42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

CPI Miss Sparks 3rd Biggest Short Squeeze Ever: Stocks, Bonds, Gold Soar As Dollar Crashes

A very, very, very, very slightly softer than expected Core CPI print combined with broadly less-hawkish FedSpeak sparked the biggest rally in stocks since April 2020 and the biggest collapse in TSY yields since March 2020.

The massive rally in stocks and bonds sent the 60/40 portfolio up 3.4% today. Since 1988, there have been only seven other sessions when the portfolio jumped more than 3%, all happening during the 2020 and 2008 recessions.

{kind=link}

Source: Bloomberg

Keep in mind, though, that the forward returns after these big rallies have been poor.

So CPI stoked the market’s rally then Dallas Fed’s Lorie Logan pured gasoline on that fire by signaling The Fed would soon slow its pace of tightening…

“This morning’s CPI data were a welcome relief, but there is still a long way to go,”

“While I believe it may soon be appropriate to slow the pace of rate increases so we can better assess how financial and economic conditions are evolving, I also believe a slower pace should not be taken to represent easier policy.”

Basically echoing the FOMC statement and trying to position herself a little towards Powell’s comments. Fed’s Harker and Daly also reiterated the same comments, specifically citing “the effect of cumulative tightening,” but noting that there is a need to tighten further and that 50bps is still a significant rate hike.

However, Fed’s Mester appeared to push back a little, arguing that “the risk of tightening too little outweighs the risk of tightening too much…”

And Fed’s Esther George warned that “monetary policy has more work to do,” but did bring up the risk of financial market instability.

So, all 5 Fed speakers confirmed higher rates from here, 3 signaled somewhat less hawkishly, 1 signaled a slight fear of overtightening, and 1 was full-hawktard.

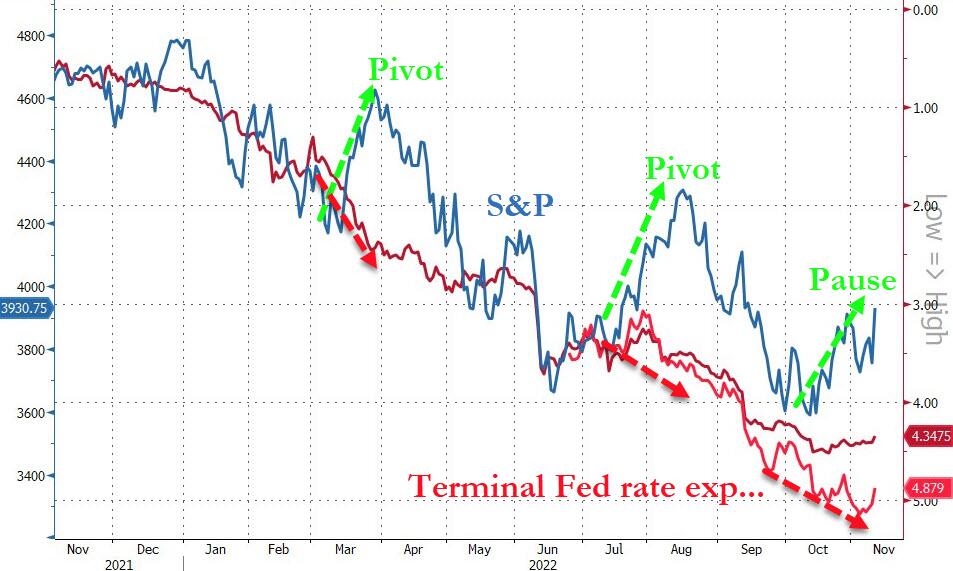

The result of all that was a dovish collapse in rate-trajectory expectations. Terminal Fed rate expectations tumbled back below 5.00% (meaning there are 100bps of hiking left in the cycle) – back below post-FOMC statement spike lows. At the same time, rate-cut expectations for after the peak in H2 2023 surged to almost 50bps (adding an tire 25bps rate-cut today). We note that realistically the only way The Fed is cutting that aggressively is if the US economy is in recession, and that is hardly a positive for stocks…

{kind=link}

Source: Bloomberg

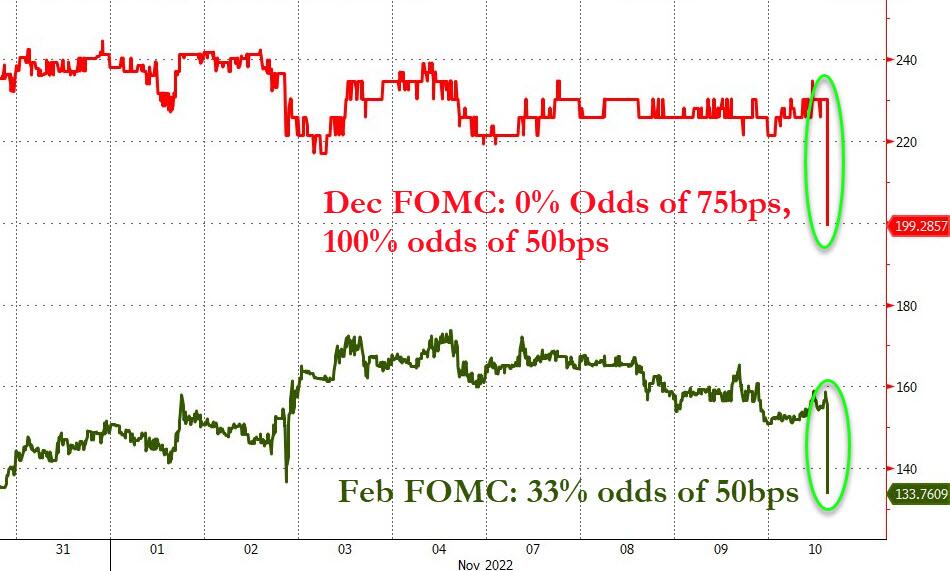

And a collapse in December’s rate-hike expectations (pricing out a 75bps hike completely and locking in 50bps)…

{kind=link}

Source: Bloomberg

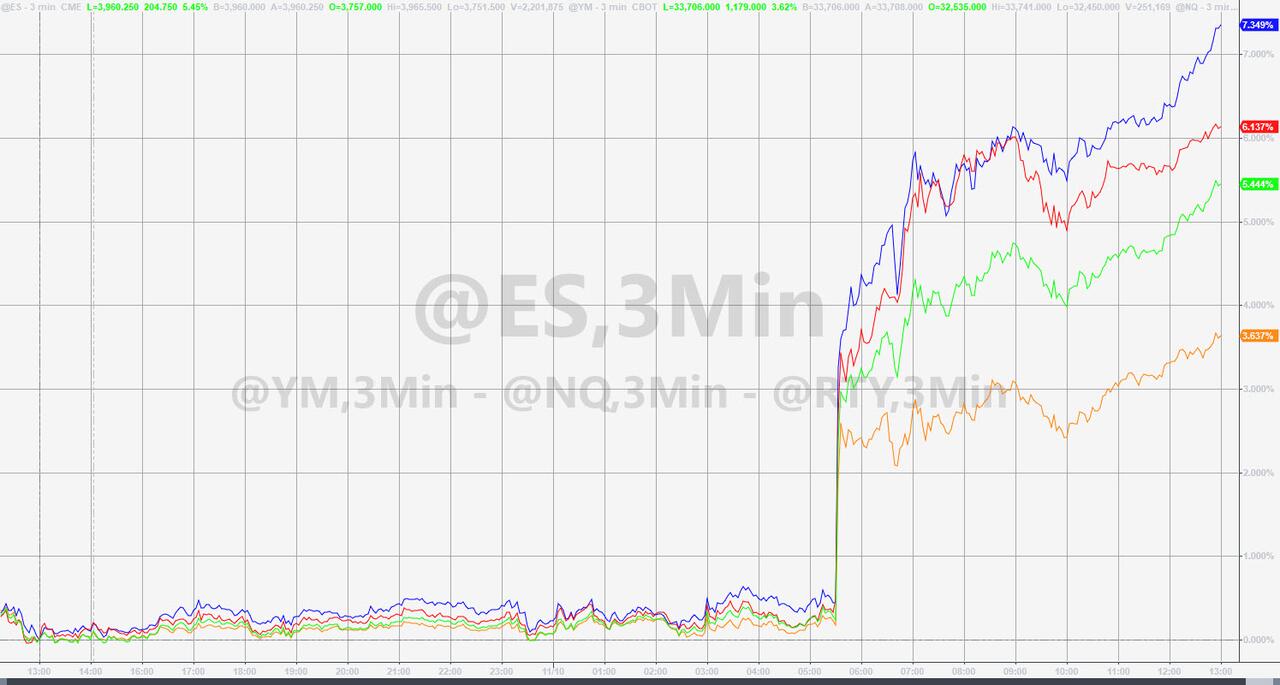

Stocks soared on all of this. around 1200ET, some additional FTX/SBF headlines on the size of the shortfall spooked cryptos and that weighed on stocks, but nothing was going to stop stonks today and they all surged to highs on the day. Nasdaq’s massive 7.3% rise today was the 3rd best day since Oct 2008 (Lehman crisis bear market bounce ahead of Fed meeting) – the other two were in March 2020. The Dow was ‘only’ up 3.6%, S&P up 5.4% and Small Caps surged over 6%…

{kind=link}

Meanwhile…

*NASDAQ 100 INDEX RALLY REACHES 7%; S&P 500 UP 5.2% https://t.co/BCpGVcMaOu

— zerohedge (@zerohedge) November 10, 2022

When the Nasdaq did this in 2008, it did not end well…

{kind=link}

The Nasdaq closed above its 50DMA for the first time since Sept 12th…

{kind=link}

This was the biggest daily short-squeeze (+10%) since April 2020’s Fed-fueled melt-up from the COVID lockdown crisis lows… This was actually the 3rd biggest short squeeze on record (since before the GFC)… We do suggest some caution since the squeeze stalled out at the close from last Friday’s Payrolls puke…

{kind=link}

Source: Bloomberg

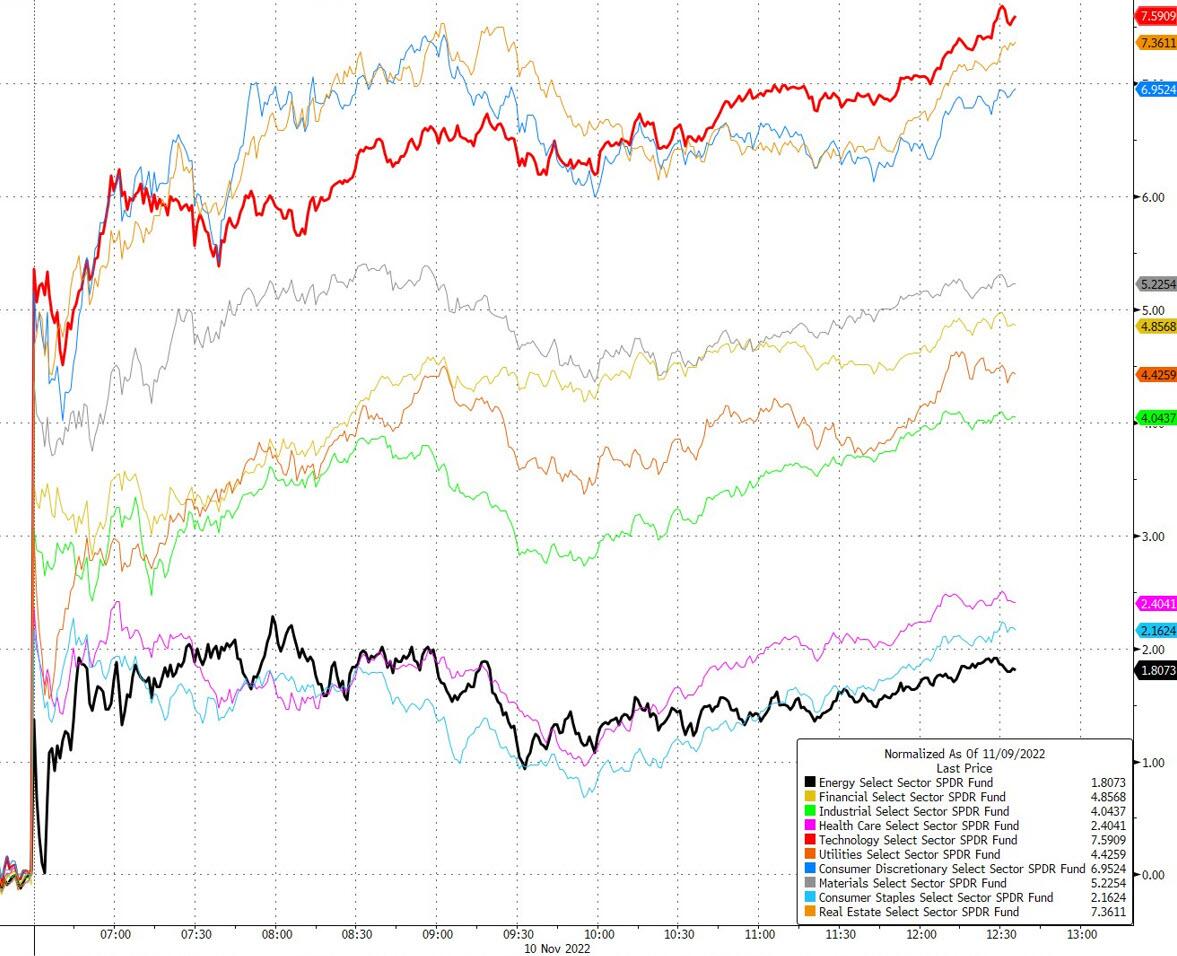

Tech outperformed (the lonbgest-duration stocks) while energy lagged but every sector was up large today…

{kind=link}

Source: Bloomberg

Also of note is that this massive short-cover occurred right as ‘most shorted’ stocks broke below the pre-COVID peak…

{kind=link}

Source: Bloomberg

Treasuries were just as insanely bid today. The short-end outperformed with 3Y yields collapsing 30bps, 30Y yields plunged ‘only’ 20bps…

{kind=link}

Source: Bloomberg

The 10Y yield crashed over 26bps, back below 4.00% to 5-wek lows – its second largest daily yield drop since March 2009…

{kind=link}

Source: Bloomberg

The 30bps collapse in 3Y yields is the largest since Nov 2008…

{kind=link}

Source: Bloomberg

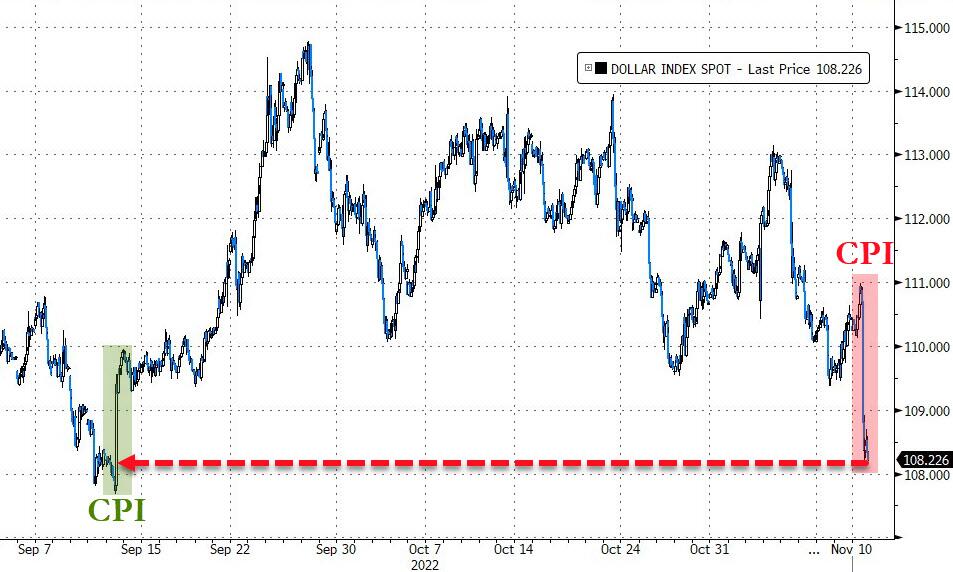

The DXY Dollar Index crashed over 2% today to 2-month lows – its biggest daily drop since Dec 2015 (ECB cut less than expected against Yellen hawkishness on strong jobs). The Dollar Index has now erased all of the gains since September’s hotter-than-expected CPI print…

{kind=link}

Source: Bloomberg

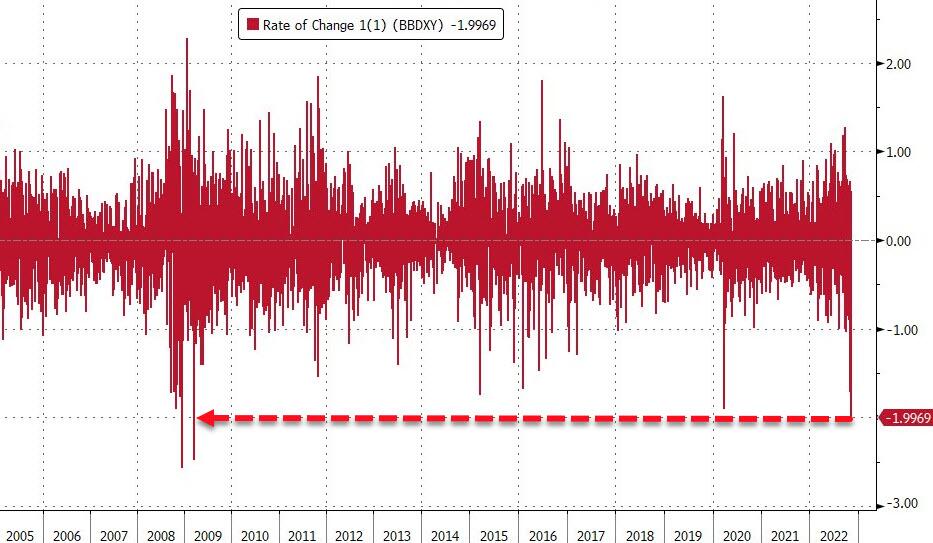

The Bloomberg Dollar Index (a broader measure than DXY) saw its biggest daily drop since March 2009…

{kind=link}

Source: Bloomberg

The Offshore Yuan exploded higher today, hitting a one-month high…

{kind=link}

Source: Bloomberg

Today also saw a massive surge stronger in the JPY back up at its strongest US session close against the dollar in over 2 months. USDJPY basically closed at the peak of its September BoJ intervention spike…

{kind=link}

Source: Bloomberg

Cryptos actually managed gains today, despite some more painful realities from FTX. Bitcoin bounced off a $15k handle overnight and rallied back up to $18k at its highs today…

{kind=link}

Source: Bloomberg

Gold’s recent spike accelerated up to almost $1760 – its highest since August…

{kind=link}

Oil rallied on the day, after 3 straight down days, with WTI chopping around between $85 and $87 (we note that the 50DMA is at $86)…

{kind=link}

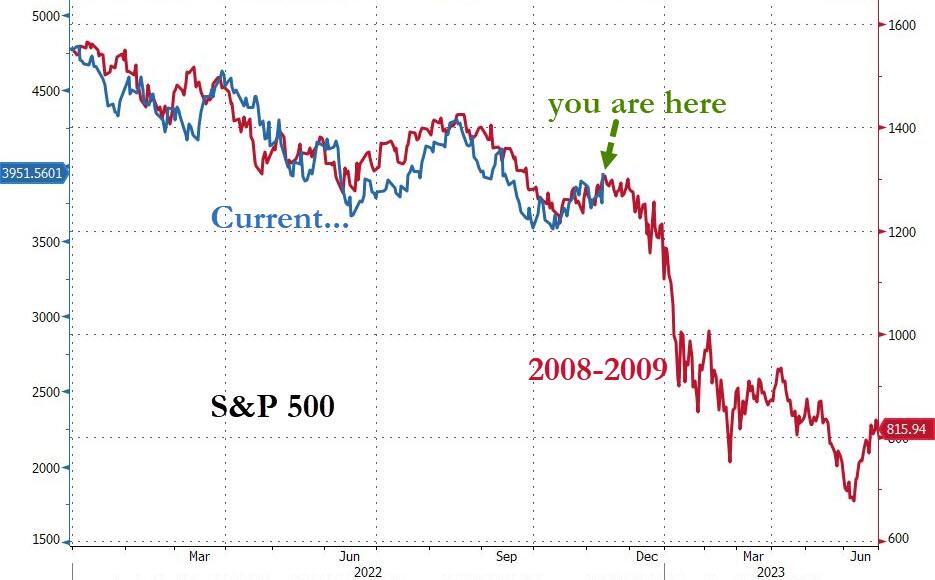

Finally, after today’s exuberance, some context. If you’re pricing in a ‘pause’/’slowdown’ by The Fed, you’re overdoing it in stocks…

{kind=link}

Source: Bloomberg

One more thing – we’ve seen this before…

{kind=link}

Source: Bloomberg

Don’t forget, bonds are closed tomorrow for Veterans Day, so there won’t be the same long-duration amplifier for stock gains as today.

Tyler Durden

Thu, 11/10/2022 – 16:01