42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Weak Semis Signal Recession… And Lower Yields Are On The Way

Authored by Simon White, Bloomberg macro strategist,

The very poor performance of the semiconductors sector this year confirms that the US will soon face a recession. This leaves extremely oversold US Treasuries increasingly vulnerable to a short-covering and haven-driven rally.

The semiconductors sector has performed the most poorly this year, down more than 40%, versus the S&P which is down 22%. As a highly cyclical sector, semis are a very sensitive bellwether for the health of the US and the global economy.

The deep underperformance of semis this year points to significantly weaker ISM New Orders, itself a dependable leading indicator of growth conditions. New Orders is already under the 50 level that is the demarcation between contraction and expansion, and is projected to head yet lower.

{kind=link}

While ISM New Orders going under 50 is not a foolproof indication of a recession, when it is combined with other indicators pointing in the same direction, the case for one becomes virtually iron-clad.

Recessions are pervasive, pronounced and persistent economic slumps. The pervasiveness can be seen in the Philadelphia Fed State Diffusion Index, which is at a level that has preceded every recession since 1980 bar the pandemic.

The mortgage-rate driven slump in the housing market – a leading indicator for the economy as a whole – is very pronounced, with sales falling and house prices dropping too. Building permits have also been badly hit. With rates set to remain elevated for some time, this slowdown will be persistent, and it won’t be long before it ticks all the NBER’s recession criteria.

Semis’ weak showing also points to strong global headwinds.

South Korean exports are one of the best leading indicators of global trade and hence growth, given it is a small, open and trade-focused economy. At the current rate, the collapse in semis’ stock prices soon points to a relatively deep contraction in South Korean exports. The risk of global recession is also rising.

{kind=link}

Semis’ troubles have been aggravated by the US’s export ban on semiconductor materials earlier this month. Since then, US semiconductors have underperformed all other US sectors, implying the signal on US and global growth sent by semis is intensifying.

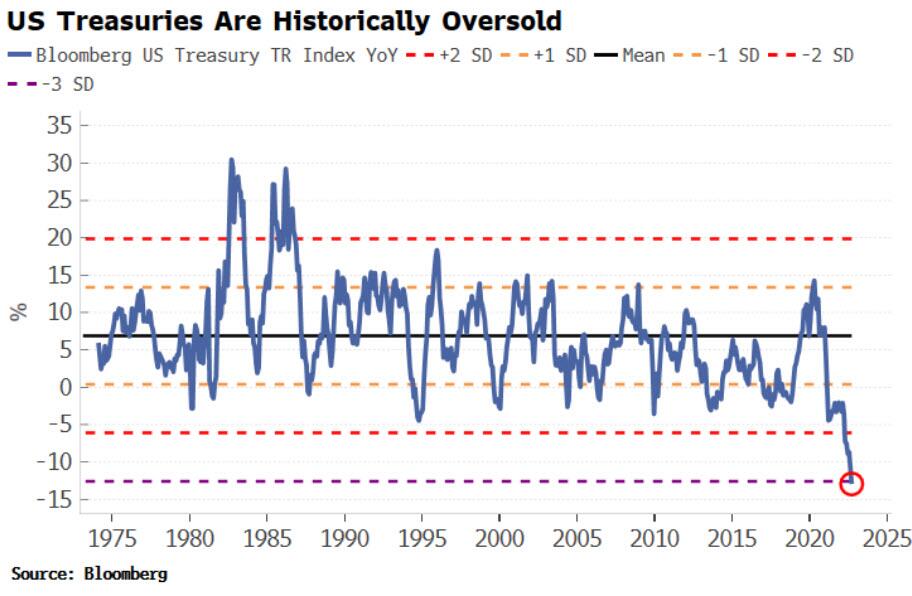

The high likelihood of a US recession makes US Treasuries look increasingly mis-priced.

Peak Fed hawkishness is likely here or very close. USTs are extremely oversold, and speculators are very short, while seasonals out to the end of the year are very positive.

{kind=link}

A recession would spur a potentially significant haven-driven bond rally, taking especially longer-dated US yields much lower.

Tyler Durden

Thu, 10/20/2022 – 12:25