42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

“If You’re Reading This, It’s Too Late”: Nomura Sees ‘Puts Puked, Calls YOLO’d’

In case you were wondering WTF is going on this week while you hide under your desk from the barrage of global headlines and extreme swings in markets, Nomura’s Charlie McElligott has the ultimate overview (from a trader’s perspective) on yesterday’s action, today’s headlines, and what happens next…

{kind=link}

First, The UK…

On a day where the escalating systemic threat of a global markets “left-tail” event then forced a eventual “RIGHT-tail” outcome with regards to eventually dictating an embarrassing, but absolutely required, policy “U-turn” from the Truss government with regard to the disastrous unfunded tax cut plan (and what has now escalated to the outright “SACKING” of Kwasi Kwarteng as Chancellor, falling on the proverbial sword for the administration, with PM Truss still in the cross-hairs as well), it was a huge deal from a “removal of worst-case scenario” market relief perspective, particularly with regard to potential to breaking the recent “doom loop” zeitgiest of forced asset-selling in order to meet margin calls

As laid-out exactly in my last email, this laughably predictable “bending the knee” of the new UK govt to market forces which had already “voted with their feet” in true bond-vigilante fashion wasn’t just about culling the “left tail” scenario on account of the second-order liquidity management “flow impacts” of 1) forced deleveraging and 2) impulse redemption requests which were adding to global market strains on the lows of an already chaotic macro backdrop of shock tightening then attempting to be offset by burgeoning fiscal stimulus attempts from governments and market interventions from authorities…

Because the impact of what is now today’s “official” policy U-turn and outright “sacking” of the Chancellor then kicked-off de facto “RIGHT tail” trade, as the “pressure release valves” being UK Rates and FX which were the epicenter of this latest global markets shock over the past few weeks, were instead powerfully reversed (10Y Gilt Yields now -63bps from Wed highs, 30Y Gilt Yields -73bps from Wed highs and GBPUSD +280 pips from Weds lows and an impossible +850 pips above the “flash crash” lows following the UK budget plan announcement Sep 26th), both by removing the catalyst behind the “forced selling” pressures of the Pension liquidity clean-up, but also too dictating stop-outs / unwinds of “Shorts” who’d been exploiting the incoherent policy dysfunction.

{kind=link}

So as this UK episode sat at the core of the latest escalation of “macro Vol” in Rates and FX, the reversal impact it had on GLOBAL Markets was tangible, as we got that sudden “IMPULSE EASING” in financial conditions, with Bonds and Equities rallying in unison at the same time that the US Dollar was being smashed— i.e. the dead opposite of the year-to-date “macro trend trades” built around behind-the-curve Central Banks creating an impulsive “FCI Tightening” which has been ripping through asset prices via violent USD strength and higher Real Yields

CRITICALLY, taking a step-back from the UK issues and looking back to the US…

McElligott refers back to Wednesday’s email, where I documented the prolific “Short” / “Under-Positioning” in broad Equities exposure across Fund types (Long-Short HF Beta to SPX at 5.4%ile since 2003, Macro Fund Beta to SPX at 6.7%ile, CTA Trend Net [Short] Exposure to Global Equities at 2.9%ile since 2011), dangerously occurring hand-in-hand with “extreme Negative $Delta” (US Equities Index / ETF Net $Delta 1%ile since 2013 going into yday) and “Short Gamma” (6%ile since 2013) within Options positioning, primarily due to the impact of outstanding legacy Hedges, which as always is a combustible dynamic which will then tend to act as “fuel for a melt-up” with the “right” macro catalyst acting to then “light the flame”

Specifically regarding this Options positioning, the event-risk of yesterday’s “most important US CPI print ever”—but in conjunction with relatively “light” underlying Equities exposure–meant:

1) copious legacy Downside hedging on the threat of hawkish market impulse from another “hot inflation” print scenario, which would then press to downside as they went ITM, juxtaposed to,

but alongside 2) a TON of short-dated and extremely CONVEX Upside optionality BOT by clients (both 13Oct and 14Oct Calls) in the case of a CPI “miss” then kicking-off a profound Stock rally…all due to this very “known” under-positioning dynamic, leaving Equities susceptible to a violent “short-squeeze” potential from clients who don’t have any “net length” / low historical exposure vs high historical “cash”

Accordingly, the market was absolutely COILED for a binary move, but particularly tilted towards Upside lift-off, due to said potent mix of 1) the UK / Macro “left tail” then turning into a “right tail” outcome, alongside these 2) extreme positioning dynamics set to be released around 3) a massive (inflation-based) event-risk then “clearing”

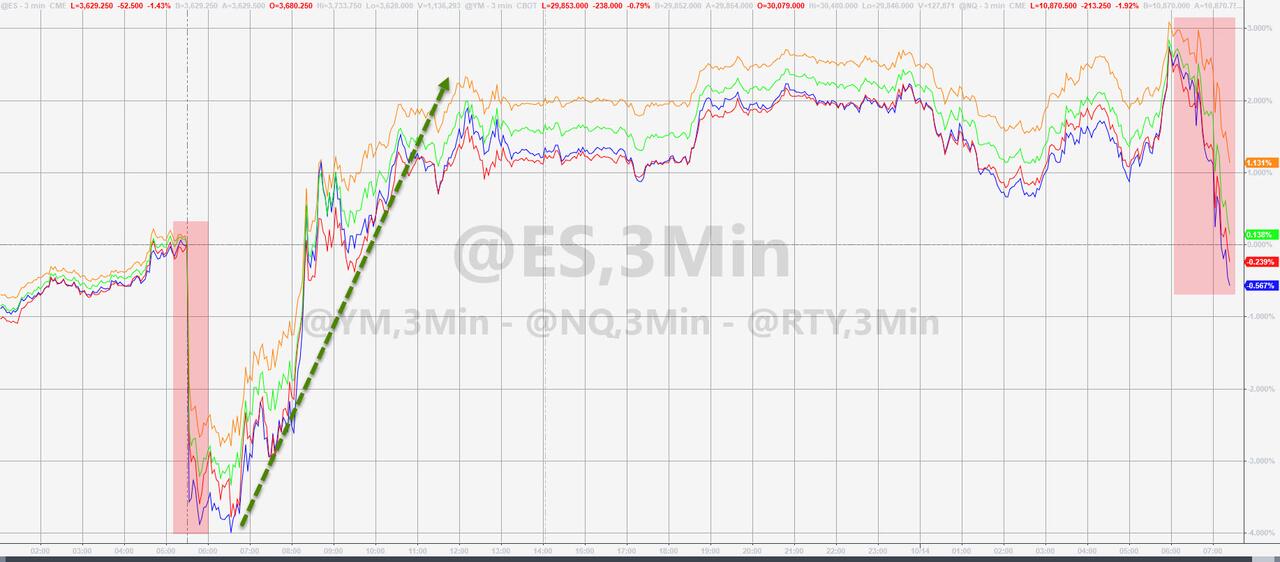

But in the “peak perversion” that makes markets so grotesquely beautiful, the US CPI print went “wrong way” for risk, with another “hot inflation” upside surprise opening the door for that panic downside push in Equities, as Fed Terminal Rate projections again exploded higher and added over a full new hike, pressing ever-closer to 5.00% (hit 4.945 at highs, 4.865 last)

S&P futures gapped -3.7% in the one minute following the CPI release (!), as this fresh “worst-case-scenario” then hit, as Puts picked-up Delta / Calls went deep OTM and dynamic hedgers pressed Shorts in the hole to fresh 2 year lows in S&P, coinciding with UST 10Y Yields exploding to 14 year highs / UST 2Y Yields to 15 year highs

BUT…and exactly as I have been documenting all year—the gap lower in Equities then saw the “new Options muscle memory 1.0” kick-in, with an almost immediate MOVE TO MONETIZE DOWNSIDE / Sell Puts, as traders wisely refuse to get too greedy in a year of so few winners, and “lock-in” accumulated wins from said hedges instead…

{kind=link}

Source: Nomura

And thereafter, in what I’d call “new Options muscle memory 2.0,” traders then looked to exploit the impact that the closing / monetization of Downside Puts will have on Spot markets then RALLYING (as Dealers close “short hedges” and have to BUY FUTURES) by buying loads of fresh super-convex (highly sensitive to price / delta chg) 0 and 1 days-to-expiration Upside Calls across single-name, ETF and Index

INTRADAY GREEKS SHOWING CALLS BEING BOT FROM THE “GET GO” IN LEVERAGED RETAIL FAVORITE OPTIONS LIKE TQQQ

{kind=link}

Source: Nomura

BUT ALSO SEEING THE DUAL POSITIVE $DELTA IMPACT OF “PUTS SOLD” AND “CALLS BOT” ACROSS OTHER BELLWETHERS LIKE TSLA:

{kind=link}

Source: Nomura

Net / Net, this dynamic of “Gap down in Equities >> Puts monetized and Calls YOLO’ed = massive Positive Net $Delta flows” (Puts sold, Calls bot) once again repeated itself, as per 2022 script…with “historic” 1d Positive Net $Delta flows / ranks in US Equities (+$154.6B, 96%ile 1d +++ Delta) then helping drive a +5.6% rally off the lows in a 6 hour period thereafter.

But in the way bigger picture, think about yesterday’s incredible price action (5th largest intraday reversal from a low in the history of the S&P 500, and the 4th largest in the history of the Nasdaq Comp—h/t @sentimentrader) like this:

IF YOU DIDN’T COVER EQUITIES SHORTS / MONETIZE YOUR DOWNSIDE ON A HOT CPI PRINT (which as least gave you a lower entry point to begin covering / monetizing on the initial gap-down)—YOU’D HAVE INSTEAD BEEN DOING IT ON A +6% DAY YESTERDAY AND ANOTHER +4% DAY TODAY IN THE CASE OF A CPI MISS

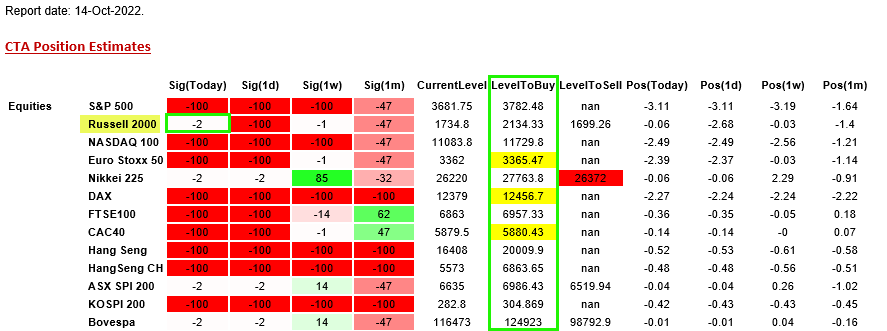

The “mechanical” and unemotional flows around Options hedging then—as so often is the case—knocked-on into Systematics, where we saw the prior CTA Trend model’s Russell 2000’s “-100% Short” signal then trigger a “buy to cover” in standard CTA “disciplined & rules-based” risk-management practice, covering nearly the entirety of said “Short” and moving to now just “-2% Short” signal, which implied +$10.1B of futures to be bot as per market conditions, and is rationally the crucial flow behind Russell Future’s +7.0% “low to high” rally since yesterday into the overnight

And further for today, we see Eurostoxx, DAX and CAC all in-play to cover half their current “-100% Short” and see the signal reduced to “-51% Short”

{kind=link}

Source: Nomura QIS

So now the latest in our series of ongoing “Trillion Dollar Questions” – will the YTD trader muscle-memory of “monetize gap down days then reload fresh downside” occur once again, after having just (at least temporarily) “solved-for” a major point of systemic stress with the UK “unfunded tax cut” reversal…and into an EPS season which is eerily looking like Q2 again, which acted as launch-point for the big Summer rally off horrible expectations which provided a “low bar” to surpass?

To this point on earnings, we’ve seen similar “pervasive negativity” into this Q3 reporting season as we did into what was the Q2 “trap” around the Summer’s massive Equities rally, with extremely low expectations based-upon the idea that top-down slowing growth and weakened consumer will see lower volumes / sales and concerns around Dollar strength…but instead, you continue seeing “inflation as a tailwind” to companies like PEP who beat and raised via this exhibition of ongoing “pricing power,” as well as companies like DAL (big forecast BEAT) noting that the consumer health remains robust “Our consumer will be in a very good place,” meshing with recent BAC commentary that the consumer is “in good shape,” while also noting that *DELTA: STRENGTH OF DOLLAR NOT AFFECTING INTERNATIONAL DEMAND

Going forward, we are gonna need more follow-through with fresh flows to push us closer to big “mechanically stabilizing / next buy trigger levels for systematics:

With CTA Trend “buy to cover” levels, we currently remain approx 2.8% away from ES1 “buy trigger” at 3782 and +5.8% away from NQ1 at 11,730…

{kind=link}

And for now, yesterday’s post-CPI gains have been erased…

{kind=link}

3700 is now the key level as it’s the biggest gamma strike on the board.

Tyler Durden

Fri, 10/14/2022 – 10:55