42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Key Events This Week: Republican Convention, Retail Sales, Powell Speaks And Many More Earnings

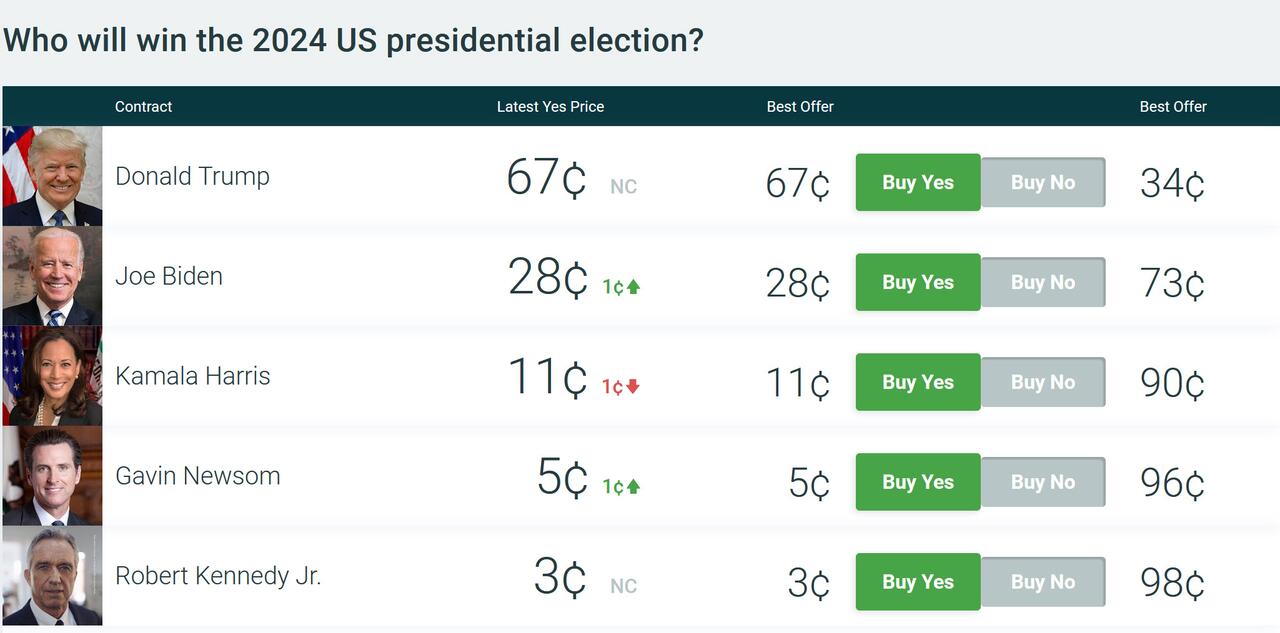

As DB’s Jim Reid writes (on his “day off”), the week starts off with the financial world assessing what the failed assassination attempt on Donald Trump means for the Presidential race and for markets. PredictIt has the probability of a Trump victory increasing from around 55% on Friday to around 65%.

{kind=link}

On a state basis, the shooting took place in Pennsylvania, one of the three most important battleground states and one Biden needs to win to be President given where current polling is. Before the weekend Trump was around 3.5% ahead in the state in the latest poll of polls. When Biden performed poorly in the debate 2 and a half weeks ago, Treasuries sold off 20bps in a couple of sessions as markets looked to price in a more fiscally loose Trump clean sweep. And with the Republican National Convention starting today, there will be plenty of politics all week.

Outside of the Presidential race, the most consequential event of the week could come today as Fed Chair Powell is interviewed at the Economic Club of Washington DC at 5pm London time. Will his tone take a notably dovish shift given the soft CPI print last week? DB’s economists new Fed forecasts would suggest he might as they now expect three cuts in the remainder of 2024 (Sep, Nov, Dec) as a mid-cycle adjustment before three more from September 2025. Eight other FOMC voters will also be on the radar this week (see them detailed in the diary at the end) so we’ll have a good idea of whether the Fed are moving direction by the end of the week. Interestingly, DB economists point out that back in December 2023 and March 2024 the Fed median forecasts from the SEP expected 75bps of cuts this year with unemployment at 4.0-4.1% and core PCE inflation 2.4-2.6% by year-end. Recent data suggest that reasonable year-end forecasts are now 4.0-4.2% for unemployment and 2.5-2.6% for core PCE.

Staying with central bankers, the ECB meets on Thursday with the council expected to vote to stay on hold for now. Also watch for the quarterly ECB bank lending survey tomorrow. This has tentitatively turned more positive in the last couple of quarters, especially in the expectations component.

In terms of the other main non-data highlights, earnings season in the US starts to build, China’s Third Plenum starts today through to Thursday with all eyes on potential policies and reforms targeted at key economic issues including the property sector (the market, understandably, expects very little from Beijing). On the same days the Republican National Convention will take place with the main event being the unveiling of the Vice President nomination and the reaction to the assassination attempt. Staying with politics, Wednesday sees the UK State Opening of Parliament and the King’s Speech which contains the new government’s legislative program for the year. The following day sees a European Parliament vote on whether European Commission President Von der Leyen gets a second term.

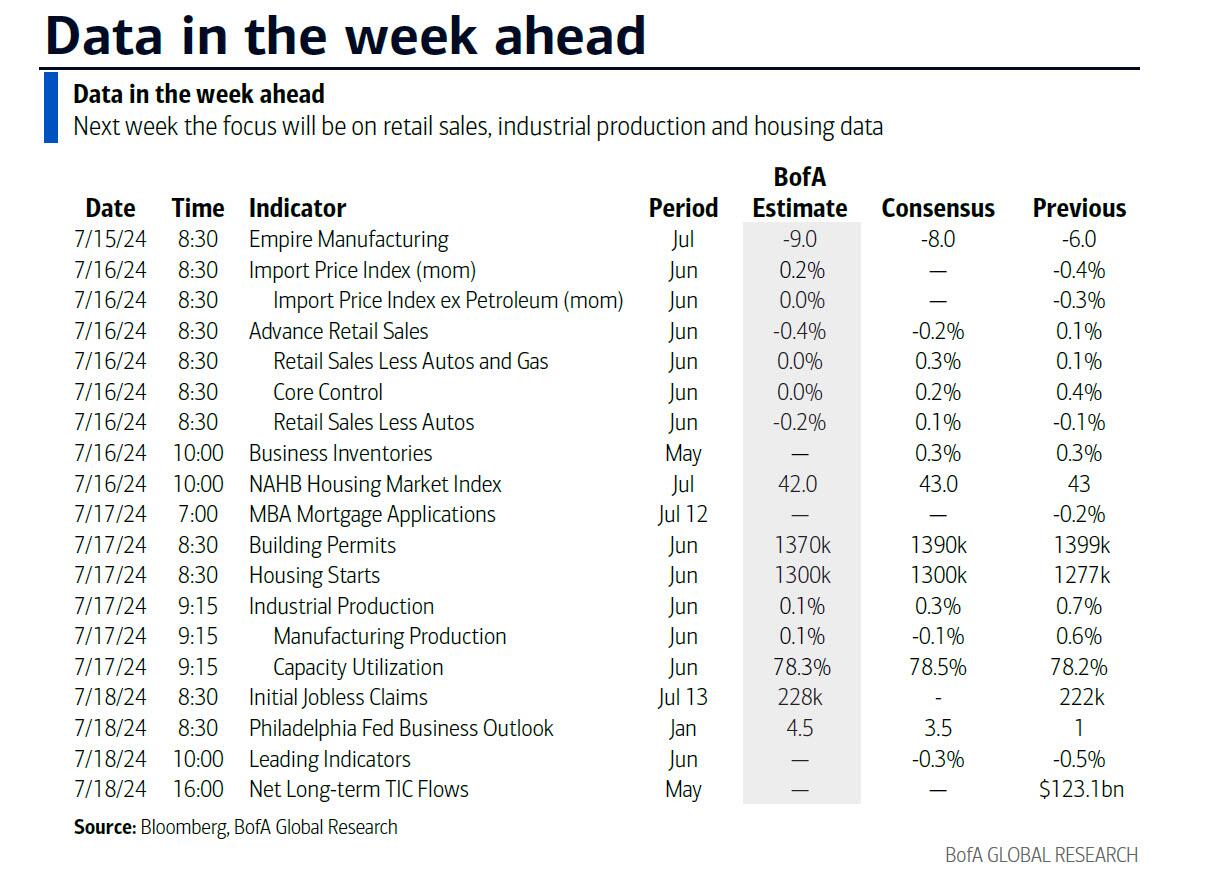

In terms of data and earnings, on a day by day basis the highlights are as follows: Today sees US Empire manufacturing, Eurozone IP with Blackrock and Goldman reporting. Tomorrow sees the very important US retail sales, the NAHB US housing index, German/EuroZone ZEW survey, Canadian CPI with BoA and Morgan Stanley reporting. Wednesday sees US IP, capacity ulitisation, building permits, housing starts, the Fed Beige Book, UK CPI, a 20yr UST auction with Johnson and Johnson and ASML the earnings highlights. Thursday sees the US Phili Fed index, jobless claims as ever, UK employment data, and with TSMC and Netflix reporting. Friday sees Japanese CPI, UK retail sales and public finance data, German PPI with Amex the earnings highlight.

{kind=link}

Also of note will be the stock market after a fascinating week last week where the Mag-7 underperformed the index with the highlight being Thursday’s largest performance gap between the S&P 500 and the equal weighted equivalent since November 2020, just after the Pfizer vaccine announcement. Reid did what he thought was a very good CoTD on Friday reminding readers of what happened to other sectors when the tech bubble burst in March 2000. The three “dullest” sectors (Consumer Staples, Healthcare and Utilities) had performed badly in the last few months of the bubble but rallied +25-35% in the final 9 months of the year as tech slumped. It wasn’t until 2001 and 2002 that the wider market really slumped. So if tech does see a correction, the market will likely go down given their size, but several sectors could rally notably.

Finally, on the earnings front we have Goldman and Blackrock today, Bank of America tomorrow, ASML, JNJ and United Wednesday, Netflix Thursday and American Express reporting on Friday.

{kind=link}

Day-by-day calendar of events

Monday July 15

Data : US July Empire manufacturing index, China Q2 GDP, June new home prices, industrial production, retail sales, property investment, Eurozone May industrial production, Italy May general government debt, Canada May manufacturing sales

Central banks : Fed’s Powell and Daly speak, China 1-yr MLF rate, BoC’s business outlooksurvey

Earnings : BlackRock, Goldman Sachs

Other : US Republic National Convention (through July 18), China Third Plenum (through July 18)

Tuesday July 16

Data : US June retail sales, import price index, export price index, May business inventories, July NAHB housing market index, New York Fed services business activity, Japan May Tertiary industry index, Germany July Zew survey, Italy May trade balance, Eurozone July Zew survey, May trade balance, Canada June CPI, housing starts, New Zealand Q2 CPI

Central banks : Fed’s Kugler speaks, ECB’s bank lending survey

Earnings : Bank of America, Morgan Stanley, UnitedHealth, Ocado

Wednesday July 17

Data : US June industrial production, building permits, housing starts, capacity utilisation, UK June CPI, RPI, PPI, May house price index, Canada May international securities transactions

Central banks : Fed’s Beige Book, Barkin and Waller speak

Earnings : Johnson & Johnson, ASML, Prologis, Alcoa

Auctions : US 20-yr Bond (reopening, $13bn)

Other : UK State Opening of Parliament and King’s Speech

Thursday July 18

Data : US July Philadelphia Fed business outlook, June leading index, May total net TIC flows, initial jobless claims, UK May average weekly earnings, unemployment rate, June jobless claims change, Japan June trade balance, EU27 June new car registrations, Eurozone May construction output

Central banks : ECB decision, Fed’s Logan and Daly speak

Earnings : TSMC, Netflix, Blackstone, Abbott Laboratories, Intuitive Surgical, Novartis, Domino’s Pizza, Volvo, EQT, Nokia

Auctions : US 10-yr TIPS ($19bn)

Friday July 19

Data : UK July GfK consumer confidence, June retail sales, public finances, Japan June national CPI, Germany June PPI, Italy May current account balance, ECB May current account, Canada May retail sales, June industrial product price index, raw materials price index

Central banks : Fed’s Bowman, Williams and Bostic speak, ECB’s survey of professional forecasters

Earnings : Schlumberger, American Express, Evolution

* * *

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the retail sales report on Tuesday and the Philly Fed manufacturing index on Thursday. There are several speaking engagements from Fed officials this week, including remarks from Chair Powell on Monday.

Monday, July 15

08:30 AM Empire State manufacturing survey, July (consensus -7.2, last -6.0)

12:30 PM Fed Chair Powell speaks: Fed Chair Jerome Powell will be interviewed by David Rubenstein at the Economic Club of Washington DC. A Q&A is expected. In his Congressional Testimony on July 11, Powell said “I do have some confidence [that inflation is moving down to 2%], I think we’ve seen that over the past several years. The question is, are we sufficiently confident that it’s moving sustainably down to 2% and I’m not prepared to say that yet.” He also said “remember, we have a dual mandate too, and I could also see us cutting if we saw unexpected weakening in the labor market. I’ll speak for myself, I now see the risk to the two mandates as much closer to being balanced.”

04:35 PM San Francisco Fed President Daly (FOMC voter) speaks: San Francisco Fed President Mary Daly will speak in a moderated conversation about the US economy, how tech advancements will impact monetary policy, and AI’s impact on the labor market at the Fortune Brainstorm Tech conference. A Q&A is expected. On July 11, Daly said “The economy looks to be on a path where one or two rate cuts this year would be more or less the appropriate path.”

Tuesday, July 16

08:30 AM Retail sales, June (GS -0.2%, consensus -0.2%, last +0.1%); Retail sales ex-auto, June (GS +0.3%, consensus +0.1%, last -0.1%); Retail sales ex-auto & gas, June (GS +0.5%, consensus +0.3%, last +0.1%); Core retail sales, June (GS +0.5%, consensus +0.2%, last +0.4%): We estimate core retail sales expanded 0.5% in June (ex-autos, gasoline, and building materials; mom sa). Our forecast reflects firming sales among retailers and a potential boost from Juneteenth celebrations. We estimate a 0.2% drop in headline retail sales, reflecting lower gasoline prices and sharply lower auto sales due to disruptions from cyberattacks.

08:30 AM Import price index, June (consensus -0.2%, last +0.4%): Export price index, June (consensus -0.1%, last -0.6%)

10:00 AM Business inventories, May (consensus +0.5%, last +0.3%)

10:00 AM NAHB housing market index, June (consensus 44, last 43)

02:45 PM Fed Governor Kugler speaks: Fed Governor Adriana Kugler will speak at a NABE conference in Washington D.C. on challenges facing economic measurement. Speech text and a Q&A are expected. On June 18, Kugler said “if the economy evolves as I am expecting, it will likely become appropriate to begin easing policy sometime later this year.”

Wednesday, July 17

08:30 AM Housing starts, June (GS +3.5%, consensus +1.8%, last -5.5%): Building permits, June (consensus -0.3%, last -2.8%)

09:00 AM Richmond Fed President Barkin (FOMC voter) speaks: Richmond Fed President Thomas Barkin will give informal remarks on the economy and take audience questions in Landover, Maryland. On June 28, Barkin said “as for me, I do believe there are still lags playing out — and that all this tightening will eventually slow the economy further. At the same time, given the remarkable strength we are seeing in the economy, I’m open to the idea that r-star has shifted up somewhat.”

09:15 AM Industrial production, June (GS +0.3%, consensus +0.3%, last +0.7%): Manufacturing production, June (GS +0.2%, consensus +0.1%, last +0.9%): Capacity utilization, June (GS 78.3%, consensus 78.5%, last 78.2%): We estimate industrial production increased 0.3%, reflecting strong natural gas, mining, and electricity production. We estimate capacity utilization increased to 78.3%.

09:35 AM Fed Governor Waller speaks: Fed Governor Christopher Waller will speak about the economic outlook at a Federal Reserve Bank of Kansas City event. Speech text and a Q&A are expected. On May 21, Waller said “I need to see several more months of good inflation data before I would be comfortable supporting an easing in the stance of monetary policy.” He also said, “if we get enough data going the right way, then we can think about cutting rates later this year, beginning of next year.”

02:00 PM Beige Book, July Meeting period: The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. The Beige Book for the June FOMC meeting period noted that activity continued to expand this spring, but that conditions varied across sectors and Districts. Businesses continued to report weakness in discretionary spending due to heightened price sensitivity among consumers. Tight credit standards and high interest rates continued to constrain lending growth. In this month’s Beige Book, we look for anecdotes related to possible turning points in regional labor markets and for further commentary on businesses’ inflation expectations over the next few months.

Thursday, July 18

08:30 AM Initial jobless claims, week ended July 13 (GS 220k, consensus 230k, last 222k); Continuing jobless claims, week ended July 6 (consensus 1,857k, last 1,852k)

08:30 AM Philadelphia Fed manufacturing index, July (GS 3.0, consensus 2.9, last 1.3)

01:45 PM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will give opening remarks at a conference co-hosted by the Federal Reserve Banks of Dallas and Atlanta. Speech text is expected.

06:05 PM San Francisco Fed President Daly (FOMC voter) speaks: San Francisco Fed President Mary Daly will participate in a fireside chat at a conference co-sponsored by the Federal Reserve Banks of Dallas and Atlanta.

07:45 PM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will give the keynote address at a conference co-hosted by the Dallas and Atlanta Fed on accountability and reform. Speech text is expected. On June 27, Bowman said “my baseline outlook continues to be that inflation will decline further with the policy rate held steady,” and went on to say “we are still not yet at the point where it is appropriate to lower the policy rate, and I continue to see a number of upside risks to inflation.”

Friday, July 19

10:40 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will participate in a panel session on “A New Era for Monetary Policy” at an event hosted by the Central Reserve Bank of Peru (BCRP), Reinventing Bretton Woods Committee (RBWC), and Inter-American Development Bank (IDB). A Q&A is expected. On July 3, Williams said “r-star is either explicitly or implicitly at the core of any macroeconomic model or framework one can imagine” but that “the high degree of uncertainty about r-star means that one should not overly rely on estimates of r-star in determining the appropriate setting of monetary policy at a given point in time.”

01:00 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will give closing remarks at a conference co-hosted by the Federal Reserve Banks of Dallas and Atlanta.

Source: DB, Goldman

Tyler Durden

Mon, 07/15/2024 – 10:20