42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Exxon Reports Record, Blowout Earnings; Stock Soars To All-Time High

The worse the tech wreck, the more the fuel – so to speak – for energy gains, and following what has been the worst quarter for megacap tech names, most of which have tumbled double digits following dismal earnings, it is hardly a surprise that the two largest US energy majors just had blowout quarters, with Exxon posting its strongest quarterly result in the company’s 152-year history including its highest ever net income, while #2 Chevron reported its second-largest profit; the two companies amassed more than $30 billion in combined net income as Democrats blast Big Oil for raking in massive profits but since a red avalanche is coming to Congress in less than two weeks, we doubt anyone cares what Democrats think.

We’ll leave the analysis of Chevron to someone else, like Warren Buffet for example, and focus instead on the one stock we have been recommending ever since the summer of 2020 when it traded below $40 and when the megabrains at S&P Global decided to kick it out of the Dow Jones (it is up 170% since then).

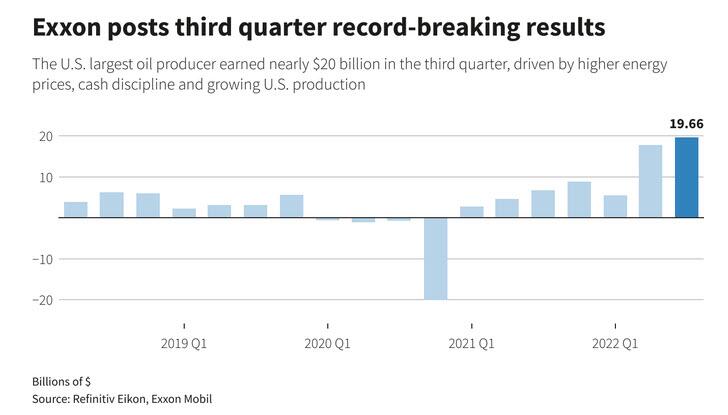

Exxon Mobil, the company that now represents all that is wrong with the admin’s ESG policies and the world’s Green agenda, smashed expectations as soaring energy prices fuelled a record-breaking quarterly profit, nearly matching that of tech giant Apple.

Its $19.66 billion third-quarter net profit far exceeded recently raised Wall Street forecasts as sky-rocketing natural gas and high oil prices put its earnings within reach of Apple’s $20.7 billion net for the same period. As recently as 2013, Exxon ranked as the largest publicly traded U.S. company by market value – a position now held by Apple. XOM’s market cap is $450BN today while AAPL is $2.3 trillion, so XOM would need to rise just 5x from here – a stock price of $550 – to catch up to AAPL.

{kind=link}

The top US oil producer also reported per share profit of $4.68, exceeding Wall Street’s $3.89 consensus view, on a huge jump in natural gas earnings, continued high oil prices and strong fuel sales.

“Our investments over the past five years, including through the lows of the pandemic, are really driving our results today,” Chief Financial Officer Kathryn Mikells told Reuters.

Some more details from the company’s blowout, record quarter:

Total revenues & other income $112.07 billion, +52% y/y, blowing away estimates of $103.14 billion

EPS $4.68 vs. $1.58 y/y, blowing away estimates of $3.89

Upstream adjusted net income $11.84 billion, estimate $11.69 billion

Energy products adjusted net income $5.54 billion, estimate $3.39 billion

Chemical products adjusted net income $812 million, estimate $791.9 million

Specialty products adjusted net income $762 million, estimate $750.5 million

Chemical prime product sales 4,680 kt, -2.8% y/y

Production 3,716 KOEBD, +1.4% y/y

Crude oil, NGL, bitumen and synthetic oil production 2,389 KBD, +3.3% y/y

Natural gas production 7,963 MCFD, -1.8% y/y

Refinery throughput 4,165 KBD, +2.8% y/y

Exxon, which led record gains by the five producers known as oil majors in the prior quarter, pulled far ahead of peers Shell and TotalEnergies with third-quarter profits almost twice as big. Its gains were aided by its highly criticized decision to double down on fossil fuels as European competitors shifted to renewables. The company has banked a record $43 billion in the first nine months of this year, 19% more than in the same period of 2008, when oil prices traded at a record level of $140 per barrel.

{kind=link}

Some more highlights from the quarter:

Achieved best-ever quarterly refining throughput in North America and highest globally since 2008

Strong quarterly oil and gas production; ~50 Koebd increase

Record in the Permian Basin

Guyana grew to ~360 Kbd

First LNG production was achieved from Mozambique’s Coral South FLNG development in October

Asset sales delivered $2.7 billion in cash proceeds in the quarter, bringing the yearto2 date proceeds to ~$4 billion

Still sees capital expenditure $21 billion to $24 billion, estimate $17.77 billion

The company spent $5.73 billion on new oil and gas projects last quarter, up 24% from a year ago, and remains on track to hit an investment target of $21 billion to $24 billion this year.

Rising profits have renewed calls by U.S. President Joe Biden for companies to invest the windfall profits from this year’s energy price runup in production rather than buy back their own shares.

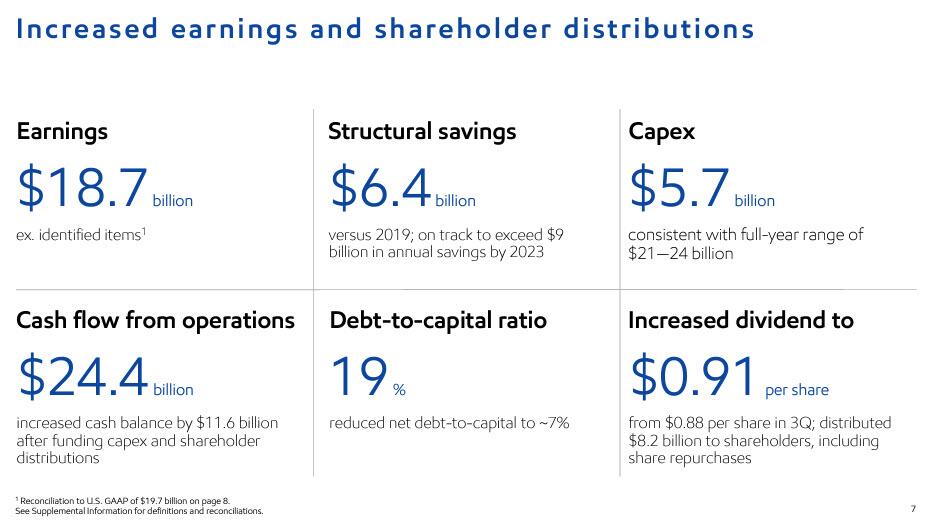

Exxon also said it will maintain its $30 billion share buyback program through 2023 while increasing dividends. On Friday, it declared a fourth-quarter per share dividend of 91 cents, up 3 cents, and will pay $15 billion to shareholders this year.

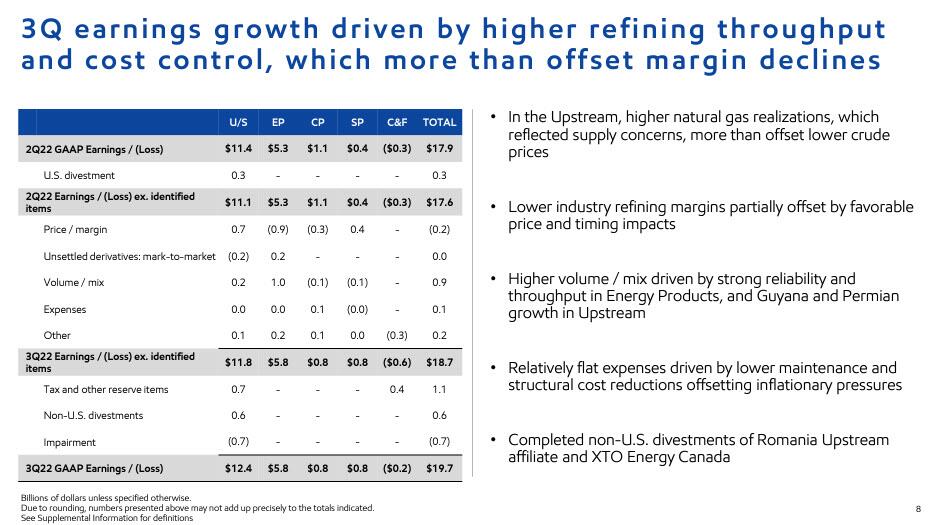

Unlike the megacap tech giants which are spending like drunken sailors hoping the Fed will the zero-cost funding flowing forever, and their stocks are collapsing as a result, Exxon said that Q3 earnings growth was driven not only by higher refining throughput but also “cost control, which more than offset margin declines.” Yes, it can be done, if only management is competent and qualfied!

{kind=link}

Some more commentary and context from the quarter:

Declared 4Q Div of $0.91/Shr, up 3c from $0.88; Paying Out $15B in Div Aggregate for Year

On Track With Year Guidance of $21B to $24B for Capex

On Track to Exceed $9B in Annual Savings by 2023

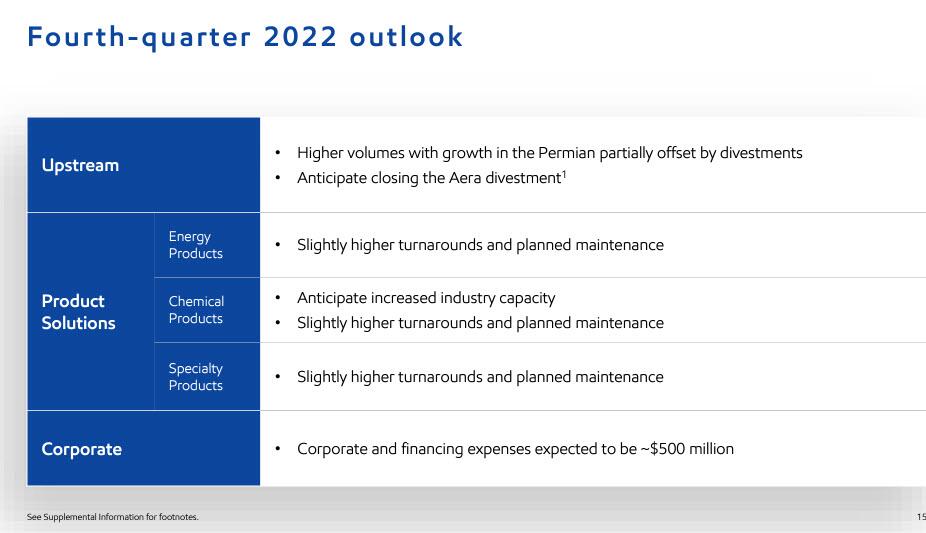

Sees 4Q Corporate, Financing Expenses to Be ~$500M

4Q Upstream, Sees Higher Volumes With Growth in Permian

Qtr incl favorable identified items of nearly $1 billion associated with completion of XTO Energy Canada and Romania Upstream affiliate divestments and one-time benefits from tax and other reserve adjustments, partly offset by impairments

Upstream Gas realizations increased 22% on European supply concerns and efforts to build inventory ahead of winter, more than offsetting the impact of decreasing crude realizations, which were down 12% on modest supply increases

“Rigorous cost control and growth of higher-margin petroleum and chemical products also contributed to earnings and cash flow growth in the quarter.”

Exxon said its oil and gas production from the Permian Basin is near 560,000 barrels of oil equivalent per day (boed), a record. That is up 11% or 50,000 barrels per day from a year ago. Results were helped by an almost 100,000 boed increase over the previous quarter in Guyana, where Exxon leads a consortium responsible for all output in the South American nation.

But output was hit by its withdrawal from Russia, where it abandoned more than $4 billion in assets and a 220,000 boed project following Moscow’s invasion of Ukraine. Exxon said its assets were expropriated. As a result, the company reduced its production forecast for the year by about 100,000 barrels per day.

“We are going to end up at about 3.7 million barrels a day for the full year,” Mikells said, down from a 3.8 million goal set in February.

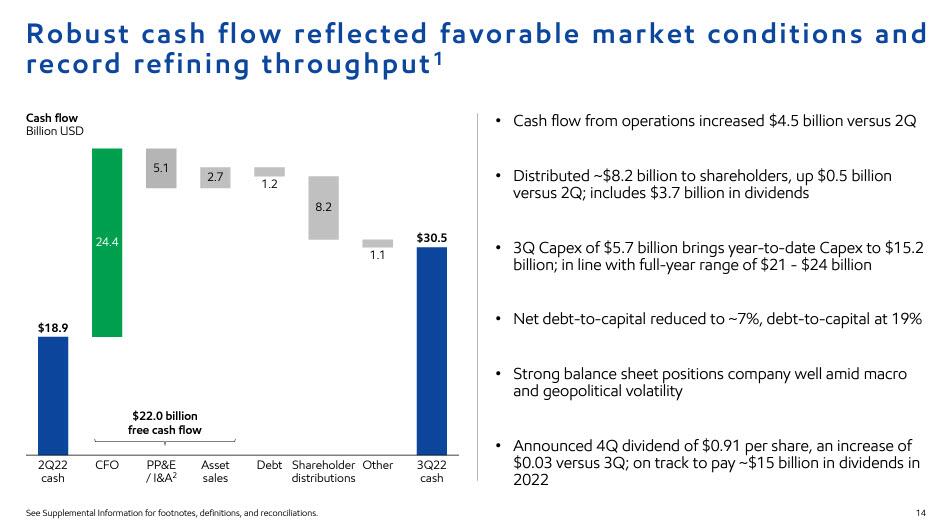

Despite that, Exxon’s cash flow bridge was a chart of beauty: the company generated $22BN in cash flow in Q3, and after paying down $1.2BN in debt and $8.2BN in shareholder distributions as well as $1.1BN in other spending, it was left with a whopping $30.5BN in cash on hand, a far cry from the near-insolvency the company found itself in in the aftermath of the Covid crash.

{kind=link}

Not surprisingly, the company’s outlook was solid, expecting strong Permian volume and growth, while warning of “slightly higher turnarounds and planned maintenance” across energy, chemical and specialty products.

{kind=link}

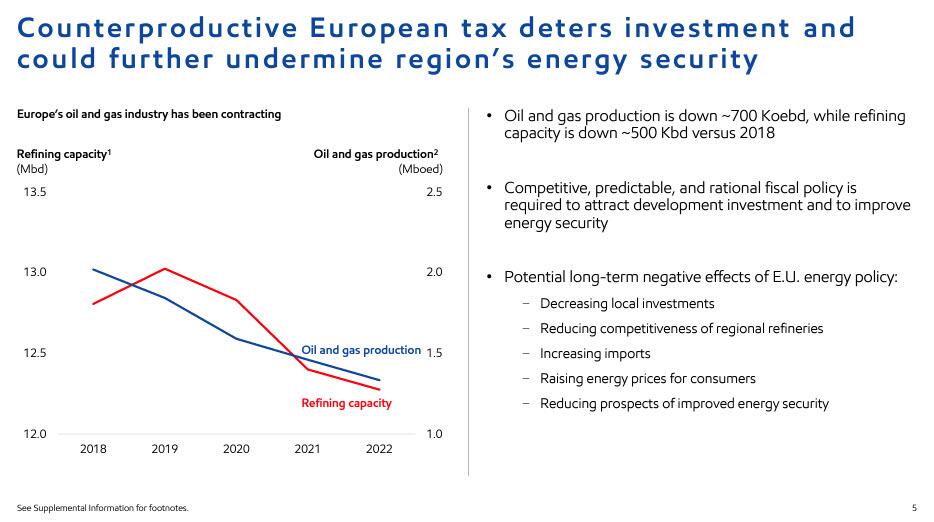

Besides stellar earnings, the company did not walk back from challenging the increasingly hostile political environment. Exxon was quick to point out that Europe’s energy crisis is largely the result of its own doing.

{kind=link}

Exxon also responded directly to Biden’s criticism of record energy-industry profits by pointing to the company’s much-vaunted dividend, which it increased on Friday by a larger-than-expected amount.

“There has been discussion in the U.S. about our industry returning some of our profits directly to the American people,” Exxon Chief Executive Officer Darren Woods said in prepared remarks ahead of the company’s earnings conference call. “That’s exactly what we’re doing in the form of our quarterly dividend.”

As pointed out above, Exxon raised its quarterly dividend to 91 cents per share from 88 cents, 1 cent more than forecast. Exxon’s dividend payments over the last 12 months have overtaken Apple Inc.’s to become the second-largest in the S&P 500 Index, behind Microsoft Corp, according to data compiled by Bloomberg.

Alas, there were no additional shareholder returns announced for Chevron, unlike Shell, Repsol and Equinor; however, just months ago, the company raised dividends and share buybacks to a combined $25 billion a year.

Of course, rewarding energy shareholders – who were crushed during the covid crisis with XOM stocks plunging almost 80% from all time highs – has done nothing to appease the senile resident of the White House basement, however, and in fact has fueled his resentment against Big Oil. On Thursday, he once again attacked oil companies after Shell issued bumper earnings, criticizing the UK company for increasing its dividend rather than cutting prices at the pump.

The good news for XOM investors is that after Nov 8, anything the raging Democrats have to say or propose in their crusade to nationalize every profitable asset in the economy, is irrelevant.

The other good news for XOM investors: in response to these stellar, blowout earnings, XOM stock just hit a new all time high this morning, rising as high as $111.1 pre-market. And despite Jim Cramer turning bullish on energy names, we are hopeful that there is much more upside in the name.

{kind=link}

The sellside was, naturally, full of praise:

Piper Sandler (Overweight): Exxon “showed off its leading leverage to global refining with a significant beat on 3Q results,” analyst Ryan Todd writes

Results demonstrated “impressive leverage to robust gas markets that more than offset the weaker crude prices”

Truist Securities (Hold; PT $111): Better natural gas prices, higher oil volumes lifted results but were “offset by higher spending”

Analyst Neal Dingmann notes Exxon is pursuing multiple projects including in Guyana and the Beaumont refinery expansion, but says “prioritizing Permian growth in the near-term to fund the longer cycle projects would result in higher investor interest”

Jefferies (Buy; PT $133): Analyst Lloyd Byrne looks for detail on an activity ramp up and “inflation in the Permian”

Notes upstream adj. net income of $11.8 billion was 12% lower than the bank’s estimate of $13.5 billion, though 9% higher than consensus

International upstream production was “the primary driver of the consensus beat” as a result of higher European natural gas prices

The company’s full earnings presentation is below.

Tyler Durden

Fri, 10/28/2022 – 09:34