42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Goldman’s Credit-Card Losses Are Soaring – “Well Above Subprime Lenders”

In 2018, we explained how Goldman Sachs had switched from betting against Subprime (Residential Mortgage Backed Securities and their various synthetic and “squared” derivatives) to betting with Subprime (hoping to profit off America’s sub-660 FICO population by lending to it).

Goldman’s credit card business, anchored by the Apple Card since 2019, has arguably been the company’s biggest success yet in terms of gaining retail lending scale, but rising losses threaten to mar that picture.

{kind=link}

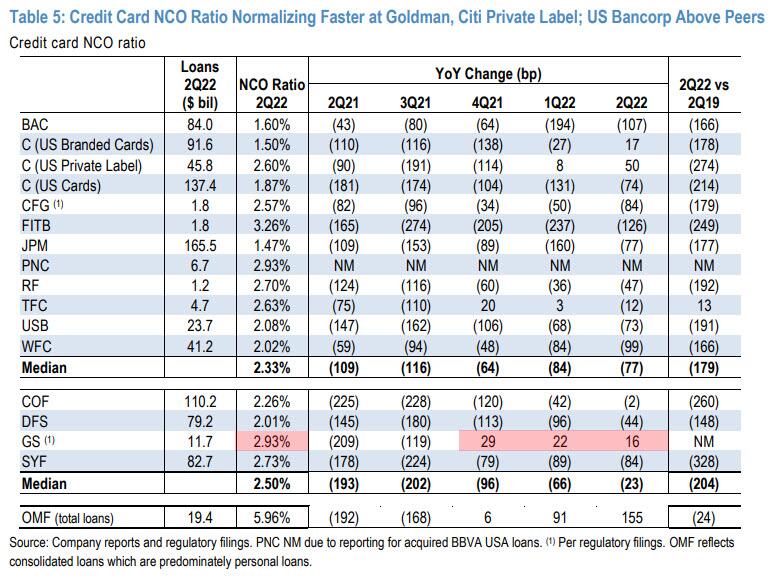

But now, post the COVID money-drop and various moratoria on payments/bankruptcies/delinquencies, the fecal matter appears to be starting to strike the rotating object as JPMorgan note points out that while competitors like Bank of America enjoy repayment rates at or near record levels, Goldman’s loss rate on credit card loans hit 2.93% in the second quarter.

{kind=link}

That’s the worst among big U.S. card issuers and “well above subprime lenders,” according to JPM analyst Vivek Juneja.

Even more notably, Goldman’s losses are also higher than that of Capital One, the largest subprime player among big banks, which had a 2.26% charge-off rate.

“If there’s one thing Goldman is supposed to be good at, its risk management,” said Jason Mikula, a former Goldman employee who now consults for the industry.

“So how do they have charge-off rates comparable to a subprime portfolio?”

None of that should come as a surprise though since, as the FT reported in 2018 citing analysts, Goldman has been targeting riskier borrowers, supplying about one-fifth of its loans to people with credit scores below 660 on the commonly used FICO scale; there is a familiar name for this group of borrowers: “subprime.”

And now, four years later, as CNBC reports, more than a quarter of Goldman’s card loans have gone to customers with FICO scores below 660, according to filings. That could expose the bank to higher losses if the economy experiences a downturn, as is expected by many forecasters.

“People are losing their jobs and you had inflation at 40-year highs; that will impact the subprime cohort more because they are living paycheck to paycheck,” Michael Taiano, a senior director at Fitch Ratings, said in an interview.

“With Goldman the question will be, were they growing too fast into a late-cycle period?”

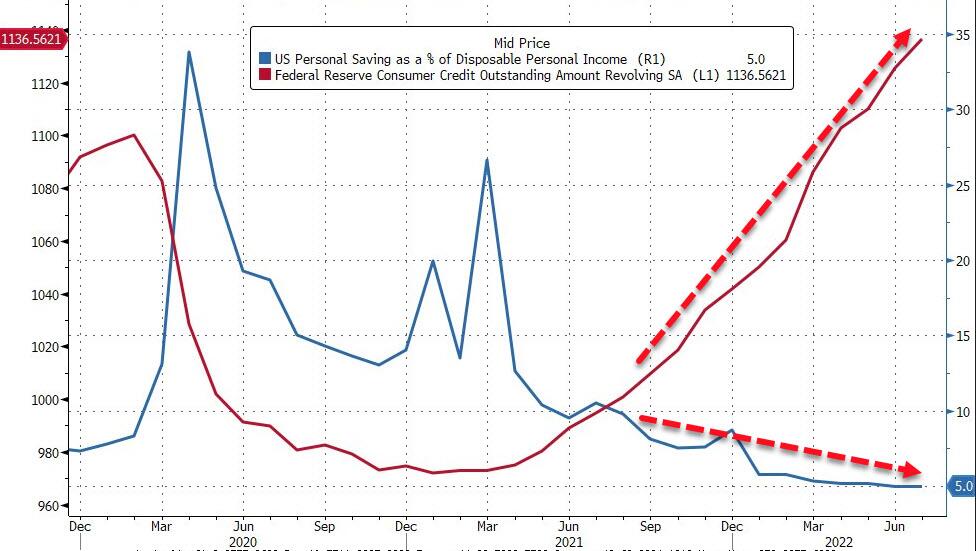

Savings rates are collapsing, forcing Americans to use their credit cards to maintain living standards as prices for everything soar…

{kind=link}

“Goldman’s credit card net change-off ratio has risen sharply in the past 3 quarters,” Juneja wrote…

{kind=link}

That is happening “despite unemployment remaining very low at 3.7% in August, similar to 2019 levels.”

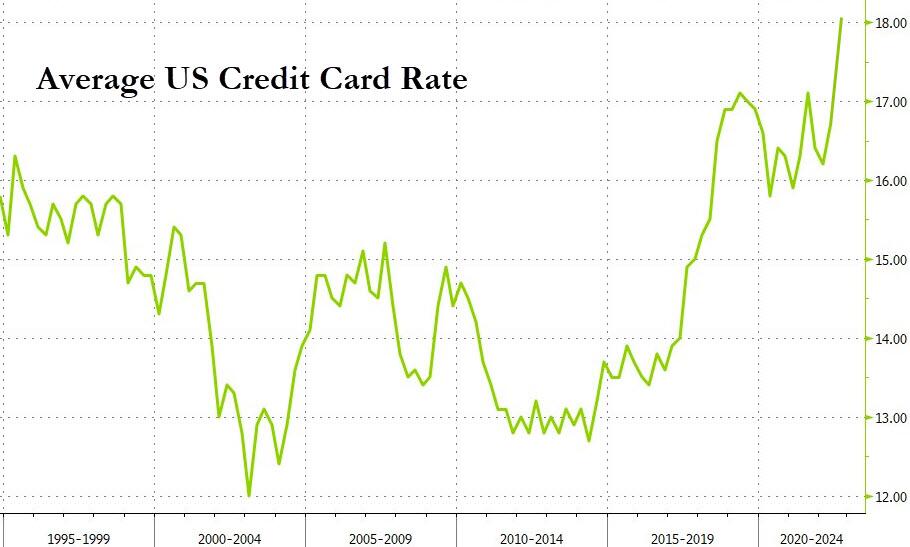

Simply put, after a period in which borrowers strengthened by pandemic stimulus checks repaid their debts like never before, it is the industry’s “newer entrants” that are “showing much faster weakening” in credit metrics… and rising credit card rates won’t help…

{kind=link}

As CNBC concludes, the difficulties seem to confirm some of the skepticism Goldman faced when it beat out established card players to win the Apple Card account in 2019. Rivals said that the bank could struggle to reach profitability on the no-fee card.

“Credit cards are a hard business to break into,” said Taiano, the Fitch Ratings director.

“Goldman already faces higher losses because their book of business is young. But when you layer on worse unemployment, you are exacerbating that trend.”

In 2018, quoted by the FT, CEO at the time, Lloyd Blankfein said Goldman was “being very careful” in its development of Marcus, “growing very slowly and deliberately with a lot of controls”, so that people do not take out loans they cannot afford to pay back.

It appears that all went out the window as ‘stimmies’ sparked a panicked rush for customers… and remember we are still ‘not in a recession’ and Americans are enjoying what Biden proclaimed “the strongest economy ever.”

Or maybe this surge in charge-offs at Goldman is the canary in the ‘consumers are strong’ coalmine.

Tyler Durden

Tue, 09/13/2022 – 06:55