42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

September Unemployment Rate Tumbles As Payrolls Print Above Expectations, Lowest Since April 2021

Ahead of today’s jobs report, in its scenario analysis JPM said that a print above 260K (or where Bloomberg consensus is) would be slightly negative for stocks, as it “would hurt the loosening labor market narrative we heard since the below-expected JOLTS number”, and sure enough one look at the puke in stocks moments after the BLS released the report would imply that the September nonfarm payrolls came in this particular bucket – just barely – printing at 263K, fractionally above the consensus estimate of 255K, and well below the unrevised August print of 315K (which as a reminder came in very hot compared to expectations). Notably, while not disastrous, the September print was the lowest since April 2021 and it continues to decline at a gradual pace at least until the midterms after which we fully expect it to collapse into negative territory as the BLS catches up with reality.

{kind=link}

The change in total nonfarm payroll employment for July was revised up by 11,000, from +526,000 to +537,000, and the change for August remained at +315,000. After revision, employment gains in July and August combined were 11,000 higher than previously reported.

If the headline payrolls was hardly a shock, then the average hourly earnings number was a total snoozer: rising at 0.3% from August, and 5.0% from a year ago, average hourly earnings came in right on top of expectations. The former number was also unchanged from the 0.3% increase in August, while the latter dropped from a 5.2% Y/Y increase one month ago.

{kind=link}

Just as boring was the average workweek for all employees on private nonfarm payrolls which was 34.5 hours for the fourth month in a row. In manufacturing, the average workweek for all employees was unchanged at 40.3 hours, and overtime held at 3.2 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls increased by 0.1 hour to 34.0 hours.

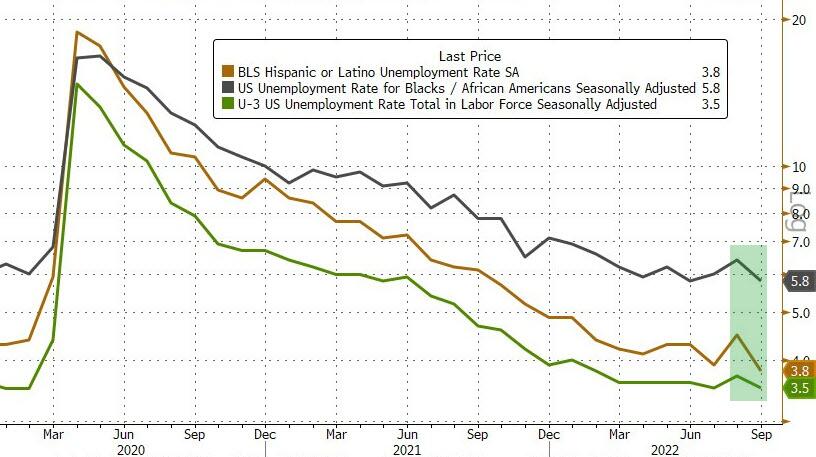

But while the payrolls number and the wage growth were both boring, what traders focused on was the ongoing collapse in the unemployment rate, which unexpectedly tumbled to 3.5% from 3.7%, well below expectations of an unchanged print. This was the result of a ~250K drop in unemployed workers, which slumped from just over 6 million to 5.753 million, even as the civilian labor force remained roughly unchanged (down to 164.689 million in Sept from 164.746 million in August). This was the data piece that gives the hawks the most ammunition; the underemployment rate dropped to 6.7% from 7% indicating less slack in the labor force.

{kind=link}

Of particular note here is the sharp collapse in both hispanic and black unemployment: among the major worker groups, the unemployment rate for Hispanics decreased to 3.8% in September (a record low), while that for Blacks tumbled to 5.8%, bringing the differential between it and the broader unemp rate to one of the lowest ever.

{kind=link}

How can the unemployment rate keep falling when the Fed is already crushing the economy? Well, as Alan Ruskin of Deutsche Bank pointed out earlier this week, the modern history of Fed tightening shows it takes quite some time for the job market to weaken after a tightening cycle begins. The current lack of progress in slowing things down isn’t unusual. He found that in eight out of nine significant hiking cycles going back to the 1970s, the unemployment rate was actually lower one year after the Fed started hiking.

And speaking of the modest decline in the civilian labor force, which took place as the civilian noninstitutional population rose modestly to 264.356MM from 264.184MM, this naturally pushed the participation rate slightly lower from 62.4% in August to 62.3% in September.

{kind=link}

Some more details from the report:

Among the unemployed, the number of permanent job losers decreased by 173,000 to 1.2 million in September. The number of persons on temporary layoff changed little at 758,000.

The number of long-term unemployed (those jobless for 27 weeks or more) was little changed at 1.1 million in September. The long-term unemployed accounted for 18.5 percent of all unemployed persons.

The labor force participation rate was little changed at 62.3 percent in September, and the employment-population ratio was unchanged at 60.1 percent. Both measures are 1.1 percentage points below their values in February 2020, prior to the coronavirus (COVID-19) pandemic.

The number of persons employed part time for economic reasons decreased by 306,000 to 3.8 million in September. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs.

The number of persons not in the labor force who currently want a job was little changed at 5.8 million in September and remains above its February 2020 level of 5.0 million. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

Among those not in the labor force who wanted a job, the number of persons marginally attached to the labor force was little changed in September at 1.6 million. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, increased by 119,000 to 485,000 in September.

Separately, the consequences of Covid still linger as the following details reveals:

In September, 5.2 percent of employed persons teleworked because of the coronavirus pandemic, down from 6.5 percent in the prior month. In May 2020, the first month these data were collected, 35.4 percent of employed persons teleworked because of the coronavirus pandemic.

In September, 1.4 million persons reported they had been unable to work because their employer closed or lost business due to the pandemic–that is, they did not work at all or worked fewer hours at some point in the 4 weeks preceding the survey due to the pandemic. This measure is down from 1.9 million in the previous month and from 49.8 million in May 2020.

Among those not in the labor force in September, 452,000 persons were prevented from looking for work due to the pandemic, little changed from the prior month. In May 2020, 9.7 million persons were prevented from looking for work due to the pandemic. (To be counted as unemployed, by definition, individuals must be either actively looking for work or on temporary layoff.)

Next we go through the major job categories in a month when total nonfarm payroll employment increased by 263,000 in September. Monthly job growth has averaged 420,000 thus far in 2022, compared with 562,000 per month in 2021. In September, notable job gains occurred in leisure and hospitality and in health care.

Leisure and hospitality added 83,000 jobs in September, in line with the average monthly job gain over the first 8 months of the year. Within the industry, employment in food services and drinking places rose by 60,000 in September. Employment in leisure and hospitality is below its pre-pandemic February 2020 level by 1.1 million, or 6.7 percent.

Employment in health care rose by 60,000 and has returned to its February 2020 level. Over the month, ambulatory health care services and hospitals each added 28,000 jobs.

Employment in professional and business services continued its upward trend in September (+46,000). Thus far in 2022, job growth in the industry has averaged 72,000 per month. Employment in temporary help services continued to trend up (+27,000) in September. Job gains occurred in investigation and security services (+9,000) and in scientific research and development services (+5,000). Job losses occurred in business support services (-12,000), legal services (-5,000), and advertising and related services (-5,000).

Manufacturing employment continued to trend up in September (+22,000). Job gains occurred in motor vehicles and parts (+8,000), fabricated metal products (+6,000), and electrical equipment and appliances (+3,000). Printing and related support activities lost 4,000 jobs over the month. Manufacturing has added an average of 36,000 jobs per month thus far in 2022. In September, employment in construction continued to trend up (+19,000), in line with average monthly job growth in the first 8 months of this year. Specialty trade contractors added 18,000 jobs in September.

Employment in wholesale trade continued its upward trend in September (+11,000). Wholesale trade has added an average of 18,000 jobs per month thus far in 2022.

Employment in financial activities changed little (-8,000), as declines in insurance carriers and related activities (-9,000) and nondepository credit intermediation (-7,000) were partially offset by a job gain in depository credit intermediation (+5,000).

Employment in transportation and warehousing was little changed in September (-8,000). A loss of 11,000 jobs in truck transportation was partially offset by a gain of 3,000 jobs in air transportation.

Hammering a point noted earlier by Goldman, Andrew Hunter, senior US economist at Capital Economics, said that payroll growth was depressed by fewer teachers than “normal” returning for the new school year. If you remove the 29,000 decline in state and local government education jobs, then payrolls were even stronger in September. Also, as this effect drops out, employment growth could pick up in the subsequent months, Hunter says.

So what does this number mean for the Fed? Here are a handful of hot takes from Wall Street:

Jefferies economists Thomas Simons and Aneta Markowska.

“To the extent that there are any implications for the Fed, the data brings us back to where we were before last month. There is not a lot of capacity for the labor force to grow, and thus strong wage pressure is going to continue to be an issue. We still expect another 75-bp rate hike in November.”

BMO’s Ian Lyngen:

“On net, it was a strong enough read to keep a 75-bp Nov hike as the path of least resistance, but the deceleration in wage growth YoY adds to the case for a slowed hiking pace to 50-bp in December, and we still expect the final 25-bp hike in February to reach terminal.”

Morgan Stanley ’economists Ellen Zentner:

“Still-solid jobs growth in combination with a drop in the participation rate do not point to much relaxation in the labor market. We continue to see the current data environment providing little room for a Fed pivot to a lower pace of rate hikes in the near term, in particular in light of our expectations for another strong reading in next week’s CPI.”

Jeffrey Rosenberg, BlackRock senior portfolio manager

“The unemployment rate and the labor-force participation rate is why there’s a negative reaction in equity futures. This is a slight disappointment relative to hopes that this report would give a piece of evidence in favor of the camp that there’s a slowdown and a pivot underway.”

Anna Wong, chief US economist at Bloomberg Economics:

“The robust September jobs report significantly bolsters the case for a fourth consecutive 75-basis-point hike at the November FOMC meeting. The labor market remains tight and the supply of workers isn’t growing fast enough to bring down wage growth. Adjusted for slowing productivity growth, wage growth is running at least triple the pace consistent with the Fed’s price target. Concerns about a wage-price spiral will keep the Fed hiking well into 2023 until rates reach 5%, in our view.”

Peter Tchir, chief strategist at Academy Securities

“I was looking for a “bad news” is “good news” trading day (higher stocks with lower bond yields), and now am stuck watching for the initial reaction (which has been “modest” by recent standards) to reverse based on positioning and “meh” not bad or good data. I’d look for bonds to reverse early losses first, as we head into a long weekend where geopolitical risk remains non-trivial and in fact is quite real across the globe.”

Bottom line: the number is too important and too political to be allowed to tumble two months before the midterms and so it won’t. Instead, we need to wait until after November 8 to find out the full extent of the Fed’s rate hike devastation on the US labor market.

Tyler Durden

Fri, 10/07/2022 – 08:43