42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Stockman: How The C-Suite Embraced Lockdowns And Economic War

Authored by David Stockman via The Brownstone Institute,

A while back, corporate America was bending over backwards to appease the Virus Patrol with lockdowns, mandatory masking and threats to fire anyone who didn’t take the Jab.

{kind=link}

This was supposedly owing to the “science,” but it has long been evident that the latter was a limpid cover story. Big Business complied because the business culture of the corporate elites has become deeply confused and even corrupt.

Their stocks being vastly overvalued owing to the Fed’s relentless and egregious monetary expansion, the C-suites have lost track of their #1 duty—profit maximization. The latter has been sacrificed to corporate virtue signaling, head pats from the politicians and invitations to White House soirees.

These corporate “statesmen” get all the above psychic rewards, plus mighty fat stock option enrichment, too, because the Fed won’t see it any other way. They are pleased to call it “wealth effects” policy, when the truth is it is market-wrecking and wealth-destroying policy.

The utter economic waste and injustice to employees, shareholders, and various other stakeholders brought on by the new corporate virtue signaling is now starkly evident in the global data that prove beyond a shadow of doubt that the whole Virus Patrol-dictated anti-Covid regime was completely wrong from the very beginning.

Ironically, the smoking gun evidence comes from South Korea, which is a hot-house case of state-dominated capitalism, if there ever was one. The so-called Chaebols take their marching orders from the state in return for unfettered access to state fiscal subsidies and protectionist trade arrangements that shield them from the rigors of free market competition.

In any event, South Korean businesses complied rigorously with the government’s absurd efforts to stamp out the Covid with what amounted to a corporate-administered totalitarian regime that actually made the Fauci’s and Scarf Ladies of Washington drool with envy.

Accordingly, during 2020 and 2021, South Korea chased zero Covid with strict border controls, aggressive testing and tracing, and a vaccination campaign that reached nearly its entire adult population with mRNA (and some DNA) shots. In fact, the latest data show that 87% of the population is fully vaxxed and fully 60% have taken the booster.

Still, the country didn’t quite get to zero. Infections and deaths rose slowly last year. But it came close enough that the usual highly credentialed “public health experts” held it up as a beacon of light:

For instance, one seer argued,

Maximum suppression helped buy time for scientists to get to work, and therefore find a sustainable exit from the crisis… The pivot from maximum suppression to mass vaccination was a rational and logical shift to achieve a successful transition out of the pandemic.

Never have the so-called “experts” been so completely blindsided. Here is what has happened to the Covid-free nation of South Korea. Namely, the scoreboard suddenly went tilt:

The South Korean case rate has soared to an off-the-charts 7,800 per million, which is 86X the current US rate of 91 per million;

The current sky-high South Korean rate is 3.3X the all-time high experienced by the US at the Omicron peak in early 2022.

In short, the entire South Korean Covid dragnet was for naught. When Omicron came along, a population within minimal natural immunity (from Covid infection) and maximum vaccination rates turned out to be a sitting duck for new infections.

Of course, the Covid capitulation was just a warm-up for what the corporate world is doing with respect to the wartime frenzy loose in Washington and among the mainstream media.

Take the case of Pepsi, for instance. It was the pioneering US company which went to Russia during the peak of the Soviet brutality against its own citizens, but is now run by a virtue-signaling CEO, who happens to be a fellow traveler of the World Economic Forum where he chairs one of its major committees.

Back in the day when Pepsi first went to the Soviet Union—a place far more evil and barbaric than Putin’s Russia by a longshot—US companies had enough grit to fight back when Washington threatened to harm corporate interests and shareholder value.

No longer, however. Pepsi’s CEO, one Ramon Laguarta, rashly decided to stop selling Pepsi in Russia, even before Washington could get around to issuing mandatory sanctions.

So doing, Laguarta destroyed tens of billions of investment value that Pepsi had built up over five decades. And he did so, apparently, because the foolish CEO of McDonald’s closed its 850 stores in Russia first in order to get a pat on the head from the Biden administration.

The Wall Street Journal, in fact, chronicled Pepsi’s betrayal of its shareholders quite succinctly:

Pepsi in 1974 was among the first American brands to enter the Soviet Union, after a Cold War encounter in Moscow in 1959 when then-Vice President Richard Nixon offered a cup of the cola to Soviet Premier Nikita Khrushchev.

By 2022, PepsiCo Inc. had 20,000 employees in Russia and it was the company’s third-largest market after the U.S. and Mexico. The company’s 24 plants and three R&D centers in Russia made soft drinks, potato chips, milk, yogurt, cheese, baby food and baby formula.

The company’s top officials discussed the geopolitical crisis nearly every day. They were reluctant to shut down the Russian operations, according to people familiar with the matter. The leaders wanted to do right by their employees and consumers, and they were under pressure to join other Western companies making moves to penalize Russia. They also had a responsibility to shareholders.

On the afternoon of March 8, McDonald’s said it was closing its restaurants in Russia. Then Coca-Cola said it was suspending its business there. Within half an hour, PepsiCo CEO Ramon Laguarta sent a memo to staff. The company would stop selling Pepsi and 7UP in Russia, he told them, but it wasn’t pulling out.

Behind the scenes, the company’s leaders explored another action it could still take. PepsiCo could write down the value of its Russian business to zero, modeling the process it used for its Venezuelan operations in 2015.

Why wantonly destroy shareholder value? Because the Fed-corrupted markets would ignore the writedowns, that’s why.

Never mind that tens of billions of cumulative investment would be destroyed by Pepsi’s virtue signaling C-suite, its stock options-glutted executives didn’t care because the Fed-fattened stock market didn’t care, either.

Needless to say, the so-called financial press has no compunction about cheerleading for this kind of destructive C-suite virtue-signaling. The above cited WSJ article was fulsome in its praise for companies acting on political, not economic, motives:

This time, companies were more prepared. The pandemic had given leaders a crisis playbook. Years of corporate activism on issues such as climate change and racial discrimination had trained them to respond to a range of issues. The invasion took many by surprise, but they reacted quickly to what was a potentially fatal threat to their employees and also a reputational threat to their businesses.

When President Vladimir Putin launched the attack on Feb. 24, and pressure from governments and employees began to build, as well as escalating sanctions on Russia, companies moved with unusual speed and a sense of collective action. The result was a corporate participation in geopolitics with little recent precedent.

Well, they got that right, but are clueless about the danger. Namely, that neither capitalism nor democracy can thrive when business becomes a subservient tool of the state and a vessel for the expression of political fashion and social conformity.

Moreover, the idea that these capitulatory actions were undertaken by the C-suites for the purpose of reputational protection is just flat-out nonsense. Nobody was going to stop buying Pepsi and Lay’s potato chips because the parent company had a 50-year old business in Russia.

Indeed, the sheer obsequiousness and hypocrisy of the C-suites defies credulity. For instance, the Volkswagen CEO shut down his Russian plants for the practical reason of lack of parts, but nevertheless explained his action with a phony bow:

Within days of the invasion, Mr. Diess shut down or curtailed production at some of his biggest factories in Europe because the plants couldn’t get wiring harnesses from suppliers in Ukraine. The company later closed down production at its car plants in Russia, citing its “great dismay and shock” over the invasion.

At the end of the day, this kind of corporate politicking is why the Fed has run rampant printing money and generating vast asset bubbles like never before in history. The politically correct C-suites of the Fortune 500, which should be on the warpath against the Fed’s rampant monetary debasement, have not said a peep about the Fed’s destructive digression into madcap money printing.

The fact is, any one paying half attention could see that the Eccles Building has been blind to the effects of is destructive Keynesian policies for years—at least reaching back to this gob-smacker from Ben Bernanke on the eve of the Great Financial Crisis:

Thus, the Fed’s minutes from January 2008 quoted Chairman Bernanke as reassuring that—

“The Federal Reserve is not currently forecasting a recession.”

That’s right. By the official dating of the NBER (National Bureau Of Economic Research) the start of the official recession was December 2007!

That is to say, if Ben Bernanke still didn’t know a recession was underway one month after it started, why would anyone think the Fed has a clue about the state of the domestic and global economy nor the capability and wherewithal to micromanage its course into even the near-term future?

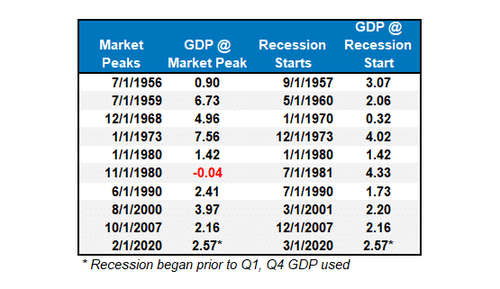

Nor was the 2008 recession a unique occurrence. The table below was put together by the astute Lance Roberts and it makes clear that the real (inflation-adjusted) economic growth rate even on the eve of recession does not always give a signal as to what is coming around the macroeconomic bend. As Roberts noted,

Each of the dates above shows the growth rate of the economy immediately prior to the onset of a recession. You will note in the table above that in 7 of the last 10 recessions, real GDP growth was running at 2% or above. In other words, according to the media, there was NO indication of a recession.

But the next month one began.

{kind=link}

With respect to the current cycle, Roberts further noted that the 2-month 2020 recession never really ended, and that we may be on the cusp of a relapse, notwithstanding the false boom stimulated by Washington print-borrow-and spending bacchanalia last year:

While the NBER declared the 2020 recession the shortest in history, such does not preclude another recession from occurring sooner than later. All the excesses that existed before the last recession have worsened since then.

Given the dynamics for an economic recession remain, it will only require an unexpected, exogenous event to push the economy back into contraction.”

And also one to push the top 1% and 10% into a world of hurt. That’s because the latter account for 85% of financial assets and 75% of household net worth, respectively.

So when the great bubble collapse finally comes, the wailing and gnashing of teeth among the wealthy households —whose brokerage accounts have been fattened beyond sanity by the Fed’s egregious inflation of financial assets— will be excruciating.

Perhaps then the C-suites will be awakened from their slumbering compliance.

Or at least, we can hope.

Tyler Durden

Sun, 03/27/2022 – 18:45