42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

The Big Stock Capitulation Is Yet To Come

Authored by Simon White, Bloomberg macro strategist,

The real decline in stocks has yet to come, as inflation and recession threaten the historic overweight in equities versus bonds.

It has been a torrid year for financial assets. The paradigm shift in inflation has led to decades of market experience being turned on its head, with stocks and bonds commonly falling together. This year has seen a peak-to-trough drawdown of over 25% in the S&P, and an historic 15% drop in Treasuries.

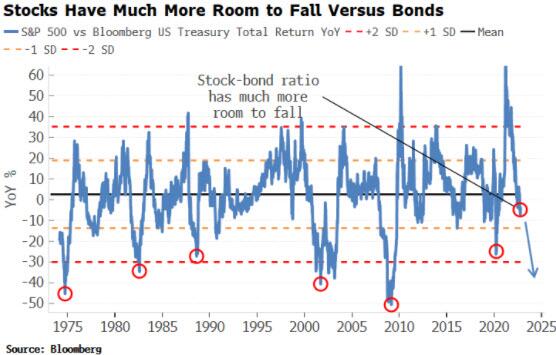

The stock-bond ratio has declined precipitously, but we are likely just getting started.

The ratio tends to revert to its mean, but with big overshoots.

Those to the upside typically lead to overshoots to the downside of a similar magnitude. The enormous fiscal and monetary injections during the pandemic led to a dizzying bubble in financial assets, sending the stock-bond ratio skyward.

{kind=link}

But the fall in stocks and bonds this year has only taken the ratio to just below its mean.

We are in the process of an overshoot that could take it much lower still, driven by the twin specters of inflation and recession.

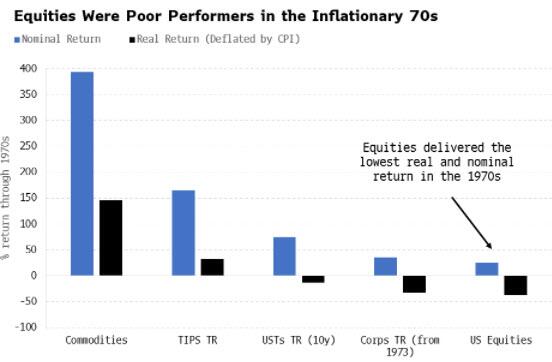

It’s a common misconception that equities are an inflation hedge. Some stocks and sectors, particularly those related to real assets, do make good inflation hedges, but equities overall are terrible at protecting against persistent price rises.

In fact, equities were the worst-performing main asset class in both real and nominal terms during the Great Inflation of the 1970s. This is because they became a shunned asset.

Why?

Stocks have an infinite duration with a fixed coupon, the return on equity. Bonds, on the other hand, have a maturity date where there is an opportunity to renegotiate the coupon.

{kind=link}

When inflation is high, equities have to compete with bonds and they begin to look less and less attractive. Today, the real dividend yield of the S&P is -5.6% and the real earnings yield is -7.2%, while the real 10-year yield on a Treasury bond is -3.5%. Why bother with equities when you can get a comparatively juicy, less risky return from bonds?

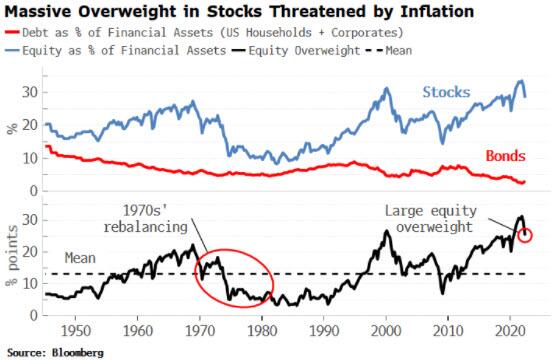

The big overweight in stocks versus bonds is therefore at great risk. The prospect of higher returns has meant a strong preference for stocks over bonds is the norm in the US. That overweight currently sits at its highest level since the tech bubble of 2000, after hitting even greater extremes during the pandemic.

As it becomes apparent inflation is entrenched and not returning to a low-and-stable regime any time soon, the penny will drop that equities are more of a leaky ship than a water-tight revenue generator, prompting an exodus to comparatively inflation-resilient bonds.

This exodus could be sizable, taking the stock-bond ratio considerably lower and decimating the long-term real return of equities. The 1970s saw a similar rebalancing, with the equity overweight in the late 1960s morphing into a record underweight that persisted until the late 1980s. Inflation, like a skin disease, gave equities a rash that made them unattractive for many years. They face the same risk today.

{kind=link}

A recession only makes the risk of further stock underperformance more immediate. Leading indicators point to a US recession in the next 3-6 months as being all but inevitable. Stocks face more downside in a downturn, while bonds are likely to catch their usual haven bid. History shows that the stock-bond ratio falls at a median of over 12% in the six months after a recession begins. Leaving aside that in real terms both assets are still likely to lose you money, the stock-bond ratio is poised to fall further in any economic slump.

Ultimately, though, stocks are more at risk than bonds as governments do not borrow in equity markets.

High inflation means yields could rise much higher, and at this point equities would be sacrificed to limit how much governments have to pay to borrow by way of financial repression. This, later on, may mark the final capitulation in the stock-bond ratio.

The long-term outlook for bonds is less than rosy in the current inflation paradigm, but the prospect for stocks is dimmer still.

Tyler Durden

Thu, 10/27/2022 – 13:00