42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Economic Slowdown Now, Recession Coming In 2023

Authored by Lance Roberts via RealInvestmentAdvice.com,

Economic slowdown but no recession! That message comes from the latest employment report, service sector data, and Federal Reserve.

“We’re not in a recession right now. We do have these two-quarters of negative GDP growth. To some extent, a recession is in the eyes of the beholder. With all the job growth in the first half of the year, it’s hard to say there’s a recession. With a flat unemployment rate at 3.6%, it’s hard to say there’s a recession.” – James Bullard, St. Louis Federal Reserve President

Such a statement certainly belies much of the economic consensus that two-quarters of negative economic growth constitutes a recession. As shown, the latest GDP report indeed met that measure.

{kind=link}

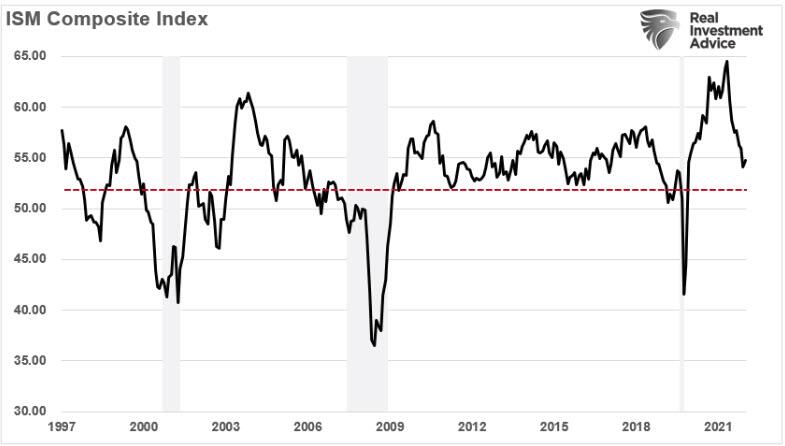

However, as stated, some indicators suggest the economy is in a slowdown but not yet in a recession. For example, our composite Institute Of Supply Management (ISM) survey is still in expansionary territory. Since services make up about 80% of the economy today, there is currently support for economic growth. However, the data trend is negative and supports the view of an economic slowdown.

{kind=link}

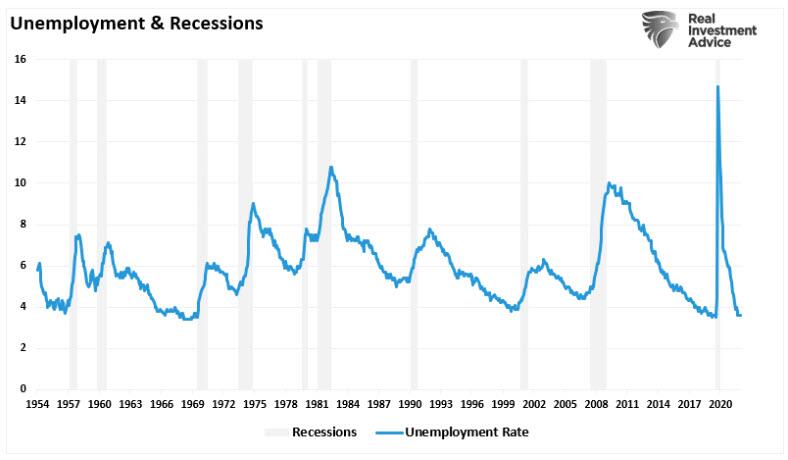

Employment also remains extremely strong. With the unemployment rate near historic lows, such does support the statement a recession is not underway. However, low unemployment rates are historically pre-recessionary and will reverse quickly as a recession takes hold.

{kind=link}

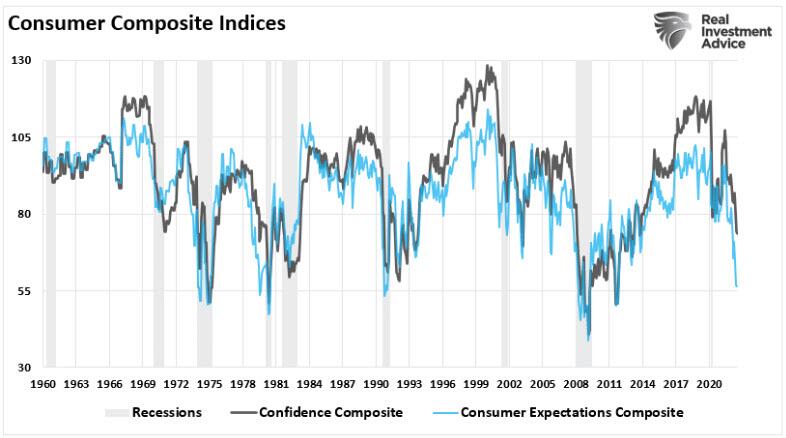

While neither measure suggests the economy has entered a recession yet, such does not preclude one from occurring. Many indicators suggest individuals “feel” like the economy is in a recession, such as our composite consumer sentiment index. Historically, a recessionary environment was present when consumer confidence and expectations declined below 80.

{kind=link}

Notably, given short-term economic dynamics, we could see a bump in economic growth due to back-to-school spending in Q3 and holiday shopping in Q4.

However, I suspect that as the Fed continues its aggressive mission to combat inflationary pressures, a recession in 2023 is likely.

The Fed’s Fight

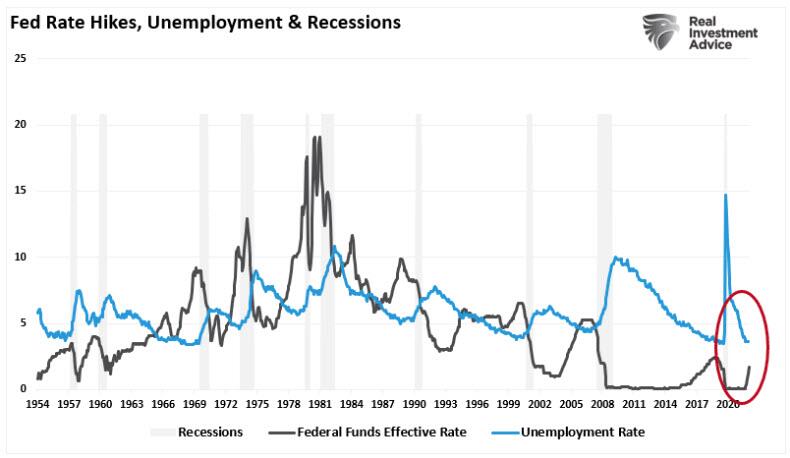

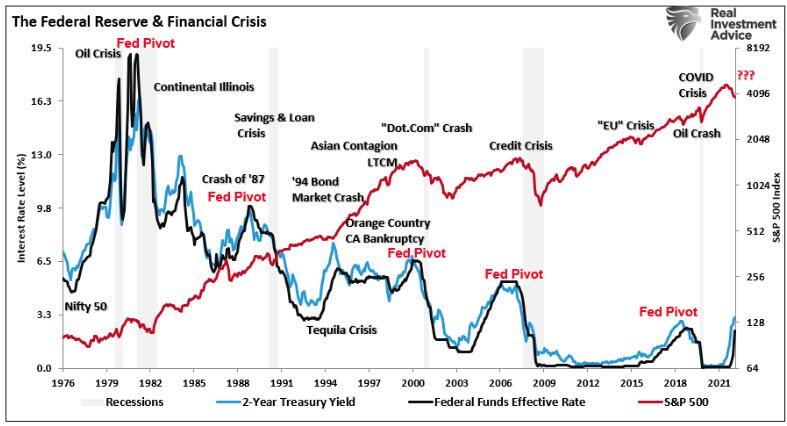

While James Bullard, and others currently directing the monetary policy regime, suggest they can quell inflation with only an economic slowdown, history suggests otherwise. Such is because the Fed makes its policy decisions based on lagging economic data.

As noted previously, the Fed is basing its ability to hike based on strong employment rates. However, historically, the Fed hikes rates to a point where “something breaks.”

{kind=link}

That breaking point occurs because the real-time economy adjusts to monetary policy changes. However, data such as employment and inflation can take several months to catch up to the actual economy.

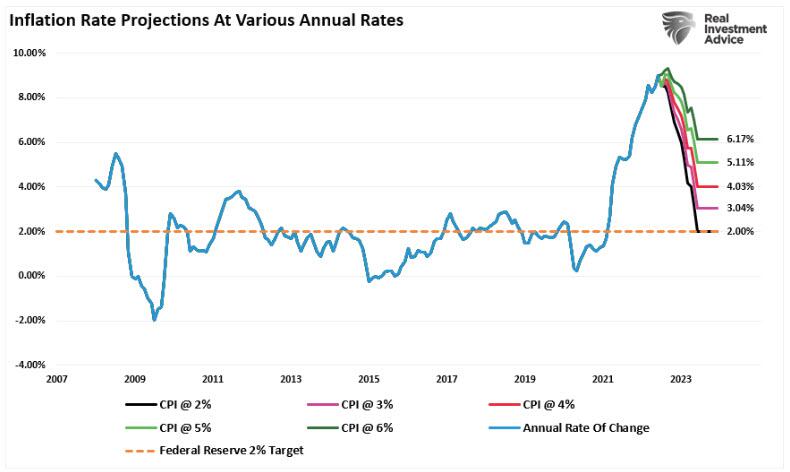

Notably, roughly 40% of CPI is Home Owners Equivalent Rent which has roughly a 3-month lag. As shown, if inflation slows dramatically to just 2% annualized, it will take until the end of 2023 to return to the Fed’s target rate. Any higher rate of growth keeps inflation elevated much longer.

{kind=link}

Given this lag effect, the Fed will continue lifting rates to slow economic demand to bring inflation back to its target. However, the actual impact on consumers and economic activity is not reflected in CPI on a timely basis. Such creates the probability of the Fed over-tightening monetary policy, turning an economic slowdown into a more severe economic contraction.

Of course, this is what history tells us will happen.

{kind=link}

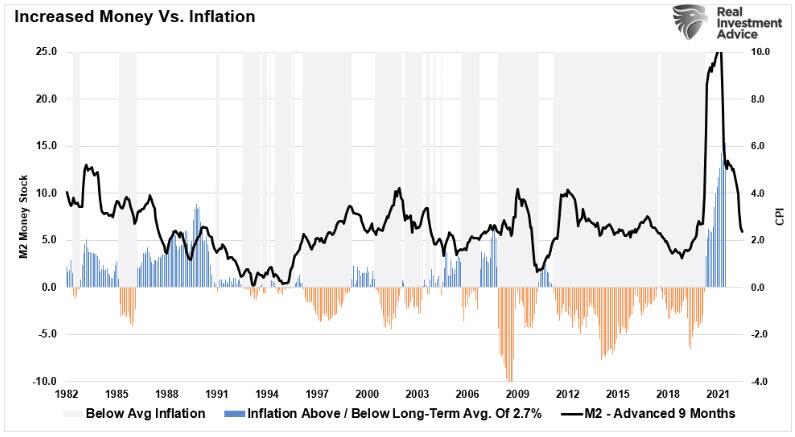

Monetary supply also tells us the Fed is likely making a mistake with its current aggressive stance on inflation. As discussed recently, inflation is the consequence of restricted supply due to the economic shutdown and increased demand from “stimulus” checks. The massive surge in M2 money supply has reversed and has about a 9-month lead on inflation.

{kind=link}

While the Fed is hiking rates to quell inflation, the contraction of the money supply is doing the job for them.

Driving With The Rearview Mirror

There is little doubt we are amidst an economic slowdown. With the Federal Reserve focused on combatting inflation by tightening monetary policy, thereby slowing economic demand, logic suggests that economic data trends will continue to decline.

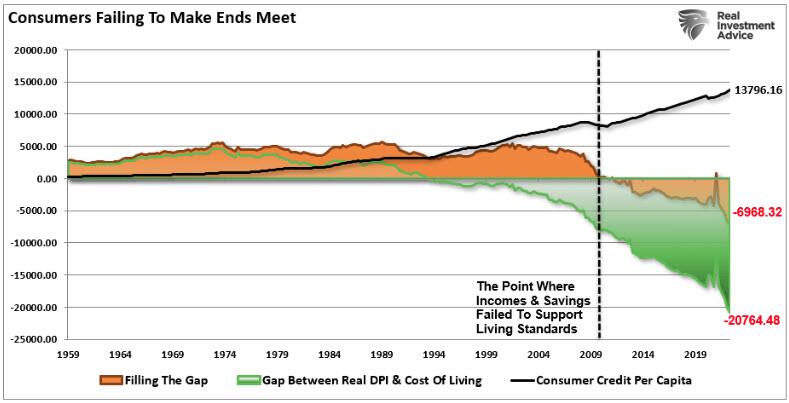

As the Fed continues to hike rates, each hike takes roughly 9-months to work its way through the economic system. Therefore, the rate hikes from March 2020 won’t show up in the economic data until December. Likewise, the Fed’s subsequent and more aggressive rate hikes won’t be fully reflected in the economic data until early to mid-2023. As the Fed hikes at subsequent meetings, those hikes will continue to compound their effect on a highly leveraged consumer with little savings through higher living costs. We have shown previously that the consumer is exceptionally unprepared for such an outcome.

{kind=link}

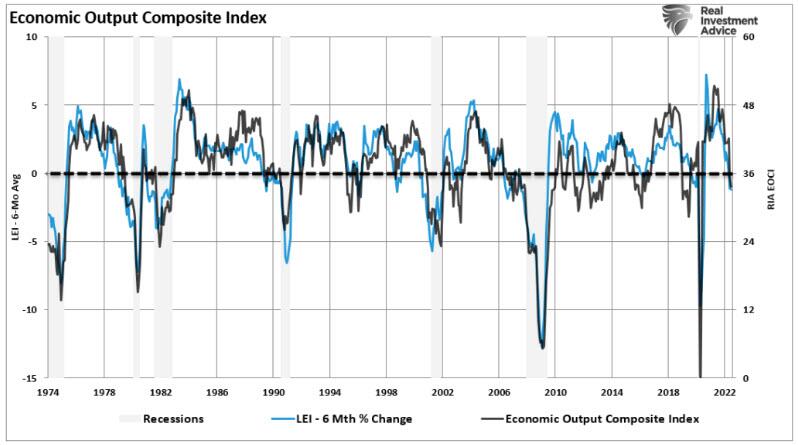

Given the Fed manages monetary policy in the “rear view” mirror, more real-time economic data suggests the economy is rapidly moving from economic slowdown toward recession. The signals are becoming clearer from inverted yield curves to the 6-month rate of change of the Leading Economic Index.

{kind=link}

The media, and the White House, will likely proclaim victory by stating the first two quarters of 2022 were not a recession but only an economic slowdown. However, given the lag effect of changes to the money supply and higher interest rates, indicators are pretty clear recession risk is very probable in 2023.

For investors, such suggests the current market rally is not the beginning of a new bull market. Instead, investors will likely get lured into a bear market rally with disappointing outcomes.

Currently, investors are hoping to catch “the Fed pivot market bottom,” however, in a bear market, it often pays to be late rather than early.

Tyler Durden

Tue, 08/16/2022 – 11:20