42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Nearly Half Of Americans Making Six-Figures Living Paycheck To Paycheck

Roughly 60% of Americans say they’re living paycheck to paycheck – a figure which hasn’t budged much overall from last year’s 55% despite inflation hitting 40-year highs, according to a recent LendingClub report.

{kind=link}

Even people earning six figures are feeling the strain, with 45% reporting living paycheck to paycheck vs. 38% last year, CNBC reports.

“More consumers living paycheck to paycheck indicates that many are continuing to lose their financial stability,” said LendingClub financial health officer, Anuj Nayar.

The consumer price index, which measures the average change in prices for consumer goods and services, rose a higher-than-expected 8.3% in August, driven by increases in food, shelter and medical care costs.

Although real average hourly earnings also rose a seasonally adjusted 0.2% for the month, they remained down 2.8% from a year ago, which means those paychecks don’t stretch as far as they used to. -CNBC

Meanwhile, Bank of America found that 71% of workers say their income isn’t keeping pace with inflation – resulting in a five-year low in terms of financial security.

{kind=link}

“It is no secret that prices have been increasing for everyday Americans — not only in the goods and services they purchase but also in the interest rates they’re paying to fund their lives,” said Nayar, who noted that people are relying more on credit cards and carry a higher monthly balance, making them financially vulnerable. “This can have detrimental consequences for someone who pays the minimum amount on their credit cards every month.”

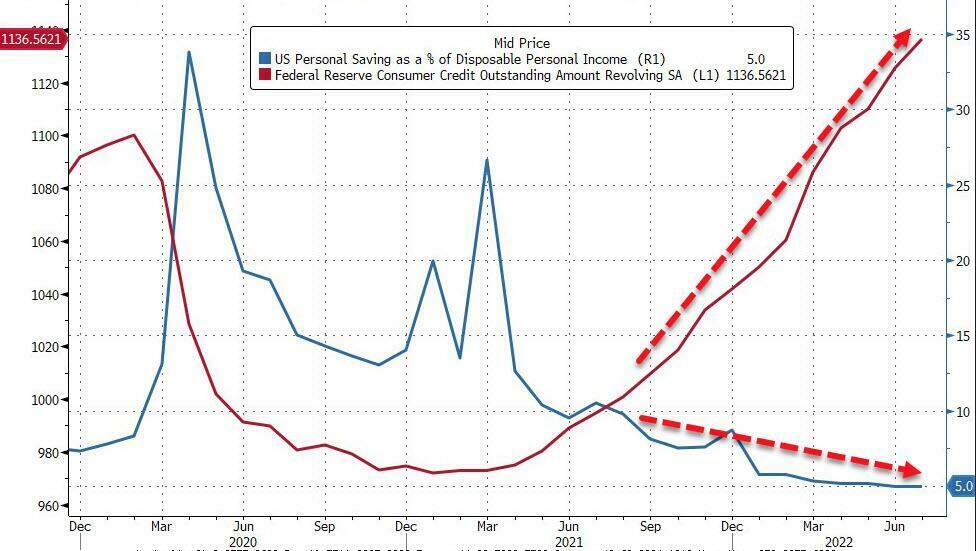

According to an Aug. 30 report from the Federal Reserve Bank of New York, credit card balances increased by $46 billion from last year, becoming the second-biggest source of overall debt last quarter.

{kind=link}

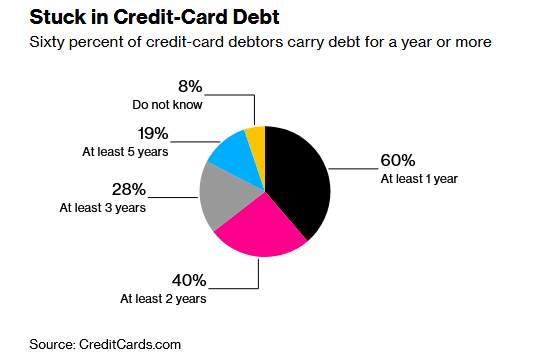

And as Bloomberg noted last month, more US consumers are saddled with credit card debt for longer periods of time. According to a recent survey by CreditCards.com, 60% of credit card debtors have been holding this type of debt for at least a year, up 50% from a year ago, while those holding debt for over two years is up 40%, from 32%, according to the online credit card marketplace.

{kind=link}

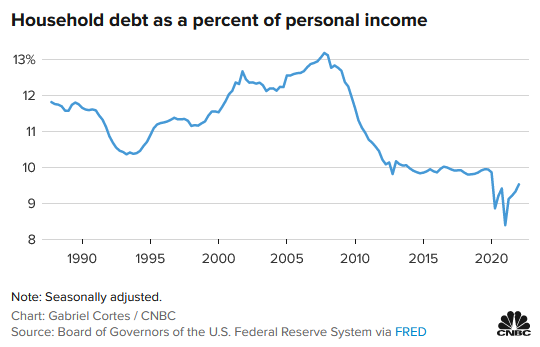

And while total credit-card balances remain slightly lower than pre-pandemic levels, inflation and rising interest rates are taking a toll on the already-stretched finances of US households.

About a quarter of respondents said day-to-day expenses are the primary reason why they carry a balance. Almost half cite an emergency or unexpected expense, including medical bills and home or car repair.

The Federal Reserve is likely to raise interest rates for the fifth time this year next week. Credit-card rates are typically directly tied to the Fed Funds rate, and their increase along with a softening economy may lead to higher delinquencies.

Total consumer debt rose $23.8 billion in July to a record $4.64 trillion, according to data from the Federal Reserve. -Bloomberg

The Fed’s figures include credit card and auto debt, as well as student loans, but does not factor in mortgage debt.

Tyler Durden

Tue, 10/04/2022 – 20:25