42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

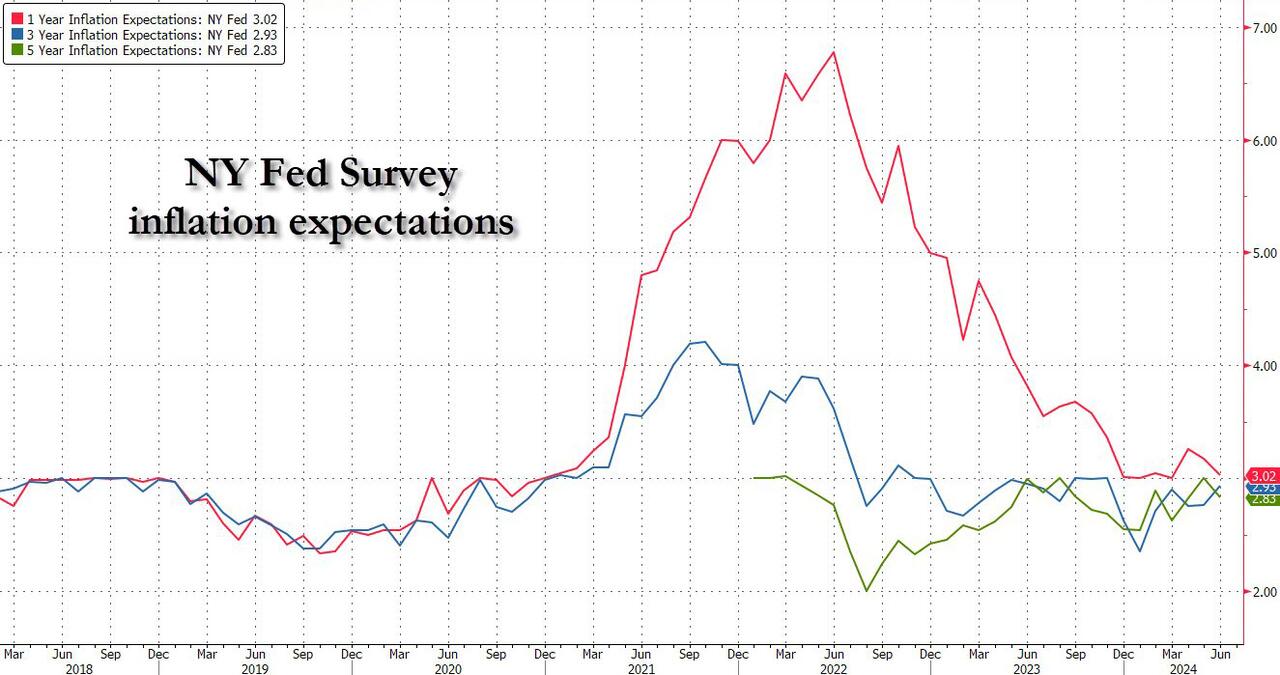

Short-Term Inflation Expectations Slide In NY Fed Survey Despite Earnings Growth Optimism

Inflation expectations at the one-year horizon dropped for the second month in a row, sliding to 3.02% in June from the previous month’s 3.17%, and from a 2024 high of 3.26% in April, according to the New York Fed’s survey of consumer expectations. At the same time, 3 year inflation expectations rose modestly to 2.93% (up from 2.76%) and the highest since Nov 23. Finally, the median five-year ahead inflation expectations also dropped to 2.83% after hitting a one-year high of 3.00% in May.

{kind=link}

Some more details from the survey: disagreement across respondents (the difference between the 75th and 25th percentile of inflation expectations) remained unchanged at the one-year ahead horizon, declined at the three-year-ahead horizon, and rose at the five-year ahead horizon. Median inflation uncertainty—or the uncertainty expressed regarding future inflation outcomes—declined at the one- and three-year-ahead horizons, but rose at the five-year-ahead horizon.

The survey affirms other recent data showing that inflation decelerated in recent months after being more stubborn than expected in the first quarter of this year. Thursday’s CPI report is expected to show that the core consumer price index, which excludes food and energy costs, rose 0.2% in June for a second month. That would mark the smallest back-to-back gains since August, a pace closer to what Fed officials would like to see.

{kind=link}

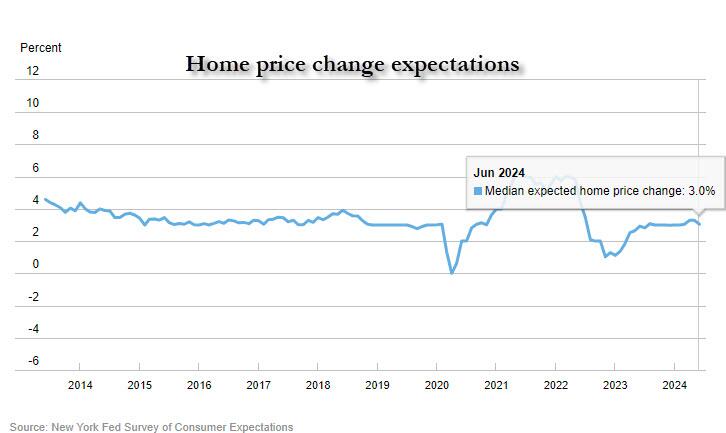

Median home price growth expectations decreased to 3.0% from 3.3%, back to the series 12-month trailing average.

{kind=link}

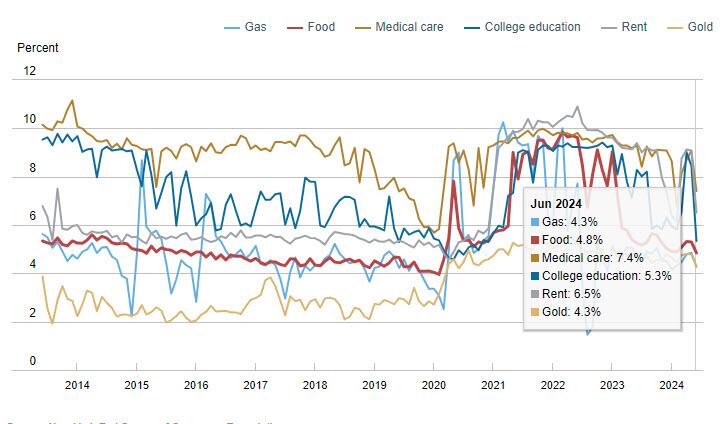

What was more notable is that median year-ahead expected price changes decreased for all goods in the survey: by 0.5% for gas to 4.3%, 0.5% for food to 4.8%, 1.7% for the cost of medical care to 7.4%, 2.6% for rent to 6.5%, and 3.1% for the cost of a college education to 5.3% (the series’ lowest level since December 2020).

{kind=link}

Turning to the labor market we find the following:

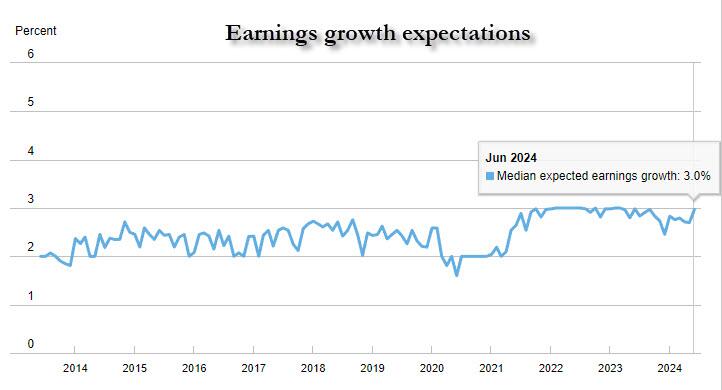

Median one-year expected earnings growth surprisingly increased to 3.0%, “the measure’s highest reading since Sept. 2023”, even though wage growth continues to slide.

{kind=link}

Mean unemployment expectations—or the mean probability that the U.S. unemployment rate will be higher one year from now—declined by 1.0 percentage point to 37.6% in June, just below the series 12-month trailing average of 37.7%.

The mean perceived probability of losing one’s job in the next 12 months increased by 2.4 percentage points to 14.8%. Since the beginning of the year, the series has been moving within a relatively wide range between 11.8% and 15.7%. The mean probability of leaving one’s job voluntarily in the next 12 months also increased (by 0.9 percentage point) to 20.5%, above the series 12-month trailing average of 19.0%.

The mean perceived probability of finding a job (if one’s current job was lost) increased to 53.4% from 52.2% in June, the measure’s highest value since January 2024 but well below its February 2020 pre-pandemic level of 58.7%.

Finally, looking at expectations about household finance, here are the main findings:

Median expected growth in household income declined 0.1 percentage point to 3.0% in June. The series has been moving within a narrow range of 2.9% to 3.3% since January 2023 and remains above the February 2020 pre-pandemic level of 2.7%.

Median household spending growth expectations rose by 0.1 percentage point to 5.1%. The series had remained stable between 5.0% and 5.3% since August 2023, and remains well above its February 2020 pre-pandemic level of 3.1%.

Perceptions of credit access compared to a year ago deteriorated slightly with a smaller share of respondents reporting that it is easier to obtain credit than 12 months ago. Consumers were slightly more polarized about future credit access with a larger share of respondents expecting tighter credit conditions a year from now, and a larger share of respondents expecting looser credit conditions.

The average perceived probability of missing a minimum debt payment over the next three months rose by 0.3 percentage point to 12.3%, above the series 12-month trailing average of 12.1%.

The median expected year-ahead change in taxes (at current income level) increased by 0.4 percentage point to 4.3%, above the series 12-month trailing average of 4.1%.

Median year-ahead expected growth in government debt was unchanged at 9.3%.

The mean perceived probability that the average interest rate on saving accounts will be higher in 12 months decreased by 1.7 percentage points to 25.3%.

Perceptions about households’ current financial situations deteriorated slightly with more respondents reporting being worse off than a year ago, and fewer respondents reporting being better off. Expectations about households’ year-ahead financial situations were less dispersed with fewer respondents expecting to be better off a year from now ago, and fewer respondents expecting to be worse off.

Finally, while earnings optimism may be thoroughly unjustified, at least consumers were somewhat more sanguine about where stocks – which are making new all time highs every day – are going next. Here, the mean perceived probability that US stock prices will be higher 12 months from now declined by 1.3 percentage points to 39.2%.

{kind=link}

Source: NY Fed

Tyler Durden

Mon, 07/08/2024 – 12:05