: Bloomberg

Mega-Cap tech and China ADRs (rate-cut) also ripped (in trump-trade-unwind-style)…

{kind=link}

Source: Bloomberg

However, any ‘Trump trade” unwind is NOT evident in bond-land…

{kind=link}

Source: Bloomberg

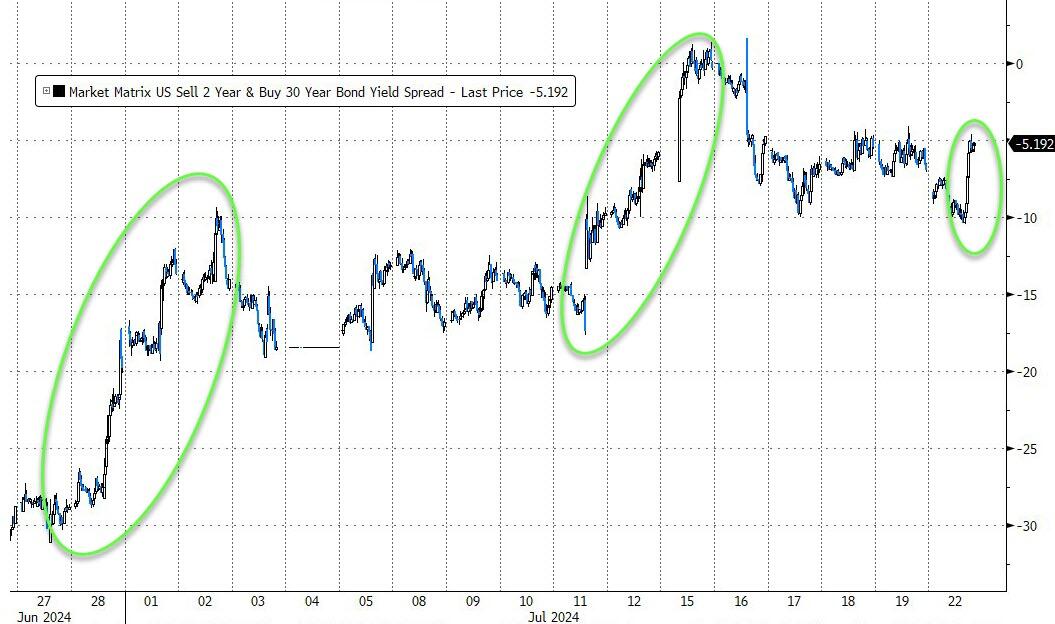

…with the curve bear-steepening (as we would expect because Trump’s “fiscal overstim / deregulation” bearish outcomes for Bonds are more problematic for the long-end of the curve)…

{kind=link}

Source: Bloomberg

Which suggests, perhaps the equity gains are due to other issues…

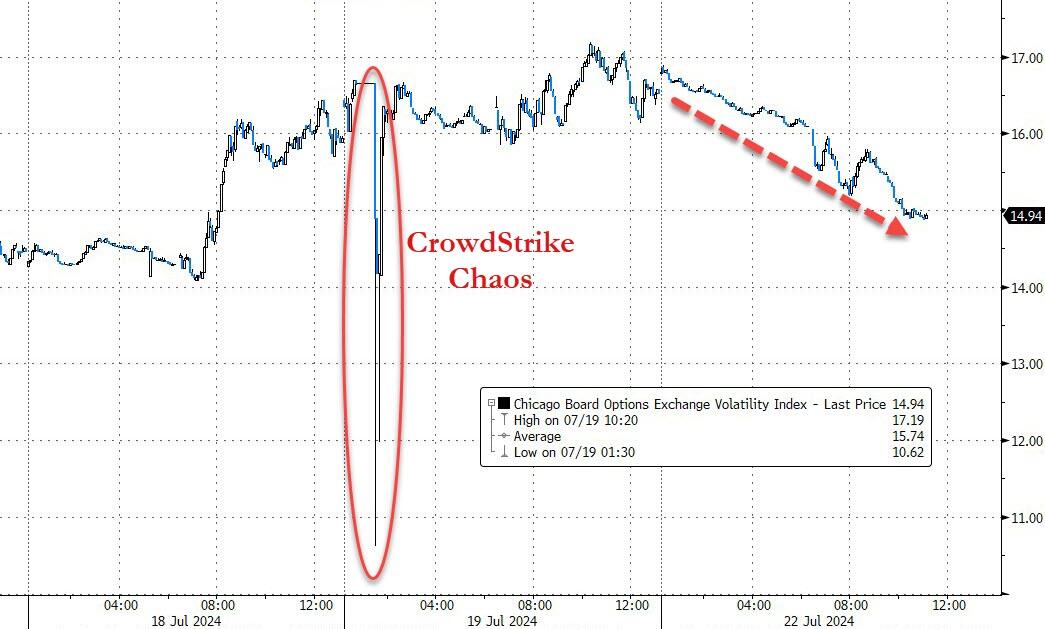

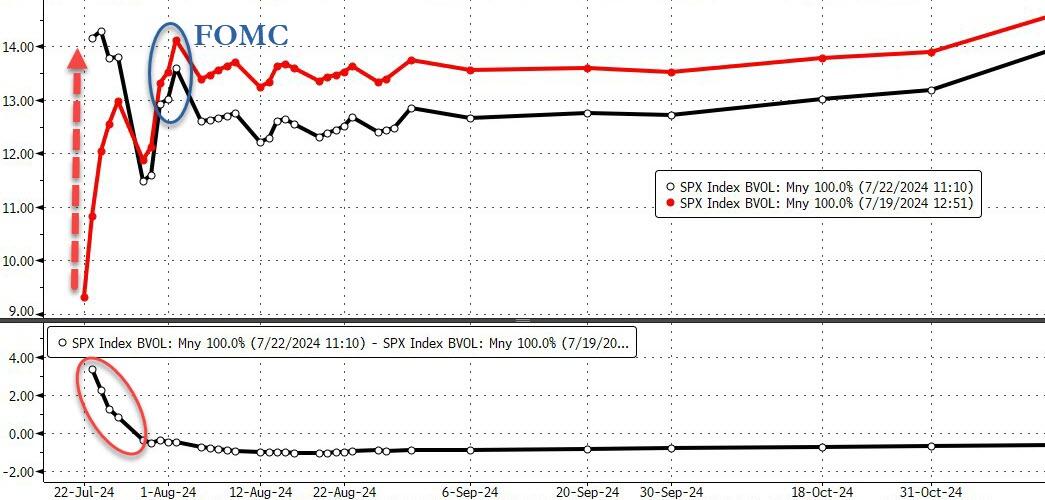

As McElligott points out, another catalyst within this stocks rally resumption is the opportunity provided by last week’s predictable “Vol reset” after having overshot “too low” in prior weeks…

Arguably, we are seeing some relative election stability forming (we seemingly now have our candidates, fake democracy be damned) which, as already mentioned, looks increasingly “gridlock” / split outcome for DC which markets thrive in…

We had the “Vol reset” last week with implieds squeezed to relative highs, Skew at multi-month highs, VVIX at multi-month highs…which then provides quite a “Short Vol / Short Skew / Short Correlation” opportunity for the post Op-Ex snapback rally to gain further legs, even despite all the boogeyman of the Vol bottoming / bullish VIX seasonality into August which was a further contributor to last week’s de-risking movement…

{kind=link}

Source: Bloomberg

While VIX is lower, very short-dated vol is elevated as the distribution of market outcomes broadened-out as evidenced by the demand for Tails, especially as the shock turn of political dramas coincided with increasingly “Correlation 1” de-risking experienced at the peak of last week’s Equities trade, with Longs and Shorts both going lower in unison at one point, with Nets being absolutely SLASHED in a monster de-grossing

{kind=link}

Source: Bloomberg

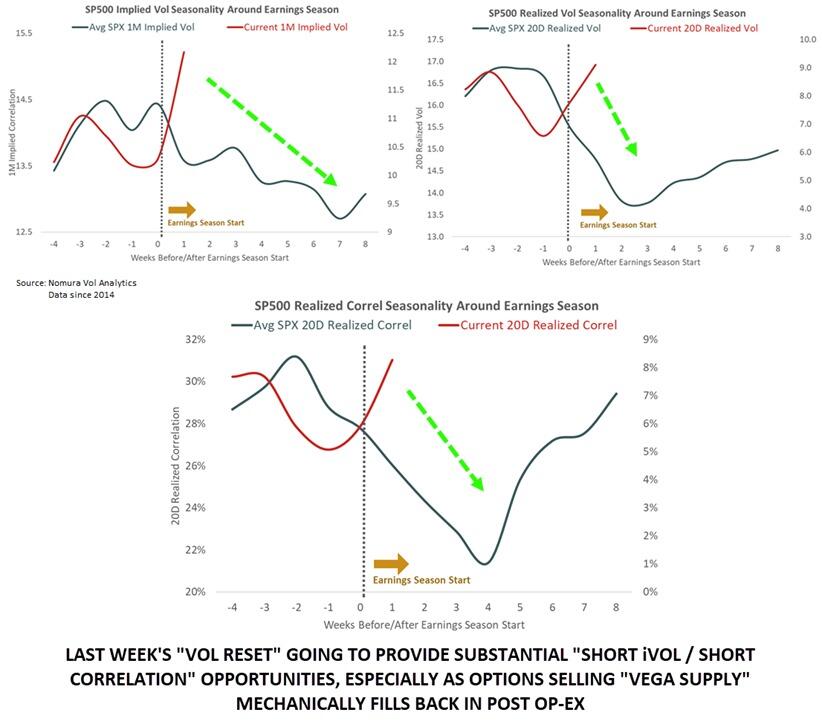

And all of these “calming” inputs most critically are occurring into the “meat” of Earnings season kicking-off with big Tech releases concentrated over the next two weeks, which, as McElligott notes, means we tend to see a large “Dispersion” effect, as Correlation goes lower (Earnings “winners and losers” going in opposite directions) and contributing to further Vol decline…while too, the “mechanical” overwriting and systematic “Vega supply” has not changed either, as the assets keep doing their thing…

{kind=link}

Source: Nomura

The Nasdaq/Russell 2000 pair found support in its nine-month range and bounced today…

{kind=link}

Source: Bloomberg

Goldman’s trading desk notes that overall activity levels are down very modestly from their recent averages, but the floor tilts -10% better for sale (that ranks 95th %-ile), driven exclusively by LOs

LOs are -33% better for sale taking profits in every sector, ex Comm Svcs (+10% better to buy there). Selling is most pronounced in Tech, HCare, Fins & Energy. The overall supply skew in Energy, Fins and HCare rank in the 94th-96th %-iles.

HFs are basically paired buy vs. sell. Demand is balanced across Comm Svcs, REITs, Energy & Mats, while supply is balanced across Fins, Cons Disc & Macro Products. ETF turnover at 34% of tape vs 29% ytd avg tells you fast money hedges moving around more actively today.

Away from bonds and stocks, it was relatively quiet.

Gold drifted modestly lower, erasing the post-CPI gains…

{kind=link}

Source: Bloomberg

The dollar went sideways….

{kind=link}

Source: Bloomberg

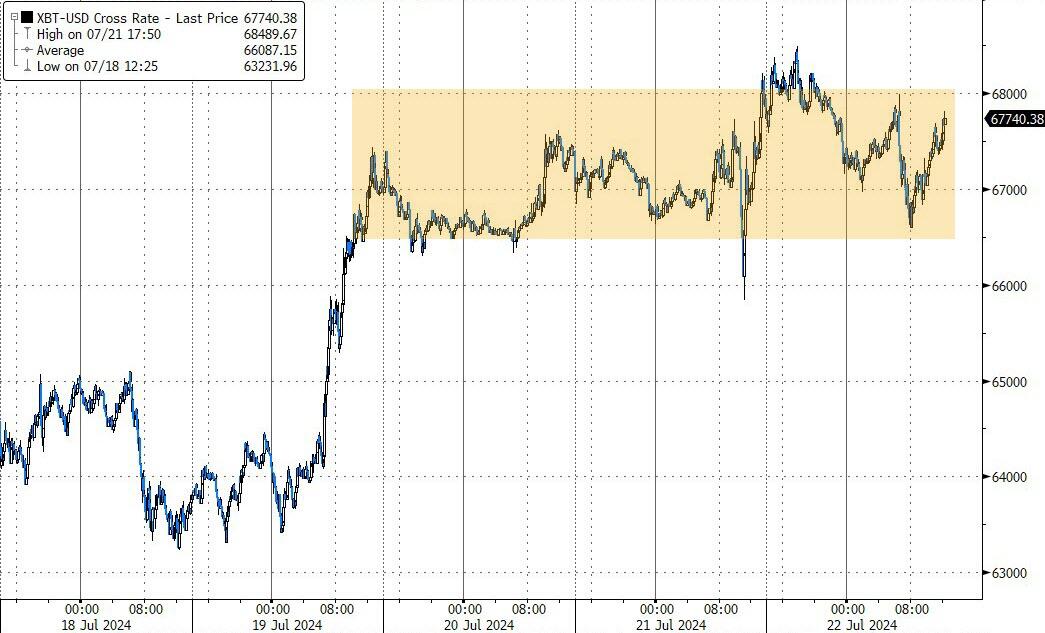

Bitcoin chopped around between $67k and $68k, holding on to Friday’s gains (another example of NOT unwinding the Trump trade)…

{kind=link}

Source: Bloomberg

Oil actually extended its trend lower though with WTI back below $80…

{kind=link}

Source: Bloomberg

Yields were higher on the day – quite uniformly rising into and across the European close…

{kind=link}

Source: Bloomberg

As, rather notably, rate-cut expectations continue to slide lower (with all 2025 dovish gains post-CPI erased)…

{kind=link}

Source: Bloomberg

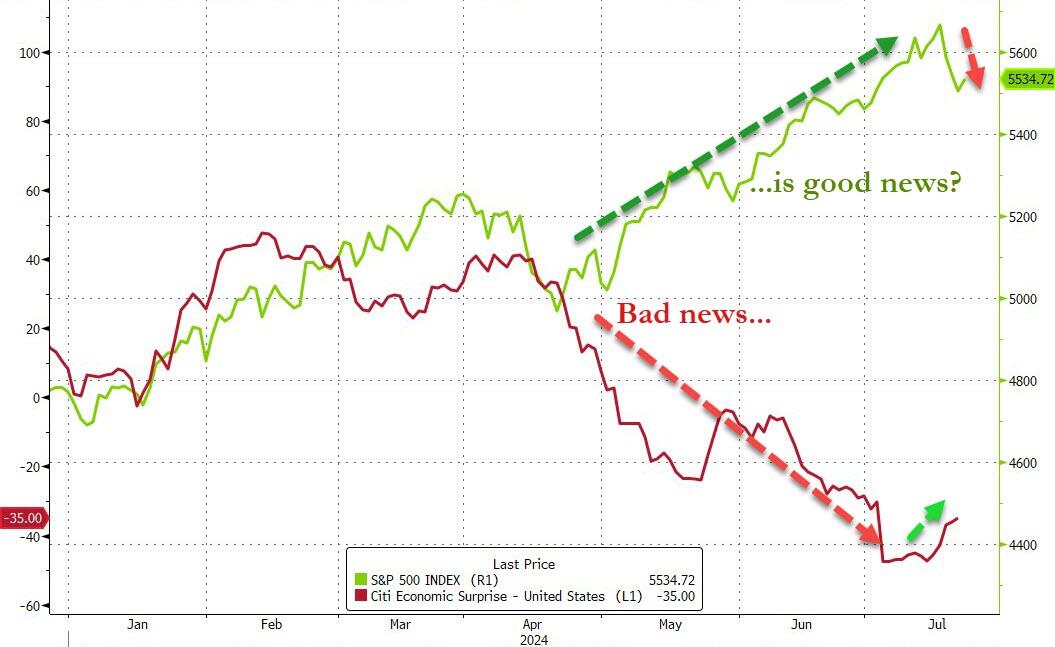

Finally, the ‘bad news is good news’ trade appears to in opposite land for now as ‘good economic news has recently been bad news for stocks’…

{kind=link}

Source: Bloomberg

Will some certainty about the 2024 election reassert the old trend?

Tyler Durden

Mon, 07/22/2024 – 16:00