42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Macleod: The Only Replacement For Fiat Is A Currency ‘Credibly-Backed By Gold’

Authored by Alasdair Macleod via GoldMoney.com,

Rising interest rates threaten to destabilise both financial asset values and the fiat currencies in which they are priced. This outcome is feared by the chattering classes who increasingly speculate about currency resets.

So far, we have seen cryptocurrencies such as bitcoin, plans for the introduction of central bank digital currencies, plans to de-dollarise Asian trade, and even El Salvador adopting bitcoin as legal tender. But are these resets valid?

Except for a new currency mooted for cross-border trading purposes between Russia, its former Central Asian satellites and China only at the conceptual stage, all these plans fail in one important respect: as things stand, legally none of them can have the status of a currency. Money, that is physical gold and silver, banknotes and bank credit are exempt from property law with respect to stolen goods which otherwise can be seized from innocent parties who have subsequently acquired them.

Without this exemption embodied in lex mercatoria a currency replacement is useless. The only replacement for fiat is a currency credibly backed by gold. And that is the legal position!

{kind=link}

Introduction

The introduction of new currencies is a topic moving increasingly into public debate driven by both the inflation dilemma faced by central banks and, recently, by the consequences of fiat currency sanctions against Russia. There is a convergence of events at play. While there are the immediate problems of rising interest rates and of the financial and commodity price war being waged between the West and Russia, there are plans for central bank digital currencies (CBDCs) to give the monetary authorities greater control over the use of new currencies that could replace existing fiat.

The problem is that in the monetary sense the public is not even ruled by one-eyed kings; we are all subjects in the kingdoms of the totally blind, at least in the economic and monetary sense. While some very clever people can tell you all about the sophisticated financial instruments few of us have even heard of and their roles in the fiat currency universe, no one in charge appears to understand the root of it all, which is money. This unbelievable situation is easily verified by listening to the utterances of or reading the information emanating from leading central bankers and the research departments of nearly all the participants in the finance industry.

The role of money has been reaffirmed by philosophers and economists from the dawn of money itself, at least until this age of neo-Keynesianism. This quote is over 2,300 years old and is from Aristotle:

“With regards to a future exchange (if we want nothing at present, that it may take place when we do want something) money is, as it were, our security. For it is necessary that he who brings it should be able to get what he wants”

This was reaffirmed by Jean-Baptiste Say two centuries ago in his famous law which defined the role of money in the division of labour. The only form of money legal from Aristotle’s time until even today is metallic. That is gold and silver coin or bullion which can be coined or weighed and does not alter over time — the rest is credit. In the form of banknotes, credit is the circulating representation of money, which we call currency. Since the end of Bretton Woods in 1971, gold has been dismissed as the anchor for currency value by promoters of fiat currency, which is now wholly dependent upon faith and credit in their issuers, who have long forgotten the vital role of metallic money.

Metallic money was settled upon as the medium of exchange by its users, and the responsible role of the state has always been not to replace it, but to standardise it. The state had a fundamental duty to ensure the coinage was good and money’s representation as credit was sound.

That is now forgotten. Nor is the role of interest rates understood. While being a cost to a borrower, for a lender who loses the use of his money, they reflect compensation for that loss and the risk that the borrower might not repay. Included in the lender’s calculation must be an allowance for changes in purchasing power. If a lender buys, say, a 10-year US Government note and currency debasement leads to a loss of purchasing power officially recorded by the consumer price index at 7.5%, then it is likely that a cohort of lenders to the US Government would seek a similar level of compensation for this factor alone.

That is without reckoning on central banks, which suppress the evidence from their debasement policies. The Fed, which bears responsibility for the world’s reserve currency, now finds itself unable to keep the lid on rising interest rates and against its will is being forced by markets to permit them to rise. All central banks are being pushed into similar decisions. Not only are they uncomfortable with markets forcing their hand, but they firmly believe that interest rates are an unnecessary imposition on investment capital and state finances. Their response to market pressures is to enforce yet greater control over markets by redesigning their currencies. But there are insurmountable legal problems, which so far have not entered the debate.

New forms of currency face a huge legal hurdle

No one could be more ill-equipped to design a new currency than planners employed by governments. Instead of the public being permitted to satisfy its own criteria, governments try to evolve currencies away from being determined by its users towards increasing statist control.

The Bank for International Settlements, which is coordinating research into CBDCs is clear on the subject. CBDCs are intended be the equivalent replacement of cash with two key differences:

“The central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability [i.e. cash], and we will have the technology to enforce that. Those two issues are extremely important and is a huge difference to what cash is.” Augustin Carstens – BIS General Manager

But as a replacement for banknotes, a CBDC cannot share the legal status of cash today, which is specific. It is not clear whether ignoring it is intentional, or the lawyers are yet to be fully consulted.

Here is the central issue. Money, that is gold and silver, and currency in the form of banknotes and representative coin have a different legal status from all other forms of property. If the true owner of money which has been stolen finds it is in the hands of the thief, he may recover it. But if the thief has purchased things in the shop with it in the usual way of business and the shopkeeper takes it honestly in the way of his trade and without knowing it has been stolen, he may retain it against the original owner from whom it has been stolen. That is to say the right to the property in the currency passes by its delivery.

This single exception to property rights extends to substitutes and representations of money, such as bills of exchange, banknotes, cheques, and other cash substitutes exchanged for money, currency, or credit, which are all assimilated to money. It accords with precedents in the Lex mercatoria (merchant law, or the Law Merchant in common legalise). It is the body of trading principles which evolved from the middle-ages along with trade between centres as a system of custom and best practice in Europe.

In this legal respect, money, currency, and credit are different from, say, stolen artworks or precious stones, which on proof of original ownership can be recovered decades later. The families robbed of their possessions by the Nazis over eighty years ago are still reclaiming their property but have no claim on the cash and bank deposits stolen from them.

The position of a CBDC appears to be intended to be different from cash and deposit currency to allow a central bank to control ownership and direct its use, as the quote above from Carstens makes clear. In other words, the right to property in a CBDC differs fundamentally from that of money and currency.

The idea that a CBDC is a legal replacement for cash founders on this important point, which the General Manager of the BIS appears to ignore. Yet the point is proved by commercial bankers in a different context, as evidenced by their inability to deal with payment fraud. If a bank customer finds his bank account emptied by someone who has stolen access to it, it is a criminal act. But the property right to the bank deposit has passed with the stolen money and the bank having had a valid instruction to transfer balances in good faith can do nothing to recover it.

A CBDC does not appear to be a currency in this legal sense, because the right of ownership is subject to conditions imposed by another party — a central bank. In layman’s terms, banknote cash is a document unconditionally entitling the bearer. A unit of a CBDC is not.

Therefore, a CBDC and its derivative forms of credit cannot be currency in law, the term given exclusively to money, credit and their immediate derivatives. Which, incidentally, applies in all post-barter jurisdictions from the time of Aristotle at least.

Not only is this important topic not discussed by the BIS committee working on CBDCs, but no one, to this writer’s knowledge, seems to be aware of a CBDC not qualifying as money or currency in law. It is true that laws may be passed to change the status of a CBDC, but it is equally true that a law may be passed to force everyone to wear a hat. No law can work when its intent is to undermine the whole basis of trade.

In commentaries on the subject, almost everyone has ignored the purpose of a currency which they confuse with money. It represents credit and nothing else. As Carstens points out, cash, by which he means banknotes, is a liability of a central bank. To this we can add bank accounts, which are credit given by a commercial bank to its depositors. And a commercial bank’s reserves held at a central bank are the liability of the central bank with the same status as the central bank’s banknotes.

Almost everyone also ignores the opinions of commercial bankers at the prospect of having their business taken from them by the state and who so far have held their council. We should remember that in America, host to the world’s reserve currency, that the largest contributors to the politicians’ coffers are the banks. That alone should ensure the enabling legislation will never get off the ground in America and therefore for every other major currency which regards the dollar as its reserve currency.

Bitcoin won’t save the Salvadorians

The legal distinction between currencies and CBDCs appears to disqualify cryptocurrencies as well, not only because they are an invention not anticipated in established law. Ownership is firmly tied to a blockchain or similar arrangement which acts as a self-auditing trail. This appears to be an insurmountable hurdle, because to operate as a currency the promoters of any cryptocurrency will have to persuade the authorities in every jurisdiction to pass legislation to give their cryptocurrencies the legal status of currencies.

The current position is that ownership of bitcoin, which we will take as proxy for all cryptocurrencies whose promoters seek to replace state-issued fiat currencies, is theoretically traceable through the blockchain. Under current property law, which in lex mercatoria is common internationally, stolen bitcoin would thus be traceable when held by subsequent owners, either through the blockchain itself or alternatively through the bank payment records when bitcoin pass from seller to buyer. This means that you may acquire bitcoin through a crypto exchange in good faith and not possess the property rights that come with it, if it had previously been the proceeds of crime.

It appears that the only reason property law has not been pursued across the bitcoin blockchain is because of the international character of bitcoin transfers, making it virtually impossible to enforce. Furthermore, access to wallets requires consent which may be withheld. But that does not change the legal position, which is that only money, currencies, and their direct derivatives, even though they have been stolen, pass away “in currency” into the hands of an innocent acquirer, becoming his or her property indisputably in accordance with established lex mercatoria.

Assuming this interpretation is confirmed in law, based on ownership being theoretically traceable the whole foundation of cryptocurrencies as legal tender fails. The authorities are unlikely to accept that it is otherwise for multiple reasons. They have stated their interest in preventing criminal activity, money laundering, and tax evasion and clearly want to confiscate the proceeds of crime when possible. They will also dislike the idea that there is a rival to their fiat currencies, which are protected by currency status in law.

It is in this context that we will consider El Salvador’s adoption of bitcoin as legal tender. Aside from the economic problems that a volatile currency creates and the encouragement for Salvadorians to use a highly volatile ethereal asset as a medium of exchange, there is the problem that by declaring it as legal tender it exposes the population to a currency where ownership in law might not actually exist if it is not classed as currency in other jurisdictions. While not unique to El Salvador, the political class seems to have so little understanding of money and the legalities behind it that we must question the motives behind bitcoin’s adoption.

In May 2021 America withdrew funding from the Salvadorean Government, following a US declaration that five of the President’s ministers and aides were corrupt. The following month the President (Nayib Bukele) announced that he was bringing a bill before the Legislative Assembly to make bitcoin legal tender. Put another way, Bukele appeared to be responding to a dollar shortage created by American sanctions. And early in September Bukele announced that the government had bought 400 bitcoins. The price at the time was approximately $48,000.

The timing of these events strongly suggests that Bukele thought that bitcoin could restore government finances following the withdrawal of US financial support. At the time it was commonly said that the price would eventually rise to over $250,000 with some saying they expected to see it go to over a million. The hype has died down somewhat in a rising interest rate environment, which has also undermined stockmarket prices. Clearly, owners of volatile stocks also own bitcoin, binding the fate of bitcoin to that of stockmarkets.

El Salvador’s launch of a $1 billion bitcoin bond to finance a new coin-shaped bitcoin city, due to have been confirmed earlier this week, has been delayed. Last December, Blockstream (El Salvador’s manager for the bond) announced it had “soft commitments” for up to $300m mostly from “Bitfinex whales”. A soft commitment is not a commitment at all, and the delay of an announcement meant to take place last week does not auger well for the project.

Furthermore, the necessary legislation has not yet been submitted and passed by the Legislative Assembly. The reasons are unknown, but if it is because subscription levels have been disappointing, El Salvador’s bitcoin strategy will begin to unravel. That being the case, the Salvadoran people many of whom do not have internet access will have been saved from an eventual crisis. But the crisis for government finances will intensify.

In propping up government finances Bukele appears to have been a victim of the popular delusions and the madness of crowds seen so many times in history, in this case a cryptocurrency bubble. Arguably, if he understood money and currencies, he might not have fallen for it. In the legal sense cryptocurrencies are not and, citing longstanding law and lex mercatoria precedent, never can be currency. These simple facts are set to doom the whole cryptocurrency movement to an extinction with which historians of financial bubbles will be familiar.

Plans for a new Eurasian and monetary system

For some time, the Eurasian Economic Commission has been discussing the currency aspects of trade between member states. The Commission represents China, Russia, and the former Soviet regions of Central Asia, all of which are members of the Eurasian Economic Union (EEU). According to Sergei Glazyev, the EEU minister in charge of integration and macroeconomics, the objective was to create a Eurasian monetary and financial system, excluding foreign currencies. The proposal was to remove exchange controls for cross-border settlements within the Eurasian membership, and thereby replace the dollar as the commonly used settlement medium between them.

Since then, the project has acquired a new urgency due to western currency sanctions against Russia. According to 24KG, which is a news agency based in Bishkek, only last week the Eurasian Economic Union and China confirmed that they will develop a new international currency (that is international between EEU members and China). The currency and the financial system that goes with it will be based on the national currencies and the prices of exchange-traded commodities. There are no further details other than this statement.

It appears that the intention is to create a sort of SDR but with links to commodity prices and unlike the SDR to be usable at local level. Presumably, the basket of commodities will include oil, and it is interesting that coincidentally Saudi Arabia is considering selling oil for Chinese yuan, calling an end to the petrodollar, and aligning itself more closely to the Eurasian superpowers behind this scheme. Let us put aside the impracticalities of the intended currency for a moment and consider the implications.

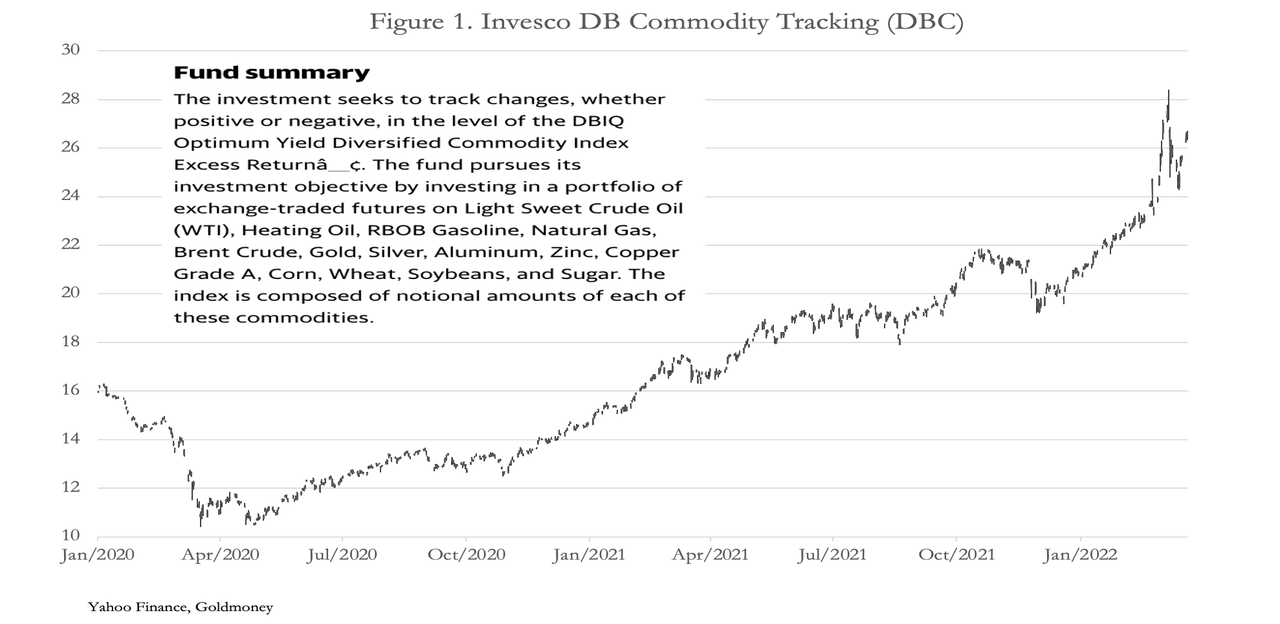

For reference, Figure 1 shows a basket of commodities in a typical ETF, which in dollars has been highly volatile.

{kind=link}

Over the last two years, the basket of commodities represented in this tracker has increased in dollar prices by 160%. Meanwhile, at the same time the price of gold has increased by 33%. There can be no doubt that the common factor is the dollar’s debasement (USD M2 increased by 42%).

Doubtless, the EEU and China will be considering not only which commodities to include and their weightings, presumably in a daily index to be calculated by a central authority. This would then form the basis of bank credit issued by commercial banks authorised to do so. Furthermore, the absence of exchange controls between participating member states will allow businesses and citizens to exchange domestic currencies for the new currency, attracted not just by rising commodity prices, but by relative weaknesses of individual national currencies. That alone will be a tricky issue to deal with, potentially destabilising some national currencies.

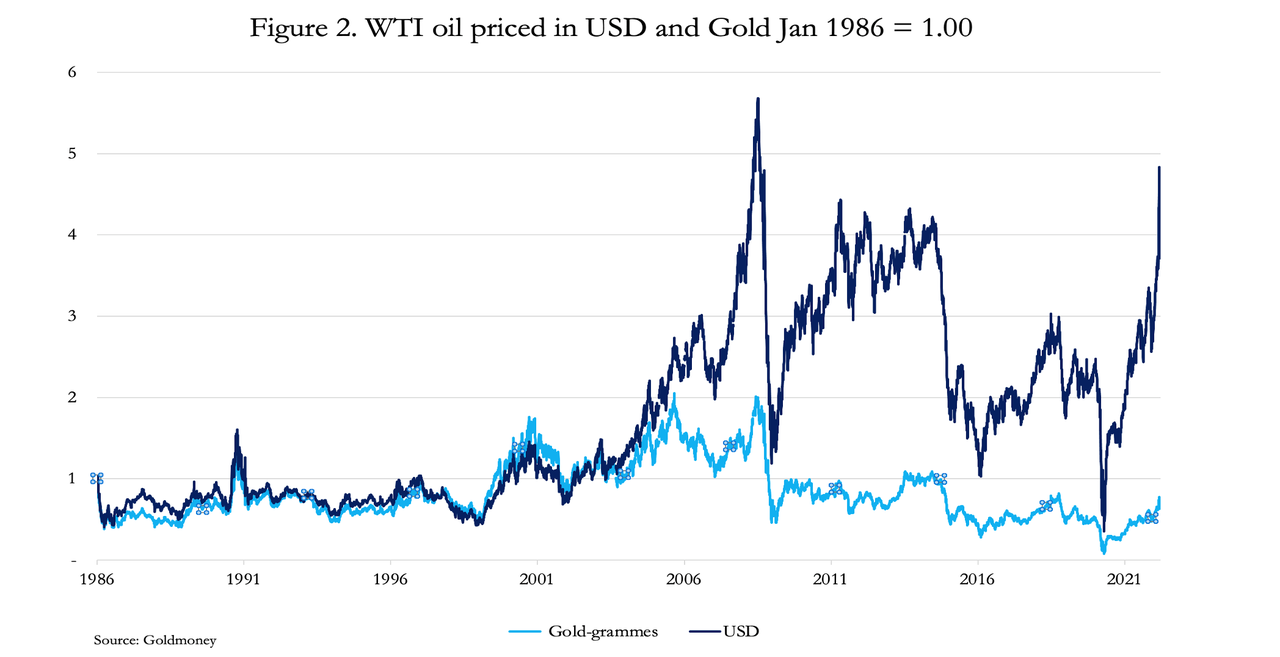

{kind=link}

Figure 2 shows that compared with pricing in dollars, oil priced in gold is considerably more stable, calling into question the concept of indexing a new currency to commodities. There is therefore a prima facie argument that instead of using a basket of currencies it would be better to use gold. For those that understand money, there is no other alternative if the objective is to design a new stable currency to banish the inflating dollar. Using gold offers the following advantages:

Gold is legal money, commodities are not.

Gold is recognised as money throughout the Asian continent. The word for money and gold in Chinese is the same for good reason. A gold-backed currency would have greater public credibility than linking it to a commodity basket.

Throughout the history of fiat currencies commodities have been more volatile than gold.

Virtually all the central banks of the EEU have been accumulating gold in their reserves. They do not possess commodities.

The international legal position of gold as money is clear and opens the possibility of other nations joining the currency scheme in future (like Saudi Arabia?).

We cannot know why the obvious solution is not being considered. The signal emanating from these half-baked ideas is that Glazyev and his team in devising a new currency have a limited understanding of money, currency, and credit.

Whatever the post-classical economic beliefs may be, the extra volatility in commodities compared with gold is undesirable, because as Aristotle said, “With regards to a future exchange (if we want nothing at present, that it may take place when we do want something) money is, as it were, our security”. In other words and in accordance with Say’s law, we require money to be stable and predictable to allow us to plan our business and lives. The economic consequences for domestic economic activity from the unpredictability of a currency’s future purchasing power will only hamper investment in production.

The lesson of history is that the industrial revolution desired by the Chinese in Central Asia is best achieved under a gold coin standard, where the currency is fully exchangeable for coin at the holders’ option. The central banks in the region have sufficient gold reserves to implement such a standard. The Chinese and Russians similarly should abandon the expansion of currency and credit as an economic cure-all in favour of monetary stability. Indeed, if China had introduced sound money and let markets set interest rates rather than the Peoples’ Bank, the level of private sector debt, much of which is unproductive, would not be so high and the current property crisis which is likely to destabilise China’s economy would not have occurred.

Unfortunately, the concept for monetary reform as announced by Glazyev is redolent of being just another statist currency with no real backing. To have a daily fix against the national currencies of the member states without an obligation to deliver anything in lieu is meaningless. And the management of currencies in a “snake” has equally proved to be a failure. It would be far better to start with a new currency operating on a regionally pooled gold coin exchange standard. And by resisting the temptation to incorporate it in a BCDC it would be fully legal.

Anyway, one can imagine that the currency proposed will take several more years in the planning, even though Western sanctions have made the issue urgent.

Conclusion

The debate on currency resets has omitted to address the fundamental legal principles behind money and currencies. They have a unique status in criminal law established over many centuries, embodied in the lex mercatoria. Without this status, no one can accept the right to currency or bank credit safe in the knowledge that it might not be reclaimed as property stolen from a previous owner.

In law this is yet to be tested on central bank digital currencies because they do not yet exist. But cryptocurrencies are already seized by governments when it is suspected they represent the proceeds of or have been used to facilitate a crime. It is acknowledged that bitcoin is not entirely fungible and the law in the US treats it as property and not a currency. The US Asset Forfeiture Policy Manual (2021) states that “most crypto currencies have a blockchain… Using open source or subscription analytical tools, cryptocurrency transactions can be often traced through their blockchains.” In other words, a US resident having purchased it in all innocence can have his cryptocurrency seized.

The problem the authorities have is accessing wallets to recover cryptocurrencies. This is normally targeted at suspected criminals, rather than later down the transaction chain. But the legal distinction of non-currency property seems to be clear, at least so far as the US Department of Justice is concerned: crypto and CBDCs are not currencies exempt from seizure under lex mercatoria.

Attempts at finding alternatives to money, which is only gold and silver coin and bullion, and currency, which is a central bank liability along with bank credit entries, are based on avoiding the discipline of a gold exchange standard. Even bitcoin and other cryptocurrencies have set themselves up as a better medium of exchange, claiming to be in tune with our technological times. Instead, they lack the crucial lex mercatoria exemption and so cannot replace metallic money. Instead, bitcoin and other cryptocurrencies are liable to collapse entirely if metallic money is reintroduced to back existing currencies. To varying degrees, central banks have the gold to back their currencies, but with few exceptions such as El Salvador they do not possess bitcoin and never will.

Meanwhile, the situation for inflating fiat is becoming increasingly precarious. Sanctions against Russia are driving up fuel, commodity, raw material, and food prices, the last of these threatening global starvation in the coming months. More currency will be printed in an attempt to defray the gathering crisis.

Interest rates are beginning to rise as control over them is being taken away from central banks by market forces. Historical precedent is increasingly pointing to a collapse of financial asset values driven by rising interest rates which will take fiat currencies down with them.

Tyler Durden

Sat, 03/26/2022 – 10:30ZeroHedge News