42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

A $1 Trillion Reason Why The Yuan Won’t Collapse

By Ye Xie, Bloomberg Markets Live reporter and commentator

The talk about a Chinese recession gets louder by the day. Foreign capital is leaving in droves. The yield premium that the nation’s bonds have been enjoying for over a decade is disappearing.

Yes, there are no shortage of reasons to be bearish on the yuan. But the massive dollar holdings accumulated by China Inc. suggest large currency depreciation is unlikely.

About 373 million people in 45 cities including Shanghai are now under full or partial lockdown, making up 40% of China’s GDP, according to Nomura. In less than a week, Premier Li Keqiang issued a third warning about economic growth risks, adding a sense of urgency to Beijing’s push to counter the slowdown via infrastructure spending and monetary easing.

The resulting policy divergence with the U.S. is undermining the support for the yuan. U.S. 10-year yields have risen above the Chinese counterpart for the first time in more than a decade, dimming the allure of the nation’s assets. But that’s not necessarily a game changer, as Macquarie Capital economists Larry Hu and Xinyu Ji point out. After all, the persistent narrowing of the yield differential last year didn’t stop the yuan rally, thanks to hefty exports.

That said, it does look like there is a tight correlation between foreign bond flows and the nominal yield differential. This chart shows the spread versus the six-month change in foreign bond flows. It is perhaps not just a coincidence that foreign investors sold their holdings of Chinese government bonds by the most on record in March, even though the nation’s real yields remain comfortably higher than U.S. peers.

{kind=link}

In addition to weakening capital flows, the other pillar that has been supporting the yuan is also becoming less robust. Exports are expected to rise 13% in the year through March, rebounding from a holiday-impacted February. While still decent, the growth rate is slowing from a clip of more than 20% last year. The shutdown in Shanghai, the world’s largest port, since late March won’t help the April figure.

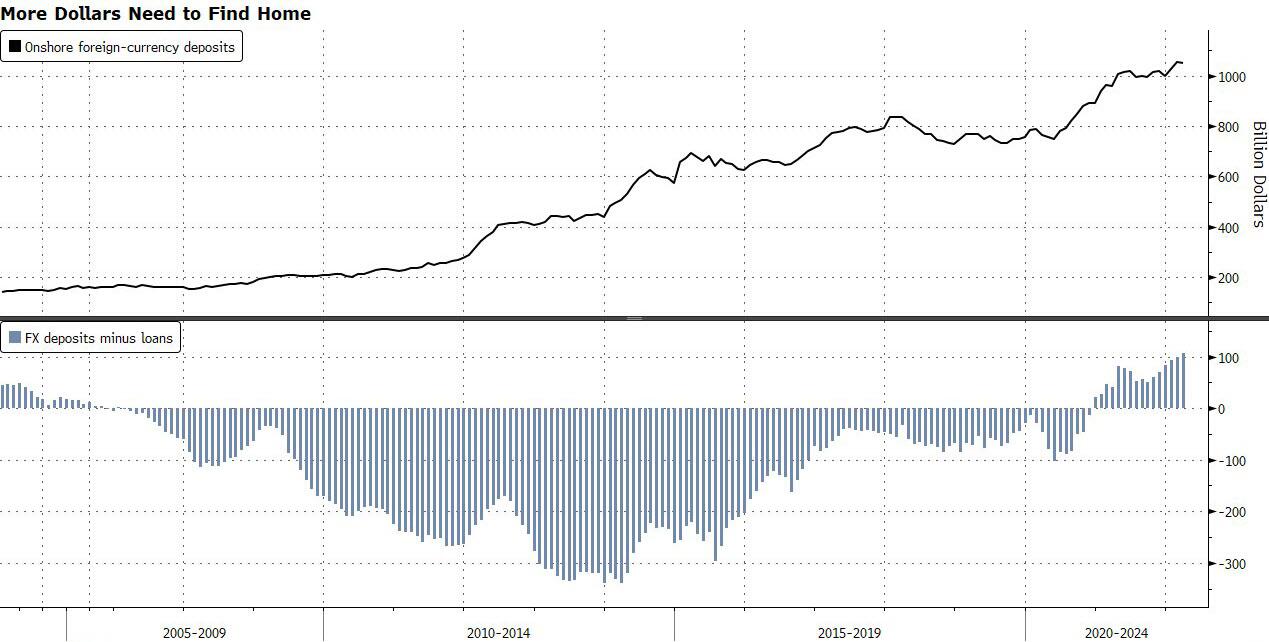

But before one gets too bearish on the yuan, it’s worth pointing out that Chinese exporters haven’t converted all their dollar receipts into local currency since the pandemic started two years ago. Far from it. Foreign-currency deposits have swelled to $1 trillion — a whopping 39% increase from the end of 2019. These extra dollar savings may come in handy if the yuan starts to depreciate.

{kind=link}

Exporters have exhibited a counter-cyclical pattern when converting their overseas dollar receipts. When the yuan weakens, they sell more of their dollar revenues for the yuan at a cheaper exchange rate. And vice versa. This chart shows that the level of exporters’ currency-conversion ratio tends to move in tandem with three-month changes in the dollar-yuan exchange rate. Effectively, China Inc. behaves as an stabilizer in smoothing out the currency volatility.

{kind=link}

All told, the peak of the yuan is probably behind us. That’s not to say that betting on yuan depreciation is a no-brainer. China Inc. has enough firepower to take the other side of the trade.

Tyler Durden

Tue, 04/12/2022 – 23:45