Hedges: The Slow-Motion Execution Of Julian Assange Continues Authored by Chris Hedges via Scheerpost.com, The decision by the High Court...

Read More

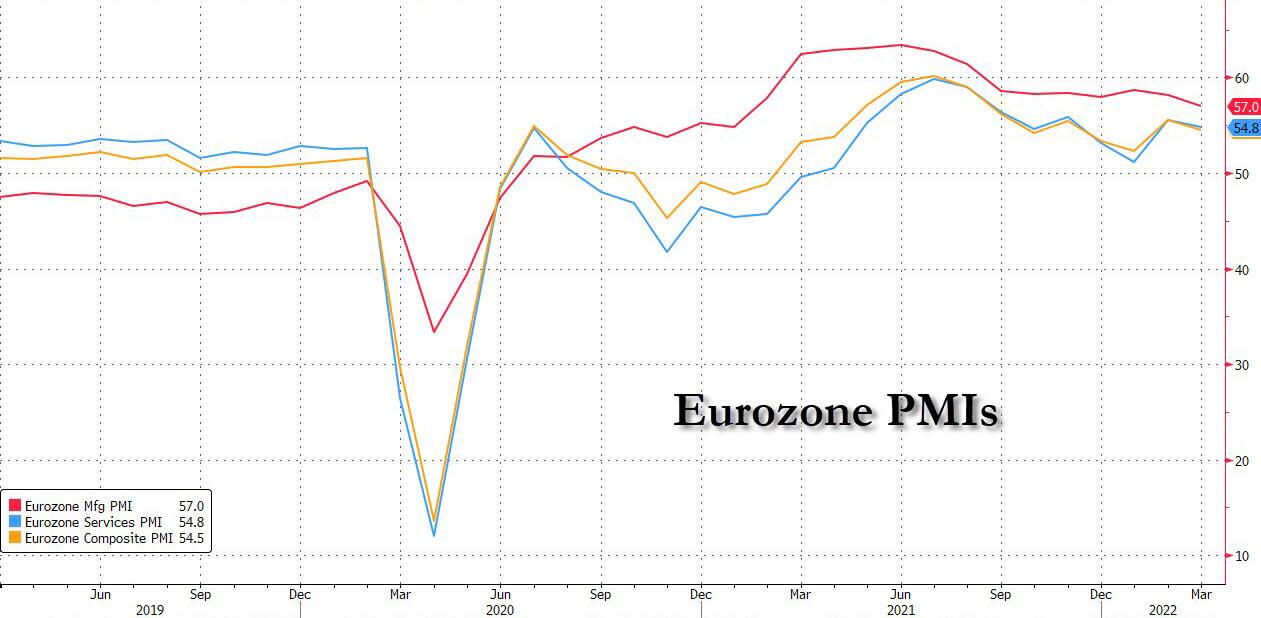

European PMI Data Confirm Ukraine War “Starting To Weigh On Growth”

All eyes were on today’s European PMI reports for confirmation that the Ukraine war has adversely impacted the local economy.

{kind=link}

The Euro area composite flash PMI decreased by 1.0pt to 54.5 in March, above consensus expectations of 53.9, reflecting a moderation in the manufacturing sector but continued strength in services amid further easing of virus-related restrictions. Here are the key numbers (responses were collected between 11 and 22 March)

Euro Area Composite PMI (Mar, Flash): 54.5, GS 53.9, consensus 53.8, last 55.5.

Euro Area Manufacturing PMI (Mar, Flash): 57.0, GS 56.3, consensus 56.0, last 58.2.

Euro Area Services PMI (Mar, Flash): 54.8, GS 54.2, consensus 54.3, last 55.5.

Germany Composite PMI (Mar, Flash): 54.6, GS 53.1, consensus 53.8, last 55.6.

France Composite PMI (Mar, Flash): 56.2, GS 54.6, consensus 54.5, last 55.5.

UK Composite PMI (Mar, Flash): 59.7, GS 58.1, consensus 57.5, last 59.9.

{kind=link}

Looking across countries, the weakening was concentrated in Germany and the periphery, offset partially by an improvement in the French composite. Expectations of future output fell sharply, with the gap between expected future and current output (a measure of pent-up momentum) falling below its historical average.

Unfortunately, a deeper dive in the data indicates that the higher than expected prints may have been propped up by ominous stagflationary trends: as Goldman notes, supply-side issues worsened, especially in Germany, as suppliers’ delivery times lengthened (after having shown signs of improvement since late last year) and price pressures grew further.

{kind=link}

Meanwhile, in the UK, the flash composite PMI moderated only slightly to 59.7, surprising consensus expectations significantly to the upside.

Despite the strength in the spot data, Goldman warns that the slowing in the pace of recovery and the significant weakening in forward-looking components as indicative of the war in Ukraine starting to weigh on European growth momentum. That said, Goldman says it will continue to monitor incoming evidence, including high-frequency data and the upcoming business surveys, to gauge the growth implications from the ongoing conflict.

Here is some more detail from the report:

The Euro area composite PMI decreased by 1.0pt to 54.5 in March, above consensus expectations. Across countries, the weakening was concentrated in Germany and the periphery, offset partially by an improvement in the French composite. The area-wide composite decline reflected broad-based weakening across sectors, but skewed towards manufacturing. The composition of the March report showed a slight improvement in employment but a decline in backlogs and new orders, with new export orders in particular falling below 50 into contractionary territory. Firms’ expectations fell sharply to their lowest level since October 2020, with the gap between expected future and current output (a measure of pent-up momentum) falling by over 3 standard deviations in March to below its historical average. Suppliers’ delivery times, which had remained long but showed signs of improvement since October last year, worsened in March and price pressures grew further, with both input and output prices reaching new all-time highs.

The German composite PMI decreased by 1.0pt to 54.6 in March, above consensus expectations. The decline was broad-based across sectors but skewed slightly towards manufacturing. The composition of the March report was squarely weaker than in February, with new orders, employment, and backlogs of work, all moderating slightly. Firms’ year-ahead output expectations posted the largest decline since the start of the pandemic and fell to their lowest level since June 2020. Suppliers’ delivery times—which were already long compared with historical standards—also recorded the largest worsening since the pandemic hit after having improved for the last 4 successive months. And price pressures grew further, with both input and output prices reaching new all-time highs.

The French composite PMI increased by 0.7pt to 56.2 in March, well ahead of consensus expectations for a moderate decline. The overall gain was driven solely by a further improvement in the services PMI, which is now at its highest level since November, while manufacturing output declined by 4pt to 51.0. Expectations of year-ahead output dropped meaningfully (albeit to a lesser extent than in Germany) to just below the historical average and suppliers’ delivery times—which had shown some signs of improvement since October last year—worsened slightly in March. Price pressures remain acute, with both input and output price components increasing to new all-time highs.

The UK composite PMI decreased by only 0.2ptsto 59.7 in March, surprising consensus expectations (at 57.5) significantly to the upside. The composite decline was entirely manufacturing-led, while the services PMI increased further in March to 61.0, nearing the all-time highs observed last summer. The composition of the March report was somewhat mixed—with higher employment but lower new orders and backlogs of work. Expectations of year-ahead output decreased but remain above the historical average and unlike in the Euro area, suppliers’ delivery times continued to improve in March (but they remain long still). On price pressures, both input and output prices edged up further on the back of broad-based upward price pressures across sectors.

Summarizing the first post-war PMI report, the data were directionally in line with expectations, the magnitude of the deceleration in the spot data was smaller than we had anticipated, reflecting continued growth in the services sector – and a notable surge in Prices – amid further easing of virus-related restrictions. That said, the slowing in the pace of recovery, especially in the manufacturing sector, and the significant weakening in forward-looking components (except in the UK where the weakening has been more limited), suggest that the war in Ukraine is starting to weigh on European growth momentum. We will continue to monitor incoming evidence, including high-frequency data and the upcoming business surveys, to gauge the growth implications from the ongoing conflict.

Tyler Durden

Thu, 03/24/2022 – 11:45

Recent Comments