42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

All Hiking Cycles That Invert The Curve Lead To Recessions Within 1 To 3 Years

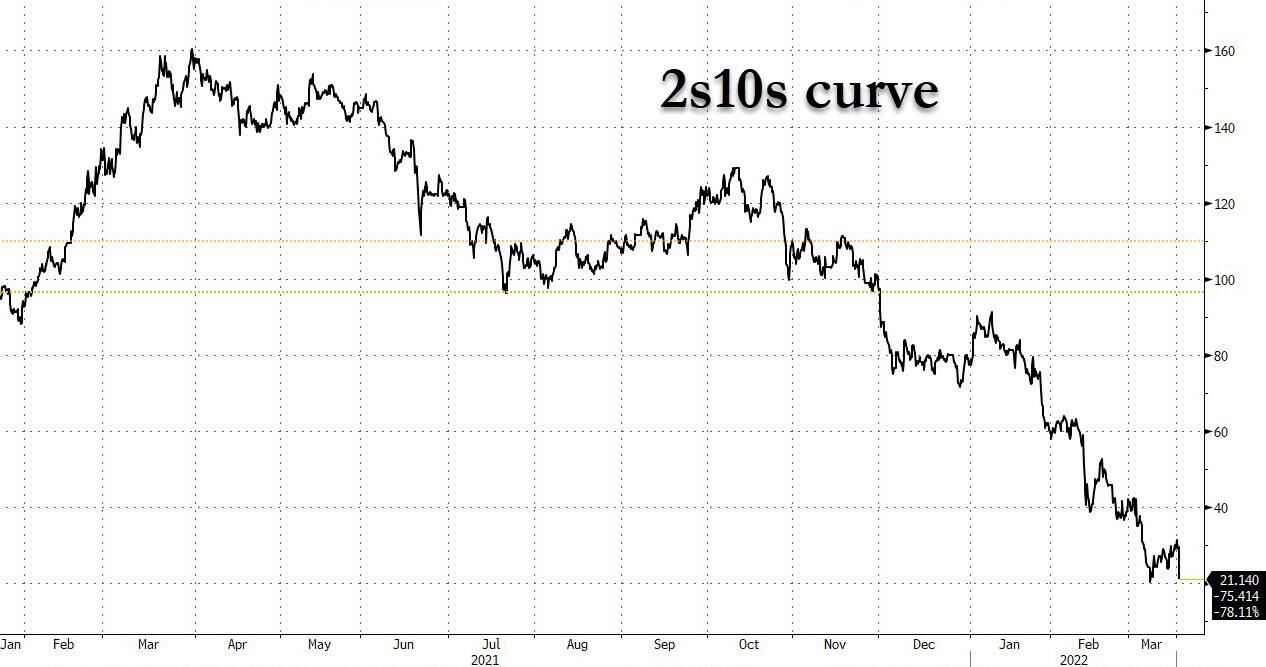

Echoing our earlier thoughts that the Fed officially started the countdown to the next recession (and rate cuts) when it inverted the 5s10s moments after Powell starting speaking, DB’s Jim Reid writes that while not every Fed hiking cycle leads to a recession, all hiking cycles that invert the curve have led to recessions within 1 to 3 years. And the problem with the Fed hiking cycle that starts today, he adds with a ZH-esque does of skepticism, is that “there is a decent likelihood that the curve inverts relatively early on. 2s10s peaked at +157.6bps last March and traded as low as +21.9bps last week before settling at around +30bps as we go to print.”

{kind=link}

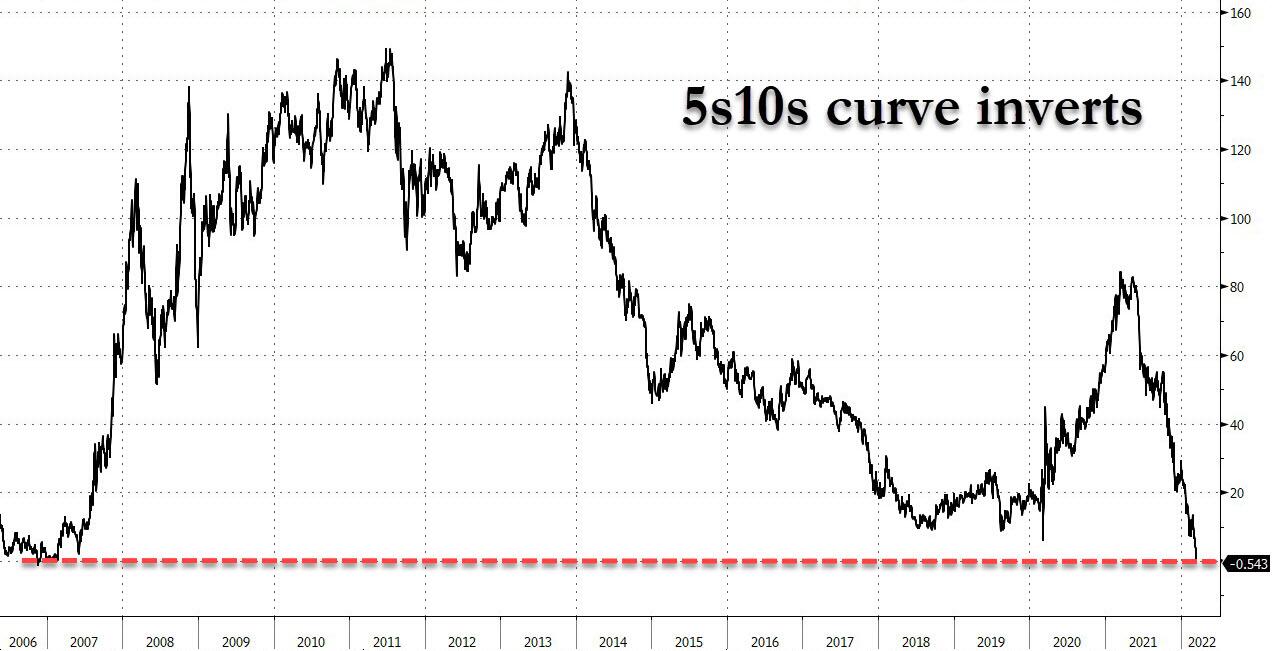

As a reminder, while not as popular as the 2s10s, the 5s10s is also a harbinger of recessions, and usually precedes the 2s10s inversion by weeks. It is this curve that inverted today.

{kind=link}

Piling on, CPI is much higher today than it was in any of those instances, and indeed the second highest at the start of any post-war hiking cycle. Thus, according to Reid “there is not only a strong risk that the curve inverts relatively early, but that the Fed will need to continue hiking anyway.” A few days ago, we phrased it differently: the Fed wants to push the US economy into a modest recession. The only problem is that the Fed has never been able to achieve such a delicate achievement, and the most likely outcome is a violent slowdown coupled with a quick easing of monetary policy, i.e., a policy error… precisely why risk assets soared later in the day.

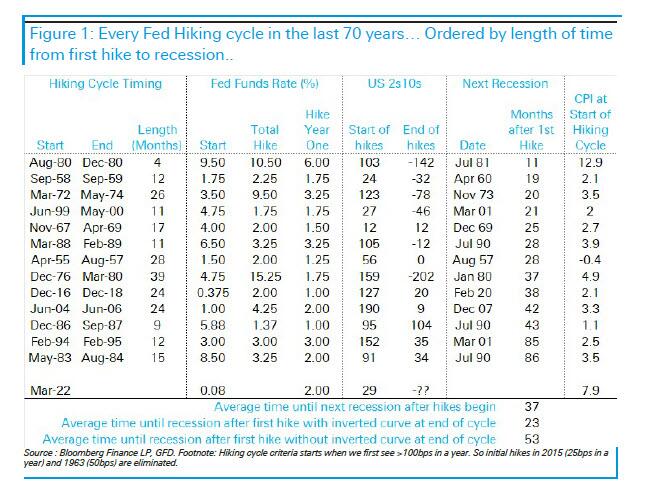

That said, the table from DB below shows the details of every Fed hiking cycle over the last 70 years alongside the time to recession, yield curve shape, and inflation at the first hike. Reid has ordered this by length of time from first hike to recession to demonstrate that the quickest recessions following hikes were associated with an inverted curve by the time the Fed stopped hiking.

{kind=link}

As shown, on average it takes around three years from the first Fed hike to recession. However all but one of the recessions inside 37 months (essentially three years) occurred when the 2s10s curve inverted before the hiking cycle ended. With all the recessions that started later than that, none of them had an inverted curve when the hiking cycle ended. In fact, hiking cycles that ended with the curve in positive territory saw the next recession hit 53 months on average after the first rate hike, whereas the next recession for hiking cycles that ended with an inverted curve started on average in 23 months, just under two years. All these cycles eventually saw an inverted curve but this happened after the Fed stopped hiking.

As a reminder, none of the US recessions in the last 70 years have occurred until the 2s10s has inverted. On average it takes 12-18 months from inversion to recession. Then again, the Fed has never before started a rate hiking cycle when inflation was already 7.9%.

Reid concludes that, “this all fits in with my view in “Roadmap to the next Recession” that 2022 is unlikely to be a US recession year but that late 2023 or early 2024 are high risk.” While we agree that a recession is inevitable, we would add that it will come well before “late 2023”, not only because the 2s10s will invert in a few days at this rate, but because as the record collapse in the fwd OIS curve – which was trading at -49bps as of late Wednesday – signals, the market is now pricing in almost two full rate cut in the fwd 1-3 year window, a number which will only grow with every incremental rate hike by the Fed.

{kind=link}

Tyler Durden

Wed, 03/16/2022 – 20:30