42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

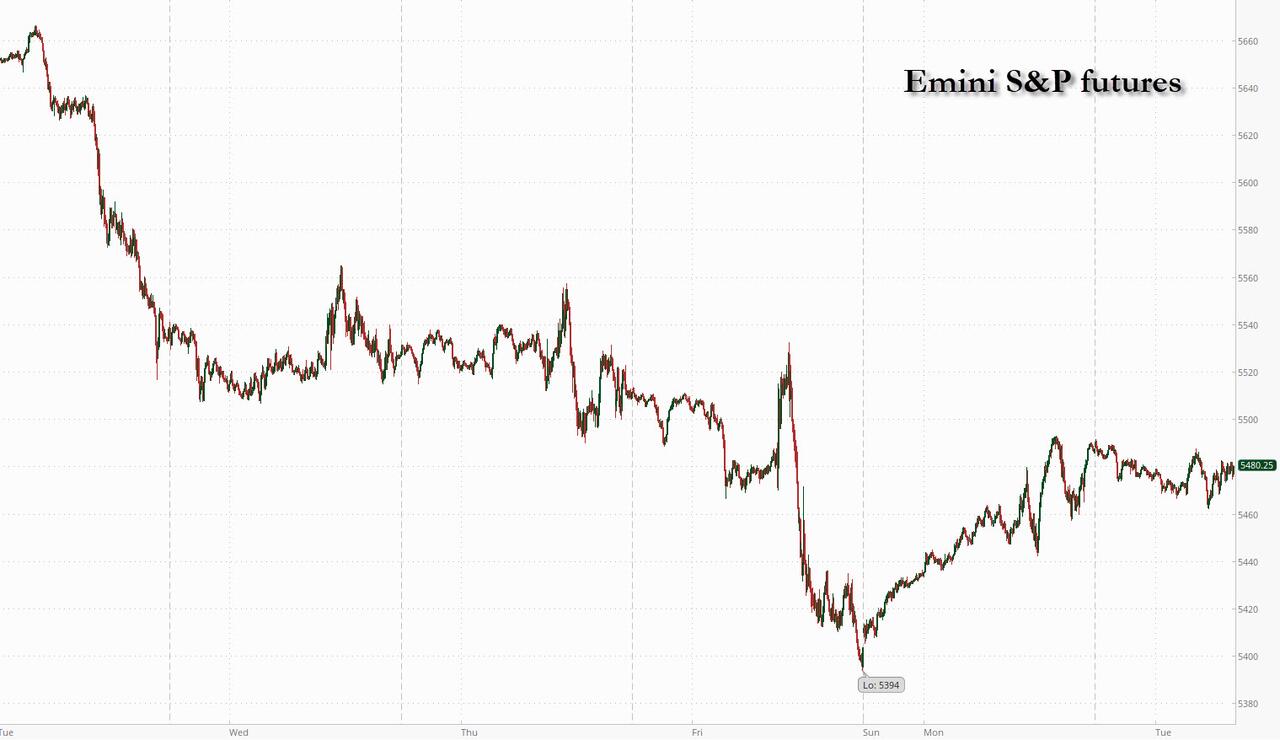

Futures Rise Ahead Of Trump-Harris Debate

US equity futures rose, trading near session highs after they rebounding off overnight lows as markets head into a crunch period, with key inflation data on Wednesday followed by the Fed’s interest-rate decision next week. As of 8:00am ET, S&P futures were up 0.1% trading in a narrow range after the underlying gauge rose 1.2% on Monday, rebounding from its worst start to the month in data going back to 1953; Nasdaq futures were down 0.2% as Mag7 and Semis are weaker while Financials rise following a Bloomberg report of lower capital requirements. Treasury yields rose a second day, higher by 1-2 bps while the USD held Monday’s gains. Commodities are mixed with metals up, energy down, and Ags mixed. The macro data in focus is on the Small Biz Optimism print (which dropped to 91.2 from 93.7, missing estimates) and the Presidential Debate.

{kind=link}

In premarket trading, Oracle jumped 8% after reporting quarterly profit and bookings that topped estimates, signaling that artificial intelligence demand continues to boost its cloud computing business. Apple shares slid 1% after the iPhone maker lost its court fight over a $14.4 billion Irish tax bill. Here are some other notable premarket movers:

Mission Produce jumps 22% after the avocado supplier reported fiscal third-quarter revenue that topped the average of two analyst estimates compiled by Bloomberg.

Rubrik drops 6% after the cybersecurity company reported earnings; Bloomberg Intelligence notes that doubts about growth in the second half of the year could linger.

Viridian Therapeutics gains 8% ahead of a conference call this morning when the company will report topline data for the Thrive phase 3 clinical trial evaluating VRDN-001 in patients with active thyroid eye disease.

As Bloomberg notes, the market mood has been cautious as investors look to balance US recession fears and the likelihood of a soft landing, amid worries the Fed may be falling behind the curve as the labor market cools. Meanwhile, US political risk is back at the forefront, with former President Donald Trump squaring off in a debate with US Vice President Kamala Harris later Tuesday. Meanwhile, according to Nate Silver, Trump’s chance of winning just hit 64.4%, the highest yet.

#Latest @NateSilver538 Forecast (9/9)

🟥 Trump: 64.4% (new high)

🟦 Harris: 35.3%

——

Swing States: chance of winning

Pennsylvania – 🔴 Trump 65-35%

Michigan – 🔴 Trump 55-45%

Wisconsin – 🔴 Trump 53-47%

Arizona – 🔴 Trump 77-23%

North Carolina – 🔴 Trump 76-24%

Georgia – 🔴… pic.twitter.com/Cw23W9WmSK

— InteractivePolls (@IAPolls2022) September 9, 2024

“We need to see what actually plays out and will have the possibility of impacting markets,” Grace Peters, global head of investment strategy at JPMorgan Private Bank, said on Bloomberg TV. “We will be watching tariffs, trade policy, taxes.”

Amid the rising uncertainty hedge funds have been unwinding their positions to get cash ready for volatility ahead of the Nov. 5 vote, according to Goldman Prime Brokerage data. At Newton Investment Management, head of fixed income Ella Hoxha is avoiding assets exposed to “a weaker cyclical backdrop, potentially wider credit spreads and weaker commodity currencies,” she said in an interview with Bloomberg TV. Since Friday, the firm has been boosting safe assets including US Treasury and Japanese government debt, she said.

European stocks declined but still traded within Monday’s levels. Heath care, autos and energy are the worst-performing sectors in Europe’s Stoxx 600 while the commodity-heavy FTSE 100 lags regional peers with a 0.6% drop. The ECB’s policy meeting later in the week is also weighing on risk appetite. The central bank meets Thursday, where it is expected to deliver a second interest rate cut this year to tackle a faltering economy.

Earlier, Asian stocks were also mixed as a reversal of early losses in China offset declines in Japan and Korea. The MSCI Asia Pacific Index traded in a tight range, with health-care firms among the biggest drags. Japan’s Topix reversed earlier gains to drop for a fifth day as the strong yen weighed on investor sentiment. Chinese stocks rose in late trading, closing slightly higher, though the CSI 300 Index is still hovering near its lowest close since January 2019. Latest data releases have added to worries over spiraling deflation in Asia’s largest economy, while the progress in US legislation that would blacklist some Chinese biotech firms adds to headwinds for the nation’s equities.

In FX, the Bloomberg dollar spot index inches marginally higher ahead of the Trump-Harris presidential debate. Pound steady at $1.30 after UK pay growth cooled to a two-year low in the three months through July. JPY underperforms G-10 FX after a Bloomberg report said that Bank of Japan officials see little need to raise the benchmark rate when board members gather next week. Morgan Stanley sees the euro sliding toward parity with the dollar within months amid risks of aggressive ECB policy easing. The US bank expects the single currency to slump to $1.02 by year-end, a roughly 7% depreciation from its current level of $1.1037. The call is the most bearish among currency analysts surveyed by Bloomberg.

In rates, treasuries are slightly cheaper across the curve amid comparable losses for bunds and gilts following several European bond sales skewed toward longer-dated maturities. Yields are higher by 1bp-2bp across the curve, the 10-year around 3.715% and slightly cheaper vs bunds and gilts in the sector, with curve spreads little changed. Coupon auction cycle begins at 1pm New York time with $58b 3-year new issue, followed by $39b 10-year and $22b 30-year reopenings Wednesday and Thursday. WI 3-year yield at around 3.515% is ~29.5bp richer than last month’s, which stopped through by 0.2bp following a selloff. Calendar events are limited ahead of the presidential debate slated to start at 9pm New York time.

In commodities, Brent crude underperforms commodities with a 1.2% drop to near $71 a barrel. Spot gold falls roughly $5 to trade near $2,502/oz.

Bitcoin continues to edge higher, now sitting above USD 57k whilst Ethereum holds around USD 2.3k.

Looking to the day ahead now, the main highlights will be the TV debate tonight between Kamala Harris and Donald Trump. Otherwise, data releases include UK unemployment and Italian industrial production for July, whilst in the US there’s the NFIB’s small business optimism index for August. Finally from central banks, we’ll hear from Fed Vice Chair for Supervision Barr.

Market Snapshot

S&P 500 futures little changed at 5,481.75

STOXX Europe 600 up 0.2% to 511.94

MXAP down 0.2% to 179.60

MXAPJ up 0.1% to 558.71

Nikkei down 0.2% to 36,159.16

Topix down 0.1% to 2,576.54

Hang Seng Index up 0.2% to 17,234.09

Shanghai Composite up 0.3% to 2,744.19

Sensex up 0.7% to 82,145.49

Australia S&P/ASX 200 up 0.3% to 8,011.94

Kospi down 0.5% to 2,523.43

German 10Y yield little changed at 2.18%

Euro little changed at $1.1035

Brent Futures down 0.4% to $71.58/bbl

Gold spot down 0.2% to $2,501.26

US Dollar Index up 0.13% to 101.69

Top overnight news

Largest US banks’ capital hike was reduced in half under the latest plan by regulators in which banks would face a 9% increase in capital requirements instead of the 19% that was originally called for by the Fed, FDIC and the Office of the Comptroller of the Currency: BBG

China’s exports come in ahead of expectations for Aug (+8.7% vs. the Street +6.6%) as companies seek out int’l markets amid soft domestic demand while imports fell short (+0.5% vs. the Street +2.5%). RTRS

A deepening selloff in Chinese stocks is exacerbating a crisis of confidence in the world’s second-largest economy, heaping pressure on policymakers to halt the downward spiral. BBG

China urged by economists to enact a ~$1.4T stimulus plan amid dire economic trends, including intensifying disinflationary pressures. FT

BOJ officials see “little need” to hike rates at their meeting next week (Bloomberg); UK wage growth eased to +4% in Jul (vs. +4.6% in June), keeping the BOE on a path to continue easing policy (although rates are expected to stay unchanged at next week’s meeting). BBG

Norway’s underlying inflation continued to ease in Aug (but was inline w/expectations), bolstering expectations for the country’s central bank to cut rates this year. BBG

Apple and Google lost landmark EU decisions in a win for the bloc’s crackdown on tech companies. Apple was fighting a €13 billion Irish tax bill, while Google had sought to topple a €2.4 billion antitrust fine. BBG

US regulators scaled back a proposed capital requirement hike for the biggest banks, to 9% from 19%, people familiar said. The move will probably appease banks and may also help Fed Chair Jerome Powell gain support from the central bank’s board. BBG

Apollo and other PE firms are muscling into the $15 trillion US life insurance and retirement savings market, shaking up traditional insurers as they push back with regulators caught in the middle. BBG

Tonight’s debate between Kamala Harris and Donald Trump has unnerved investors more than before the June event with Joe Biden. A measure of dollar volatility is near the highest since 2023 and the VIX is on the upswing. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly took impetus from the gains on Wall St where the major indices rebounded amid light newsflow ahead of looming key events, although Chinese markets lagged amid mixed Chinese trade data. ASX 200 was led higher by strength in financials and utilities but with gains capped after weak consumer and business surveys. Nikkei 225 edged higher albeit with trade contained in the absence of any major pertinent catalysts. Hang Seng and Shanghai Comp were mixed as the former was indecisive with Alibaba the biggest gainer after its Stock Connect inclusion, while WuXi AppTec was at the other end of the spectrum after the US House passed the Biosecure Act which would prohibit the US government from contracting with certain biotech firms. Conversely, the mainland lagged behind regional peers amid mixed Chinese trade data and after protectionist measures by the US House which also voted to pass the Countering CCP Drones Act that would bar new drones by DJI from operating in the US.

Top Asian News

BoJ reportedly sees little need to hike interest rate next week, according to Bloomberg sources; officials are not ruling out another hike later this year or in early 2025 contingent on the economy and market.

US House passed the Biosecure Act with broad bipartisan support which would prohibit the US government from contracting with, or providing grants to, companies that do business with a “biotechnology company of concern”, while it specifically named five Chinese companies which were BGI Genomics, MGI Tech, Complete Genomics, WuXi AppTec, and Wuxi Biologics.

US House voted to bar new drones from Chinese drone maker DJI from operating in the US, according to Reuters.

TSMC (2330 TW/TSM) August (TWD) Revenue 250.87bln, -2.4% M/M

Chinese August vehicles sales -5% Y/Y (prev. -5.2% in July), Jan-Aug vehicles sales +3% Y/Y (prev. +8% a year ago); NEV sales +30% Y/Y.

China’s Vice Commerce Minister said China is willing to engage in dialog and consultations to appropriately resolve China-EU economic and trade frictions

European equities, Stoxx 600 (+0.3%) began the session flat/mixed but quickly turned positive as sentiment improved since the cash open. Since, sentiment has deteriorated and indices now sit towards the bottom end of today’s ranges. European sectors are mixed; Real Estate takes the top spot, with Tech also on a firmer footing. Healthcare is the clear underperformer, dragged down by AstraZeneca (-5%) after its lung cancer drug trial failed to significantly improve survival. US equity futures (ES -0.2%, NQ -0.2%, RTY -0.2%) are entirely in the red, paring some of the gains made in the prior session; the NQ marginally lags, hampered by Apple (-1% pre-market), after a EU tax order. EU to lower proposed tariffs on Tesla’s (TSLA) and other EVs from China. Tesla’s tariff rate reportedly to fall to under 8% from 9%, according to Bloomberg sources. Apple (AAPL) has lost fight against EUR 13bln EU tax order to Ireland, according to Reuters; Apple said EU regulators are trying retroactively to change the rules. EU top court dismissed Alphabet’s (GOOG) fight EUR 2.42bln EU antitrust fine.

Top European News

Kantar: UK Grocery inflation 1.7% (prev. 1.8%), UK Grocery sales +3% in value terms in the 4 weeks to Sep 1st Y/Y.

Germany’s Chemical Industry Association VCI said Q2 production +3.7% Y/Y, or +8.4% without pharmaceuticals.

FX

DXY has paused for breath after a two-session winning streak which has taken the index from a 100.58 base on Friday to a current session high at 101.72. Data docket for the remainder of the day is light so the next risk event for the USD comes via the Presidential debate overnight.

EUR is steady vs. the USD with EUR-specific drivers light in the run up to Thursday’s ECB decision which ultimately may prove to be an event lacking in volatility. If the pair’s recent downtrend resumes, support comes via the 3rd September low at 1.1026.

GBP is the marginal outperformer across the majors post-UK jobs data which showed a decline in the unemployment rate and a sharp jump in employment. For cable, the pair has moved back above its 21DMA at 1.3080 but failed to sustain a move above 1.31 after topping out at 1.3107.

JPY is on the backfoot vs. the USD in an extension of yesterday’s price action. For now, the pair has been unable to top yesterday’s best at 143.80.

Antipodeans are steady for both of the antipodes vs. the USD. AUD is a touch softer post disappointing confidence data which overshadowed broadly encouraging Chinese trade metrics. AUD/USD is back below its 100DMA at 0.6646.

PBoC set USD/CNY mid-point at 7.1136 vs exp. 7.1140 (prev. 7.0989).

Fixed Income

USTs have pulled back a touch in-fitting with some of the downside seen in European peers. Tonight’s US Presidential debate could offer some impetus, whereby a strong showing from Trump could reignite some of the bear-steepening bets seen post-his debate with Biden in the summer; US2s10s is still in positive territory whilst the 10yr yield is currently sitting within yesterday’s 3.691-763% range.

Bunds are a touch softer in a move which coincided with UK jobs data. Fresh macro drivers for the Eurozone are light in the run up to Thursday’s ECB decision which ultimately may prove to be an event lacking in volatility. German 10yr yield is back below the 2.2% mark at 2.178%.

Gilts are slightly lower, in-fitting with European peers. The main macro update from the UK has come via labour market/earnings data which saw a downtick in unemployment, jump in employment change and slightly softer earnings components. UK 10yr yield is currently contained within yesterday’s 3.856-944% range.

Orders for Italy’s new BTP are over EUR 108bln, spread set at 13bps over 2053 BTP, according to Reuters.

UK sells GBP 900mln 0.625% 2045 I/L Gilt: b/c 3.44x (prev. 3.88x) & real yield 1.20% (prev. 1.304%).

Germany sells EUR 0.462bln vs exp. EUR 0.5bln 2.10% 2029 Green Bobl and EUR 0.485bln vs exp. EUR 0.5bln 0.00% 2050 Green Bund.

Commodities

Crude is on the backfoot amid quiet newsflow for the complex, and after yesterday’s modestly firmer settlement. Chinese trade data added more concerns regarding Chinese demand after imports missed expectations. Tropical Storm Francine, which is expected to strengthen into a hurricane today before making landfall tomorrow; Brent sits in a USD 70.71-72.28/bbl parameter.

Precious metals are mixed with spot gold and silver subdued and palladium once again outperforming, albeit off highs in recent trade.

Base metals tilt lower in subdued trade after the Chinese trade data reinforced weak domestic demand as imports missed forecasts. 3M LME copper trades in a narrow 9,070.50-9,150.50/t range.

Spot gold is slightly softer, but with trade fairly rangebound in the European morning; XAU currently sits just above USD 2.5k/oz in a narrow USD 2500.26-2507.72/oz range.

Base metals are almost entirely in the red,

NHC said Francine is expected to become a hurricane soon with storm surge and hurricane warnings in effect for the Louisiana coast.

US Coast Guard ordered the closure of Brownsville and other small Texas ports, while the port of Corpus Christi remained open under vessel traffic restrictions, according to an advisory.

NHC said strong winds and dangerous storm surge expected along the Louisiana coast tomorrow.

NHC said Francine is likely to become a hurricane today

Chevron (CVX) announced to evacuate all staff and shut in oil and gas production at two US Gulf of Mexico platforms.

Shell (SHEL LN) announced to shut oil production at Perdido offshore platform in US Gulf of Mexico citing downstream impacts.

Goldman Sachs said strong production and disappointing demand pose a downside risk to their US gas price forecast, while it added that Tropical Storm Francine is expected to further reduce power demand and potentially impact LNG exports out of the Gulf.

China oil industry researcher said China oil products demand is projected to fall by an average of 1.1% annually between 2023-2025.

India Steel Minister said the Indian steel ministry backs taxing imports

Geopolitics: Ukraine

Israeli military said it conducted an air strike which targeted a Hamas command centre in Khan Younis, while Hamas media reported the death toll from the Israeli strike on a Gaza tent encampment was at least 40.

US President Biden was reported to convene his national security team to discuss the impasse in negotiations on the hostage deal, according to Axios’s Barak Ravid citing sources.

Yemeni Houthis noted that they downed US MQ-9 drone in Saada

Geopolitics: Other

Moscow’s Vnukovo and Domodedovo Airports stopped flights after reports of nearby drone attacks, while it was separately reported that a fire broke out at a multi-storey residential building in Moscow’s Ramenskoye district as a result of a drone attack.

North Korean leader Kim said they must prepare North Korea’s nuclear capability and readiness to use it properly at any given time, while they are implementing a nuclear force construction policy to increase the number of nuclear weapons exponentially, according to KCNA.

Russian forces have attacked energy infrastructure in eight Ukrainian regions in the last 24 hours, according to the energy ministry cited by Reuters.

Russian Security Council Secretary Shoigu said Russia has enough forces and continues its offensive, according to Ria

US Event Calendar

06:00: Aug. SMALL BUSINESS OPTIMISM, est. 93.6, prior 93.7

Central Bank speakers

10:00: Fed’s Barr Speaks on Basel III Endgame

12:15: Fed’s Bowman Gives Speech on Stress Testing

DB’s Jim Reid concludes the overnight wrap

This week I celebrate 20 years since I left gardening leave, a climb to the top of Kilimanjaro, and my one and only ever half marathon behind, and started at DB. How time flies. It’s been an eventful and enjoyable ride so far and how long it lasts likely depends on a combination of DB’s tolerance and when my kids leave the payroll. The latter date may be greater than the former! We will see.

There have been far more eventful days in those past 20 years than yesterday but after the September stresses so far, risk assets have recovered over the last 24 hours, with the S&P 500 (+1.16%) posting a decent advance after its worst weekly performance since SVB’s collapse. There wasn’t a single catalyst for the recovery, but in a constantly flip-flipping macro narrative the sense yesterday was that last week’s fears about a sharper US downturn were overdone, and the headline data (including payrolls at +142k) still wasn’t consistent with a recession. In the meantime, with confidence growing about the outlook, that led investors to dial back the chance that the Fed would deliver a 50bp cut next week. Tonight we see the long awaited Trump vs Harris TV debate take place at 9pm EST time. So it will be all over a couple of hours before we go to press tomorrow and is the only confirmed debate between the two candidates exactly 8 weeks today until polling day. The election has moved down the pecking order of macro topics of late after dominating mid-summer, likely as Harris reversed what was looking like a strong polling momentum towards a red sweep before Biden stood aside.

In recent days, the general perception from polls, betting odds and forecasting models is that Trump has regained a bit of ground relative to where things stood after the Democratic convention. In particular, there was a lot of focus on a national New York Times/Siena poll, which showed Trump ahead of Harris by 48-47%, and that’s considered a high-quality poll. Now that’s been at the upper end of the recent range for Trump, and the RealClearPolitics average still has Harris ahead by 1.2pts. But given the Republicans have the slight advantage in the Electoral College, Harris likely needs to be a bit further ahead of Trump in the national vote to be confident of victory. Perhaps with tonight’s debate and once we know for certain whether the Fed are going to ease 25 or 50bps next week, we’ll be back to talking about the election more.

Back to the last 24 hours and the more positive momentum shift was down to sentiment rather than any new data, but investors got a reminder that growth is certainly not currently falling off a cliff given the updated Atlanta Fed’s GDPNow update. The latest reading yesterday included Friday’s jobs report, which lifted the Q3 growth estimate from an annualised +2.1% rate to +2.5%. If realised, that would be the 8th quarter in the last 9 where growth is running at an annualised pace above 2%. Along similar lines, the New York Fed’s Staff Nowcast stood at +2.6% for Q3 on Friday, so still pointing well away from recessionary levels. Adding to the generally resilient cyclical data, yesterday’s US consumer credit release for July (+$25.5bn) showed the strongest monthly rise since October 2022.

Against that backdrop, risk assets posted a recovery on both sides of the Atlantic. For equities, that saw the S&P 500 (+1.16%) post its biggest daily gain in three weeks, after a run of four consecutive declines. This was a broad rebound, with all but one of the 24 industry groups higher on the day, and more cyclical sectors including consumer discretionary (+1.63%), industrials (+1.56%) and information technology (+1.42%) leading the way. The Magnificent 7 advanced +1.37% amidst strong gains from Nvidia (+3.54%) and Tesla (+2.63%). Meanwhile in Europe it was much the same story, with the STOXX 600 (+0.82%) finally making up some ground after falling every day last week.

Elsewhere, as optimism grew on the economy, it led investors to price in a greater chance that the Fed would only cut rates by 25bps next week. Indeed, futures were giving a 50bp cut a 31% probability by the close, which is its joint lowest level over the past two weeks. In turn, that led to a rise in front-end Treasury yields, with the 2yr yield up +2.2bps to 3.67%. However, there was a fresh move lower for the 10yr yield, which fell -0.9bps to 3.70%, which is its lowest closing level since June 2023.

When it comes to next week’s Fed decision, the last big piece of data beforehand will be tomorrow’s CPI release for August, which could help tilt the balance between 25 and 50, particularly if there were a big surprise in either direction. For our US economists’ CPI preview, and to register for their post-release webinar, see here. We’ll have to wait and see what that brings, but yesterday did see the New York Fed release their latest Survey of Consumer Expectations, where inflation expectations were broadly unchanged. The 1yr expectation series remained at 3.0%, 3yr expectations ticked up two-tenths to 2.5%, and the 5yr expectation was unchanged at 2.8%.

Back in the political sphere, former ECB President Mario Draghi published his long-awaited report into European competitiveness yesterday. Among others it called for additional investments of €750-800bn per year, and it said that some “joint funding of investment at the EU level is necessary to maximise productivity growth”. Overall the report contained a fairly blunt message, and Draghi said to reporters that “For the first time since the Cold War we must genuinely fear for our self-preservation”. The reality though is that Europe is struggling for the political capital to rally around delivering the findings of Draghi’s report. So whether the 400 pages in the report can make a difference is a moot political point.

Asian equity markets are relatively quiet this morning with the Hang Seng (+0.09%), Nikkei (+0.01%), and the KOSPI (+0.05%) trading just above flat. Elsewhere, Chinese stocks are lower with the CSI (-0.54%) approaching its lowest close since January 2019 while the Shanghai Composite (-0.53%) is also trading in the red. S&P 500 (-0.14%) and NASDAQ 100 (-0.36%) futures are pulling back a little of yesterday’s gains.

Early morning data showed that China’s export growth in August (+8.7% y/y) surpassed market expectations for a +6.6% gain, and up from the +7.0% increase seen in July. However, import growth slowed to +0.5% y/y in August (v/s +2.5% expected), down from a +7.2% advance in the previous month, thus indicating weakening domestic demand, possible import substitution, and an excess of domestic production. The trade surplus stood at $91.02 billion, (v/s $81.10 expected) and up from $84.65 billion in July.

To the day ahead now, and one of the main highlights will be the TV debate tonight between Kamala Harris and Donald Trump. Otherwise, data releases include UK unemployment and Italian industrial production for July, whilst in the US there’s the NFIB’s small business optimism index for August. Finally from central banks, we’ll hear from Fed Vice Chair for Supervision Barr.

Tyler Durden

Tue, 09/10/2024 – 08:16