42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

When Things Kinda Make Sense

By Peter Tchir of Academy Securities

When Things Kinda Make Sense

I’m a contrarian by nature. I much prefer finding things that markets may be pricing incorrectly, to going along with the consensus. Usually there is no shortage of topics to pick from as a contrarian. Anything from China, to the quality of data, to the economy, to geopolitical risk, to valuations, but right now, I’m struggling to find an issue to get worked up about. Maybe this is the exception that proves the rule?

In any case, let’s run through a variety of issues that, for better or worse, I think kind of make sense from a market pricing standpoint.

Interest Rates

For the first time in recent memory, I think rates are, more or less, priced correctly. As discussed last week in Little New to Say, it was getting more difficult to remain bearish on Treasury yields, though the bull case was even less convincing. The 10-year did eventually rally back to 4% on Wednesday, but then gave up most of those gains, and is stuck right around 4.1% again.

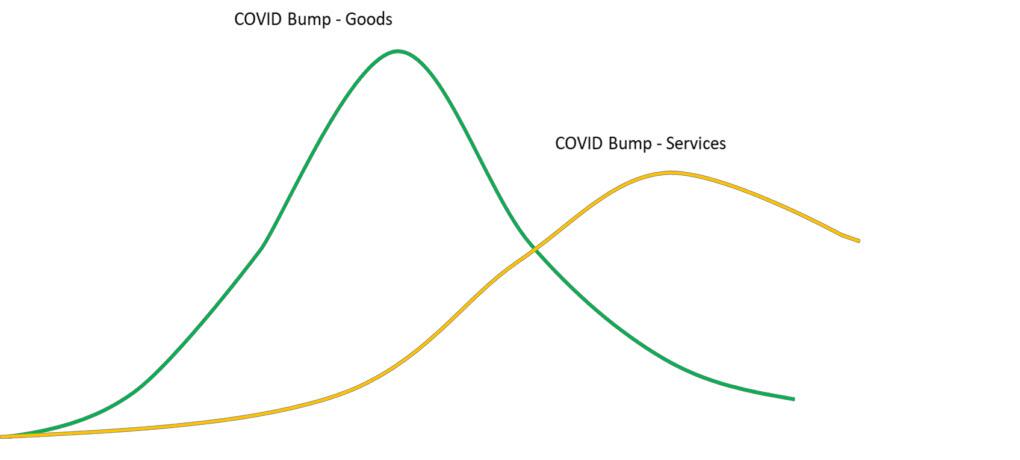

We’ve argued in that report and in War, Inflation, and the Neutral Rate, that we might have seen a temporary bottom for inflation. The disruptions caused by hurricanes Helene and Milton could prove inflationary. The rebuilding efforts, which will begin in earnest as insurance checks hit, will also be inflationary. Again, I’m not alarmed that we will get a surge in inflation, but the easy part of the lower inflation story is almost over (the “simple” model of two distinct “Covid bumps” – one for goods and one for services – has been an effective tool in estimating the direction of inflation). You can find the “Covid bump” chart in Building the Case For Rate Cuts from early July.

{kind=link}

The Neutral Rate has become a part of virtually every bit of FedSpeak that we get. Almost all speakers agree that it is higher than they previously thought. So far, they seem to be channeling 3% to 3.5%, but I expect that to solidify to 3.5% to 3.75% sooner than later. We spent over a year over 5% and the economy has barely slowed!

Having said all that, markets have largely moved to be in line with our take. They are still a bit more aggressive on the rate cut front than we are, and we think they are too complacent on the deficit and the longer end of the yield curve, but market rates are in our ballpark now.

On the Fed cut front:

The market is pricing in 2.5 cuts in the next 3 meetings.

That isn’t far from our expectations. As discussed on Bloomberg TV last week, we are still pricing in 25 bps in November as a certainty. Bloomberg TV captioned our recent interview as Embarrassing for the Fed Not to Cut in November. The caption is a bit aggressive (it was 5:30 in the morning after all, and we covered a lot more ground), but I do think that for the sake of continuity and to support the decision to go 50 in September, they will cut 25 unless we get some extremely strong data. Then, I would expect a pause in one or both of the next 2 meetings. Our base case is only 2 cuts in the next 3 meetings, which means the market is “only” 0.5 cuts higher than us (the markets were 2 full cuts more than us a couple of weeks ago).

Our current outlook for next 3 meetings:

50% chance of 25, 0, 25

30% chance of 25, 25, 0

20% chance of 25, 0, 0

The market doesn’t get below 3.3% on Fed funds until January 2026. That is a far cry from when it was below 3% by the summer of 2025 a few weeks ago. I think that it continue to inch up towards 3.6%, but my timing for that is early 2026. We are basically down to arguing over just about 1 cut, instead of 3, which is where we were. Again, all kinda makes sense.

That still leaves me slightly bearish 10s, primarily because I think 2s vs 10s should be 25 bps (though they closed at 13, which fits that “kinda right” vibe of today’s report). Also, I just see many more scenarios where we get another “buyer strike” as the realization that no one in D.C. is incentivized to control the growth of the deficit, rather than scenarios that see a surge in demand. For a range on 10s, I think 4% to 4.2%, but with more risk of a breakout to 4.5% than a breakdown to 3.75%. The 30-year is even more susceptible to a major move to higher yields from Friday’s 4.4% close (5% seems unlikely, but is a risk).

Jobs and the Economy

Following my view that seasonal adjustments have been wrong (adding too many jobs in the winter and subtracting too many jobs during the summer), we should be getting “clean” data. In fact, errors and issues surrounding jobs data have retreated from front and center for us, to more of a back burner issue. But, while issues addressed in The Fog of War have not been entirely resolved, they just aren’t our highest priority right now.

While the hurricanes will cause some distortions, I expect the jobs data to be “okay.” Consistent with a bumpy/choppy landing – not signifying growth, but also not hinting that we might already be in a recession.

Consumer data seems “mixed.” There are signs that spending remains robust, like this week’s retail sales data. There are also some signs that consumers, especially lower income ones, are getting stretched. Credit card debt, even adjusted for inflation (and wage growth), is getting to be a potential hurdle to further spending. We are seeing delinquencies (most noticeably in autos) tick higher. Regardless of which data you look at on this front, the trend has not been friendly. On the other hand, some metrics are still below 2018/2019 averages, so it shouldn’t signal panic, just something to watch.

At the same time, some portion of that record amount of money in money market funds is held by individuals. Presumably, some of that interest gets spent, helping the economy. I think the surprise in this cycle will be that lower yields stall spending as most debts are locked in at lower yields and the lack of interest income will hurt households more than the cuts help (ok, I managed to squeeze in one “out there” view in today’s report).

The Atlanta GDPNow estimate is at 3.43%! That is up from a recent low of 2.54% on October 1st. This number is a bit volatile, but even 3% would indicate a decent, even good economic backdrop, which I cannot disagree with.

Our “bumpy” scenario is that some sectors will be doing well, while others struggle. Ditto for various regions of the country. Nothing that the economy can’t handle, but also not some overly rosy resurgence story.

Earnings and Market Responses

Taiwan Semiconductor announced earnings that helped that stock jump 10% on Thursday. The chip stocks did well, but not as well as TSM, and the Nasdaq 100 edged only marginally higher. To me, the response seemed kinda right. The epicenter of the move was on the stock that delivered the positive outlook, and the strength rippled out from there, but in what seemed appropriately proportional amounts. It didn’t cause the entire market to go into a furor of buying. Similarly, NFLX did extremely well on Friday (up 11%), but it seemed to be treated, correctly in my opinion, as a validation of their business, rather than some sign that all tech should rally! Yes, markets did rally on Friday, in part because of NFLX, but I think it had more to do with another effort by China to further talk up their markets and their commitment to stimulus. ARKK, which I still use as a barometer for “disruption,” was actually down on Thursday, again signaling “differentiation” rather than excessive speculation in the market.

Breadth seems to be increasing as the Russell 2000 outperformed the other major indices and the equal weighted S&P 500 beat out the regular S&P 500 on the week (barely, but still, a positive sign for breadth).

The fact that major companies, with large market caps, can move 10% on earnings, still seems a bit bizarre to me, but I like how the rest of the market performed around these earnings. It is as though we’ve built up a base and are being thoughtful, rather than just slapping the “BUY” button.

I’m sticking to my assessment that the CCP needs the economy to turn around and will continue to add measures to prop it up (see China Stimulus Simplified). So far, they seem to be following our playbook as though they read the T-Report. One thing I do think the market is getting wrong, is assuming the Chinese stimulus will help the big global companies, when I believe it will be as targeted as possible to support domestic brands, as part of the transition from Made in China to Made by China.

I’m still concerned about valuations in some areas and think there is a big risk if we see any signs that spending on AI is slowing or even being questioned. It is just as easy (or maybe easier) to have 10% down days. In general, I do think the market behaved rationally relative to the news flow recently.

Finally, from a purely “Market Structure” standpoint, we continue to have the risk that a lack of liquidity can cause larger-than-rational moves in either direction, where the chance of very large single day moves to the downside heavily outweigh the odds of a big day to the upside.

Credit Markets

Remember when we asked How Tight Can Credit Spreads Go? Well, the market continues, maybe begrudgingly, to move in our direction. We listed multiple reasons to remain so bullish credit. We have reiterated some in recent reports, but I urge you to go back to this report from July to see the entire list, since the reasons are all still in play.

{kind=link}

The Election

If saying credit spreads, already tight, are likely to go tighter, isn’t treading into dangerous waters, then bringing up the election certainly is.

Gridlock. That seems to be the one thing markets and most polls agree on. Most things I see point to a House of Representatives won by the Democrats and a Senate won by the Republicans. So long as that seems to be the base case, then it doesn’t matter as much who wins the presidency, as their ability to create real change will be limited. It also fits with a view (which I hold) that people who vote against someone (rather than voting for someone) are more likely to split their ticket. They want to vote against someone, but don’t want to give, whoever they vote for, too much power.

We are starting to spend time thinking more seriously about potential outcomes and policies and expect to publish early this week on the subject, but for now, we think the markets are moving in regard to election headlines.

Geopolitics

Academy’s Geopolitical Intelligence Group published a SITREP on Israel Kills Sinwar. There are ongoing developments this weekend and we continue to expect Israel to retaliate against Iran directly. While the death of Sinwar may open the door to some truce with Hamas, that is far from certain. In any case, Israel is likely to continue to prosecute their war with Iran’s other proxies and Iran itself.

The markets seem entirely focused on whether or not Israel (or Iran) will do anything to disrupt the flow of oil. So long as that seems to be off the table (which was the indication that we were given this past week), markets will not pay too much attention to the situation. Yes, participants in markets are paying close attention to all of the suffering and death, but that does not translate into markets moving, unless we get significantly more escalation and expansion (even then, the reaction in markets is likely to be muted unless energy supplies are affected). It seems harsh to write this (and it probably is), but there is a significant difference between human tragedies and what can move markets.

Owning energy (rather than Treasuries) is the best way to hedge any escalation. Though at 4.1%, it is less unreasonable to own some Treasuries as a hedge to geopolitical risk (though I don’t think it will be as successful as owning energy).

Bottom Line

Rates, call it slightly bearish, but just barely (low conviction and small sizes).

Credit, still dull and still a great place to be.

Equities, Chinese stocks, value, small caps, and equal weight indices all look attractive. Still too worried to fully commit to the stocks with the highest valuations/multiples/best moments, but I did like how the market behaved (though I’d add to the laggards rather than to the year-to-date winners). Finally, things seem to be falling into place for commercial real estate bets. I would have liked to see a lot more “clearing transactions” where we developed a true clearing price as I’m told there still is a difference between what buyers are willing to pay and what sellers think they deserve. But everything from the end of rate hikes to more “Work From Office” headlines, makes me want to add exposure here.

Tyler Durden

Sun, 10/20/2024 – 14:00