42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Bonds, Bitcoin, & Big-Tech Battered As US ‘Misery’ Reaches 40 Year Highs

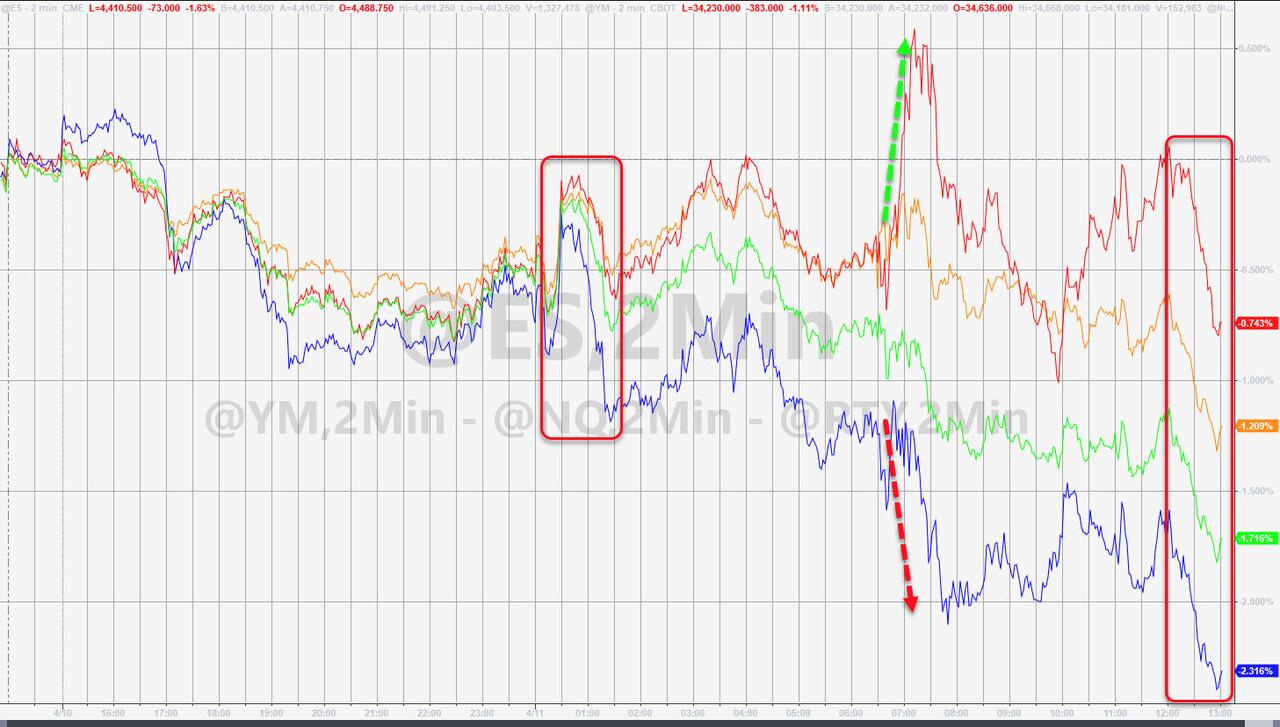

Despite no economic data and minimal fresh news, Tech wrecked again today as yields rose and hawkish FedSpeak abounded. Late in the day, everything puked (all US majors and crypto) on new news catalyst as they broke technical levels. Nasdaq was the ugliest horse in the glue factory while Small Caps ‘outperformed’ the rest (but were still red, unable to hold unch late on…

{kind=link}

Defensives and Cyclicals were equally smacked today but Growth was puked relative to Value, now down dramatically since last Monday’s upside spurt…

{kind=link}

Source: Bloomberg

All the majors broke below their 50DMAs…

{kind=link}

Of course, the big headlines in equity-land were from TWTR and Elon Musk as he rejected a board position, sparking speculation that he will bid for a bigger stake in the progressive-hegemon. After an initial 5-6% tumble, TWTR ended 3.5% higher on the day

{kind=link}

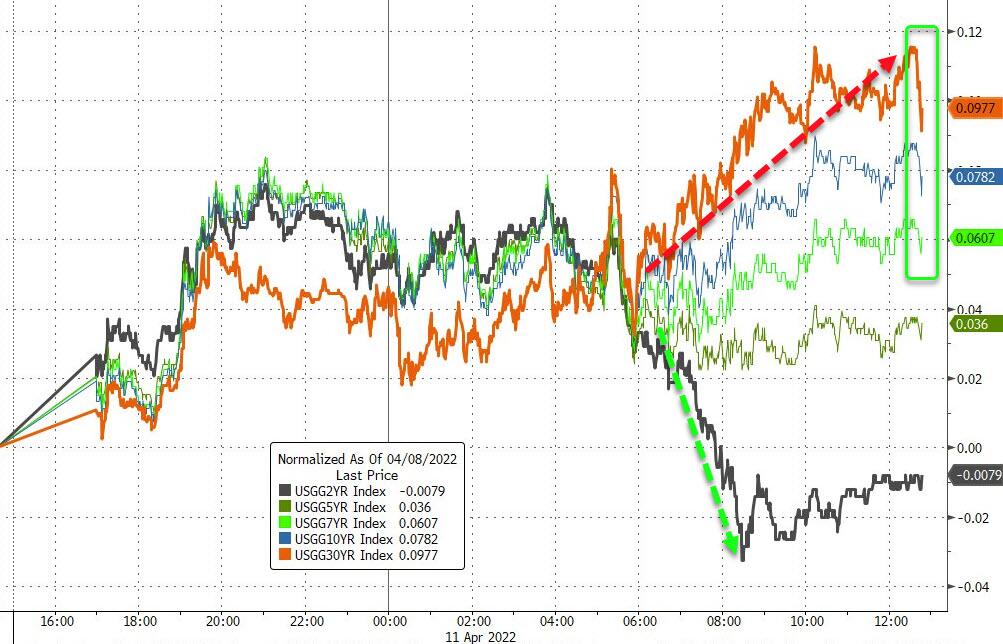

Treasuries very mixed today with the short-end outperforming and the long-end smacked with the ugly stick (30Y +11bps, 2Y -1bps). That was right before the last few minutes as stocks puked, a bid emerged for the long-end, rescuing its from its worst levels

{kind=link}

Source: Bloomberg

The yield curve steepened dramatically today with 2s10s surging up to the pre-March-FOMC plunge levels…

{kind=link}

Source: Bloomberg

Notably, a 7-part back-end loaded Amazon deal, large block trades, and a looming $20 billion 30-year bond reopening sale on Wednesday all contributed to the curve steepening today.

Additionally, the steepening appears to be driven by a sudden rush to short the 10Y (as signaled by the plunge in o/n repo rates)…

{kind=link}

Source: Curavture’s Scott Skyrm

And rather notably while the rate-hike cycle remains relative unchanged (around 9 more hikes this year), the subsequent rate-cut cycle is shifting hawkishly with just 2 cuts now priced in for the following 2 years…

{kind=link}

Source: Bloomberg

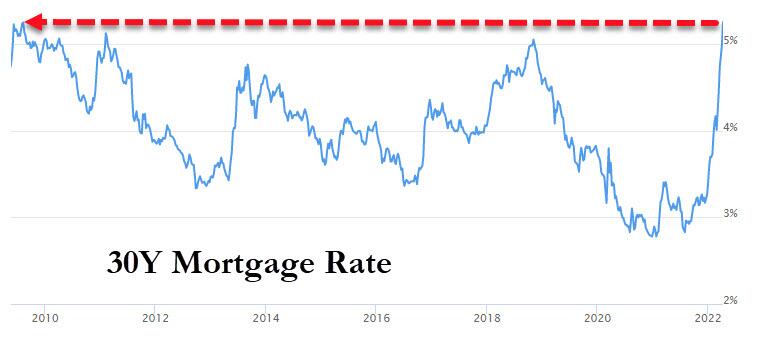

Meanwhile the 30Y mortgage rate hit 5.25% today – the highest since 2009!

{kind=link}

Bitcoin collapsed in the last 24 hours, puking back below $40,000 (not far above the pre-invasion levels of late Feb)

{kind=link}

Source: Bloomberg

The dollar extended its gains to its highest close since July 2020…

{kind=link}

Source: Bloomberg

Interestingly, after a weekend of downplaying Russia’s currency recovery, the Ruble was clubbed like a baby seal today…

{kind=link}

Source: Bloomberg

Oil prices tumbled back near pre-invasion lows today with WTI trading with a $92 handle briefly…

{kind=link}

Gold rebounded further today, back above $1970 intraday…

{kind=link}

Finally, this is all happening against a backdrop of severe economic malaise in America. Instead of relying on the traditional “Misery” Index (which relies on the ‘unemployment rate’, which in turn is entirely dependent on the participation rate), we go straight to the source and create an ‘alt-Misery’ Index (combining the inflation rate and the percent of Americans not participating in the workforce). It is currently at 40 year highs of ‘Misery’…

{kind=link}

Source: Bloomberg

This ‘alt-Misery’ Index dovetails strongly with The Fed’s own survey findings today that “Perceptions about households’ current financial situations compared to a year ago deteriorated in March, with more respondents reporting being financially worse off than they were a year ago. Respondents were also more pessimistic about their household’s financial situation in the year ahead, with fewer resondents expecting their financial situation to improve a year from now.”

And bear in mind tomorrow is CPI day… and The White House has already warned of “extraordinarily elevated” March inflation (no doubt entirely due to Putin, of course).

“Due to Putin’s Price Hike™️” 🙄 pic.twitter.com/yD9GY2p2ni

— Ramp Capital (@RampCapitalLLC) April 11, 2022

And there’s no need to worry, because as Chicago Fed president Charles Evans said today, “we will know a lot more about persistent inflation the end of the year” and (here’s the best line), he is “hopeful it’s receding…”

So The Fed is now in the business of “hope”!

Tyler Durden

Mon, 04/11/2022 – 16:01