42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Goldman: “Too Furious Ferrous Rally”

China’s recent monetary and fiscal bazooka will likely fall short of the policy prescription needed to rid the world’s second-largest economy of deflationary risks. The real estate crisis remains unresolved, and iron ore markets are trending lower after a brief spike in late September when Beijing initially announced stimulus.

Just as the iron ore rally was blasting off, Goldman’s Thomas Evans told clients around Sept. 24 to “fade iron ore rallies.”

“In the long term, steel overcapacity and growing supply in iron ore are the two biggest headwinds to ferrous supply chain, which can’t be fixed any time soon. The indicator to watch is whether, when and how much iron ore production would be cut from junior miners for market to rebalance,” Evans said, adding the market cannot rebalance “until steel capacities are shut down and junior iron ore miners cut production.”

Between Sept. 24 and Oct. 7, iron ore jumped nearly 28% from $89 a ton to $114. By Oct. 8, prices plunged from about $114 to $105 on news that China’s National Development and Reform Commission did not deliver enough stimulus the market hoped for.

{kind=link}

We noted:

Now, with iron ore prices slipping under the $100 a ton level on Friday, Goldman’s Aurelia Waltham, Daan Struyven, and Samantha Dart expect prices to fall back to around $90 amid a much-needed rebalance as port supplies remain elevated:

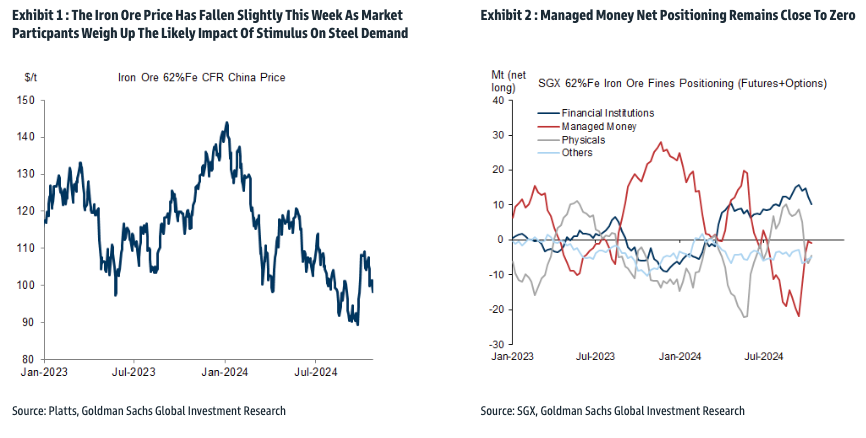

Iron ore prices have retreated this week, with the 62%Fe index at $99/t today (Oct. 24), down 2% from last Friday. While the price drop appears to stand in contrast to the ongoing rise in consumption, in our view it reflects the broader oversupply in the iron ore market. Specifically, Chinese port stocks remain 40% higher than this time last year, driven by elevated arrivals. With surging shipments from India and Australian volumes in recovery, we expect port stocks to rise further unless prices drop below $90/t, which would remove Indian supply from the market, and allow fundamentals to start rebalancing.We also highlight that, with the market continuing to assess the impact of stimulus on demand, there is the risk of steel prices reversing the gains made since the end of September if stimulus disappoints. This could renew the pressure on steelmakers’ margins and result in hot metal output cuts.

In a separate note, Goldman’s Gerald Tan called the price moves in iron ore: “Too furious ferrous rally.”

{kind=link}

Tan continued:

The roughly 20% rally in iron ore prices following stimulus looks excessive relative to our estimate of a fundamental boost of up to 7%. The significant elasticity of supply around current price levels explains this muted fundamental boost, which may be even smaller in practice given the policy focus on inventory destocking instead of starts. We thus reiterate our view that iron ore prices need to fall below $90/t to rebalance fundamentals.

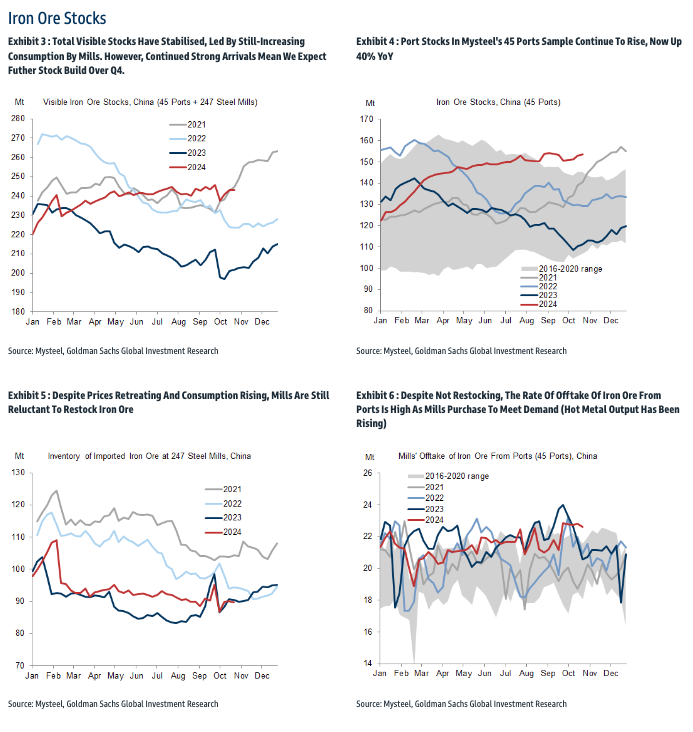

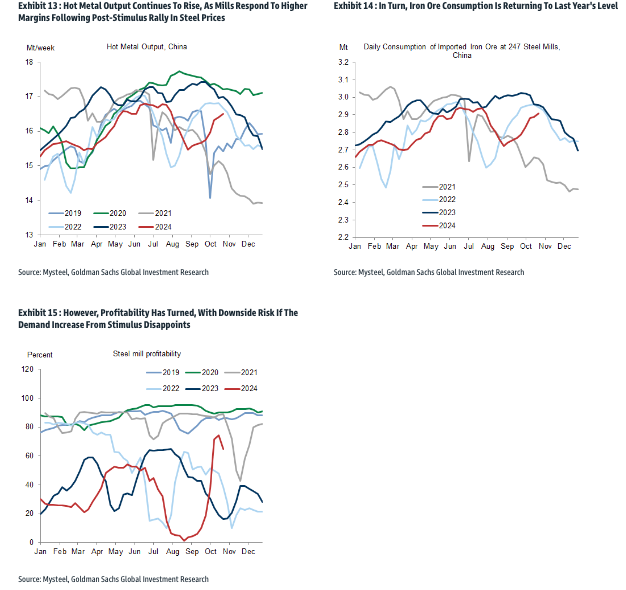

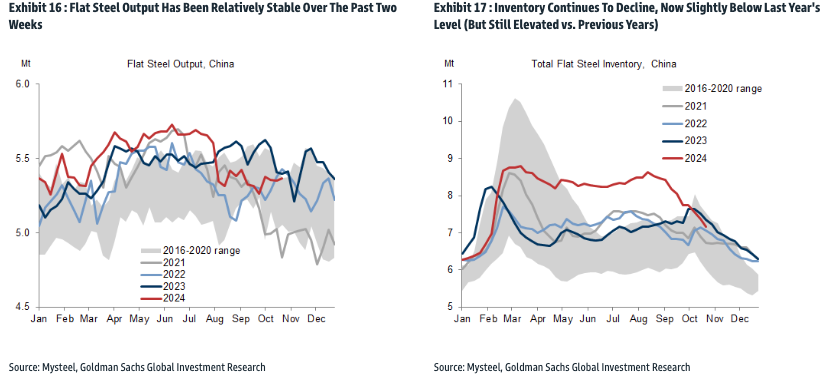

Back to Waltham’s note, the analysts provided clients with a chart pack that clearly shows oversupplied conditions:

Prices

{kind=link}

Fundamentals

{kind=link}

Supply

{kind=link}

Consumption

{kind=link}

Finished Steel

{kind=link}

So far, Goldman has nailed the rollercoaster price action in iron ore futures. Lower for longer appears to be the key move for proper rebalancing.

Tyler Durden

Fri, 10/25/2024 – 09:10