42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

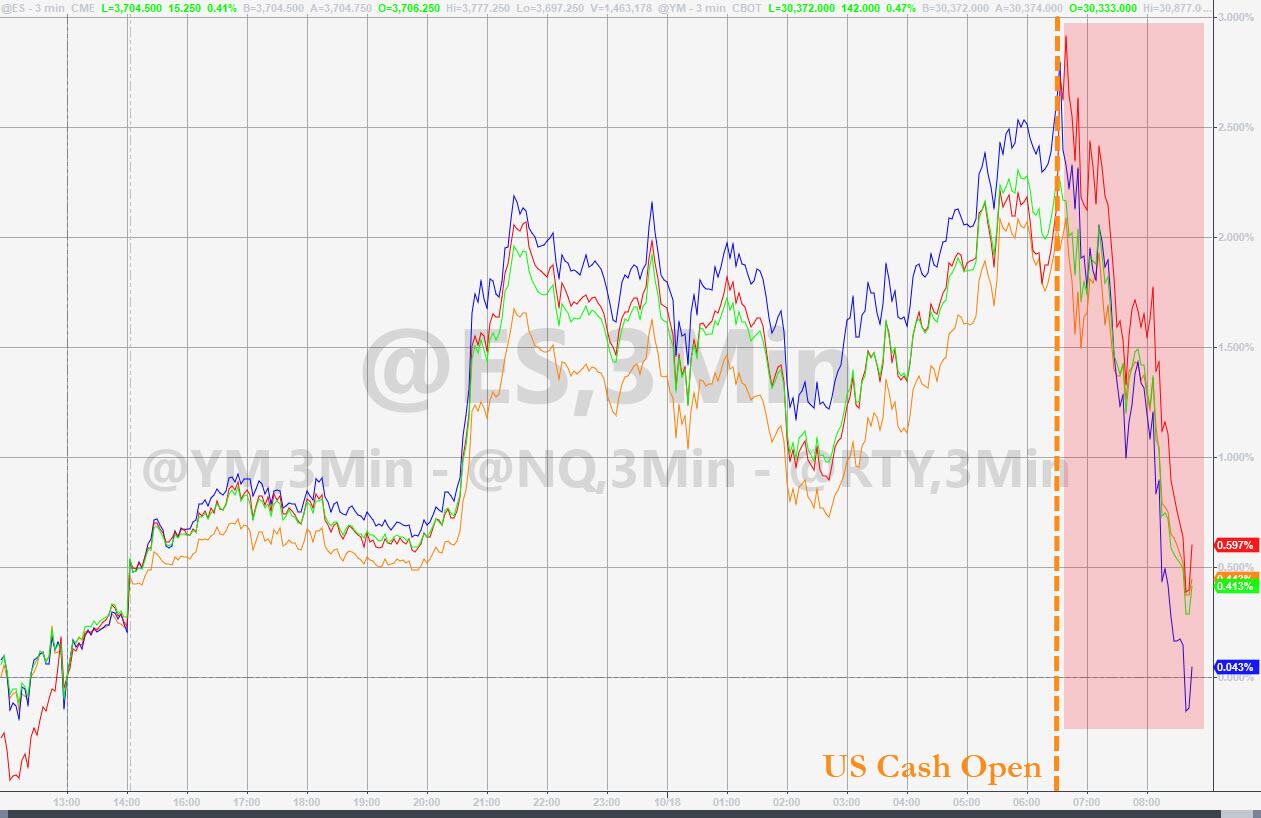

US Bonds, Stocks Are Suddenly Puking Into EU Close; “Correlation=1” Days Accelerating

With just minutes until the European close, US equity and bond markets are puking back earlier gains with Nasdaq is in the red now on the day (after being up almost 3% in the pre-open)…

{kind=link}

The selling started the moment the cash market opened – after another big short-squeeze…

{kind=link}

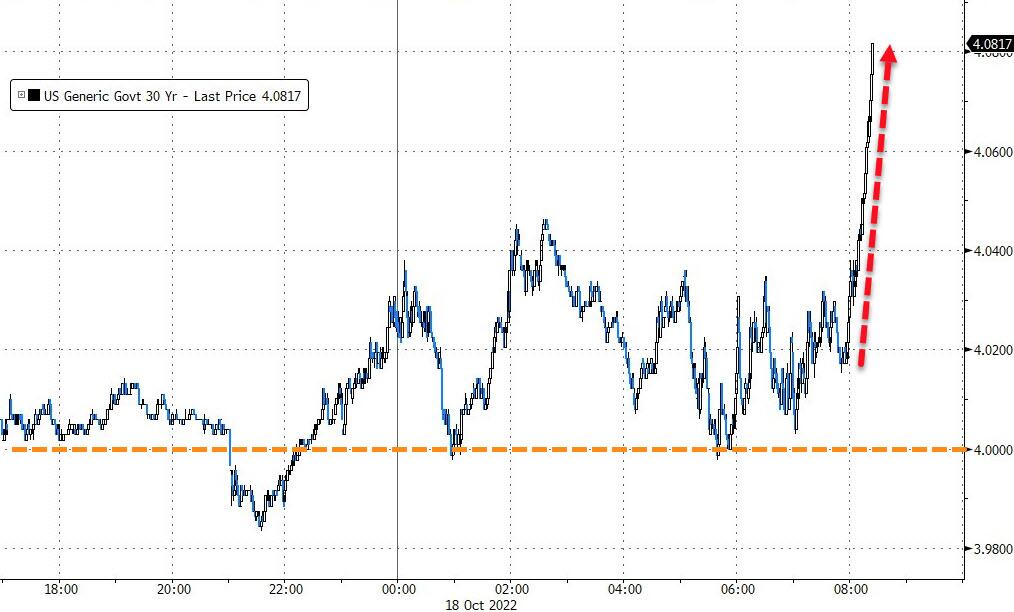

US Treasuries are also getting smashed with yields exploding higher…

{kind=link}

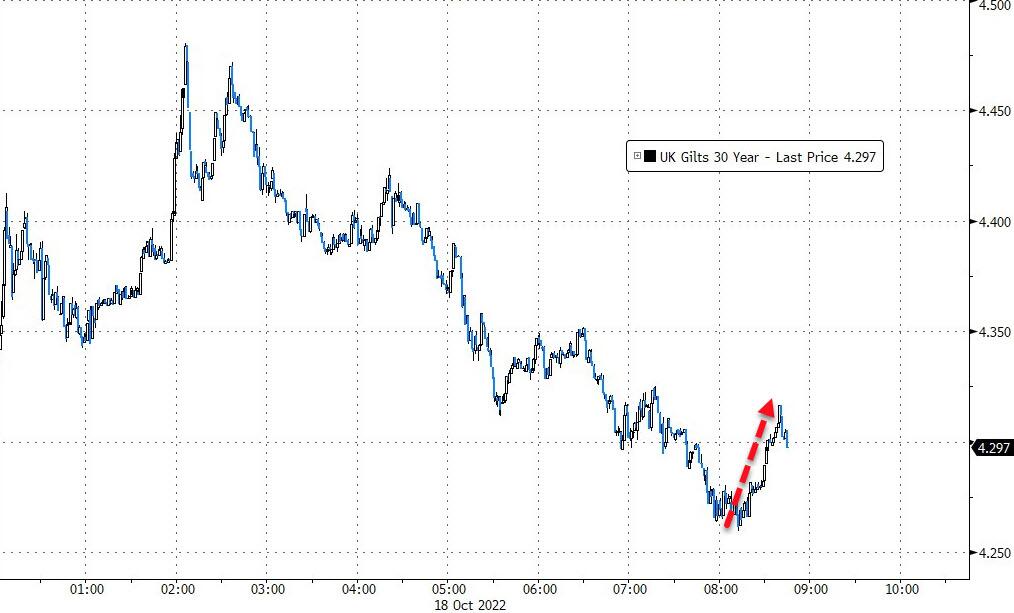

This started around 1100ET with no obvious headline catalyst, but some suggested comments out of Europe on property funds forced-selling may have prompted this sudden shift (after the narrative suggested the UK fund crisis was over)…

Bloomberg reports real estate funds whose investors include UK pension schemes have begun offering properties for sale to meet redemption requests.

The sales are the latest sign that the turmoil that has rocked the UK pension industry in recent weeks is still reverberating through financial markets. Pensions have been dumping stocks, bonds, collateralized-loan obligations, and pulling money from almost any fund that will give it back.

30Y Gilt yields suddenly turned up into their close…

{kind=link}

Fed rate-hike expectations continue to grind higher and more hawkish…

{kind=link}

Goldman’s Prime Desk noted that – the early action today was following the same pattern as yesterday – 240k SPX call options have traded (8k contracts per minute // 3billion notional per minute) and 620k SPY call options have traded (21k contracts per minute // 750million notional per minute).

Additionally, ETFs made up ~39% of the consolidated tape, continuing to indicate a macro product cover bid (with high vol leading to high usage of macro product)…

{kind=link}

And also of note is that Goldman’s CTA work suggests that there has been almost zero demand from this cohort over the last few sessions.

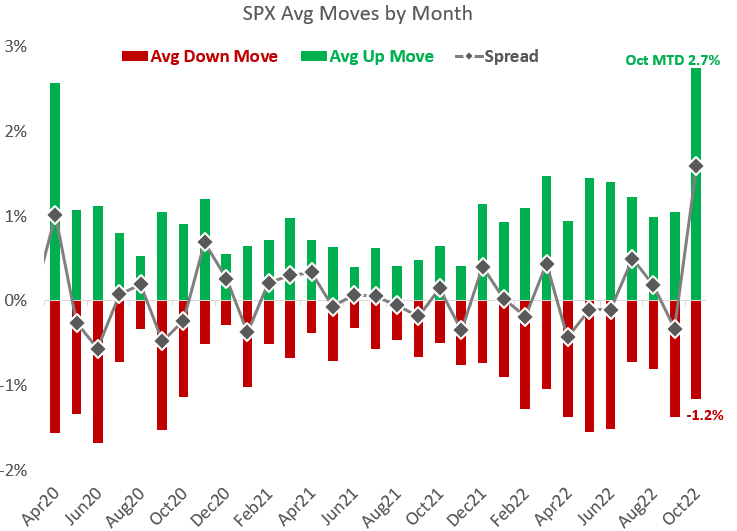

Finally, after the last few days, Nomura’s Charlie McElligott provided some context at just how extreme the far more explosive upside days have become to the ongoing “grind” to the downside.

The absolute magnitude of market moves on “Up” days in Oct-to-date is 2:1 that of “Down” days…

{kind=link}

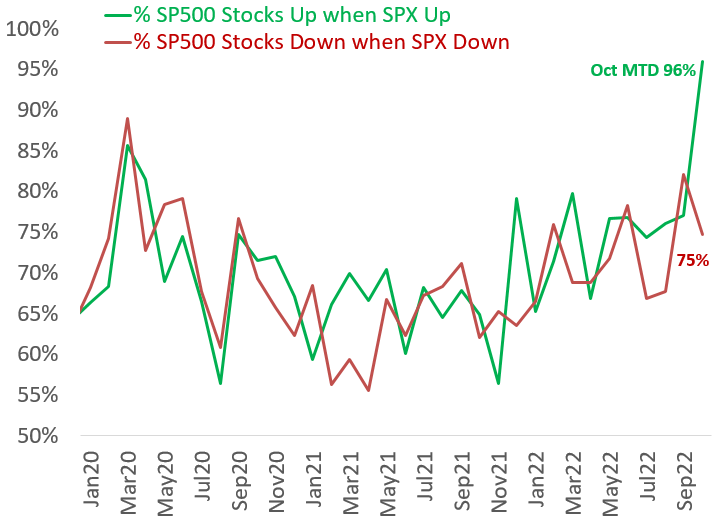

Additionally, McElligott notes that ‘against historical norms, “Correlation = 1” Days are now occurring on upside moves more than during down-days…

{kind=link}

Put it all together and it feels increasingly “unstable” – but hey, welcome to 2022!

{kind=link}

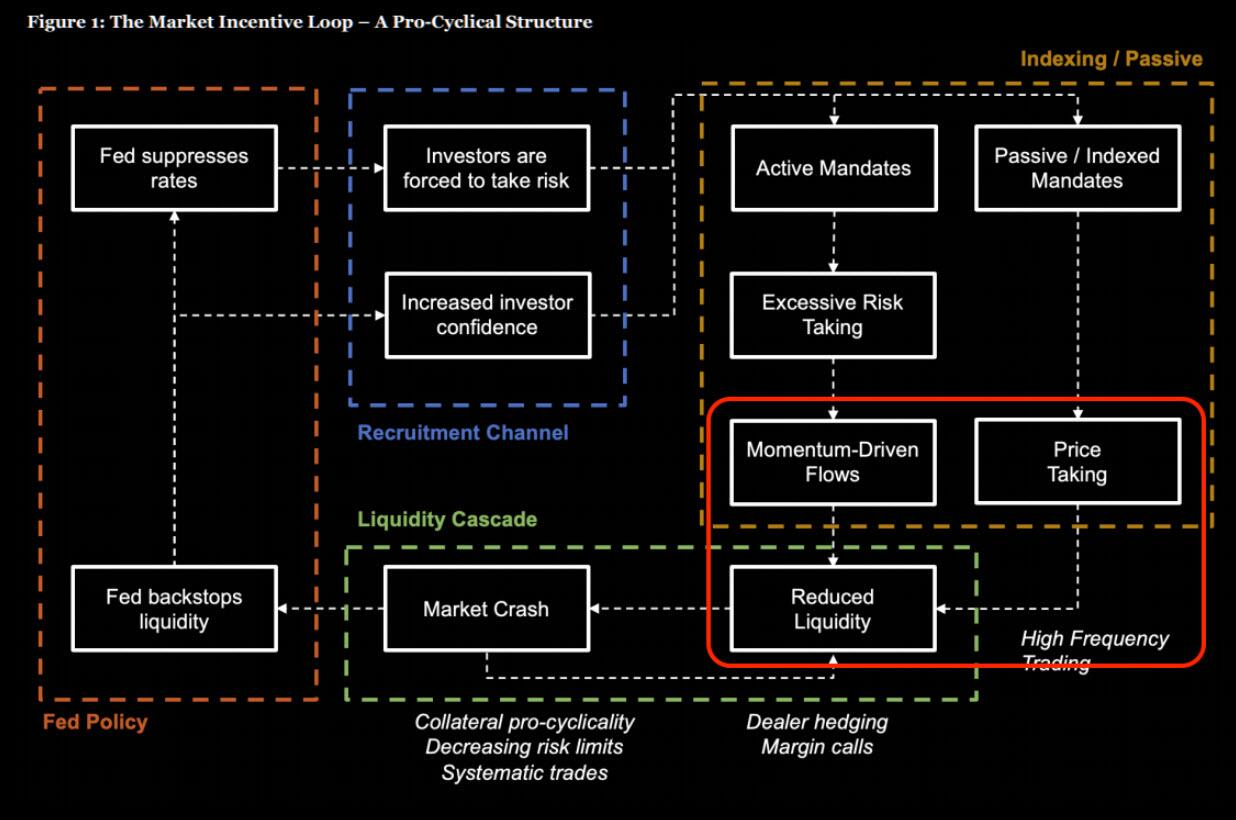

A few years ago Newfound Research put out an interesting piece called “Liquidity Cascades”. Below is a diagram from that note which outlines the feedback loop in markets from Fed policy to market activity.

{kind=link}

SpotGamma highlights the bottom right quadrant in red, which is what we mark as our current position. If you believe that options trading invokes dealer – that hedging is both momentum driven flow and price taking. Additionally, market makers cannot wait on a stock bid getting hit if their risk is too high – they will pay spread and take price. This is what makes that short dated volume from above such an issue in these markets which have lower levels of liquidity. It can amplify volatility in the ways we saw Thursday, Friday, and Monday, and have investors trying to draw fundamental conclusions from positional options hedging flows.

Perhaps today’s plunge is more of the same amplification flow.

As we have stated endlessly this year, markets rallying from put sales are inherently unstable, and we need to see call positions come in to quell volatility… for now we are not seeing that.

Tyler Durden

Tue, 10/18/2022 – 11:27