42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Goldman Net Income Surges 150% As Investment Banking Misses, Credit Loss Provisions Slide

After a mixed bag of results from JPMorgan on Friday and a downright ugly net interest margin report from Wells, moments ago Goldman Sachs reported second quarter profits which more than doubled to $3bn as both fixed-income and equity traders outpaced analysts’ estimates, offset by a small miss in investment banking, while a rebounding capital-markets business helped drive better-than-expected results across much of the company’s Wall Street operations.

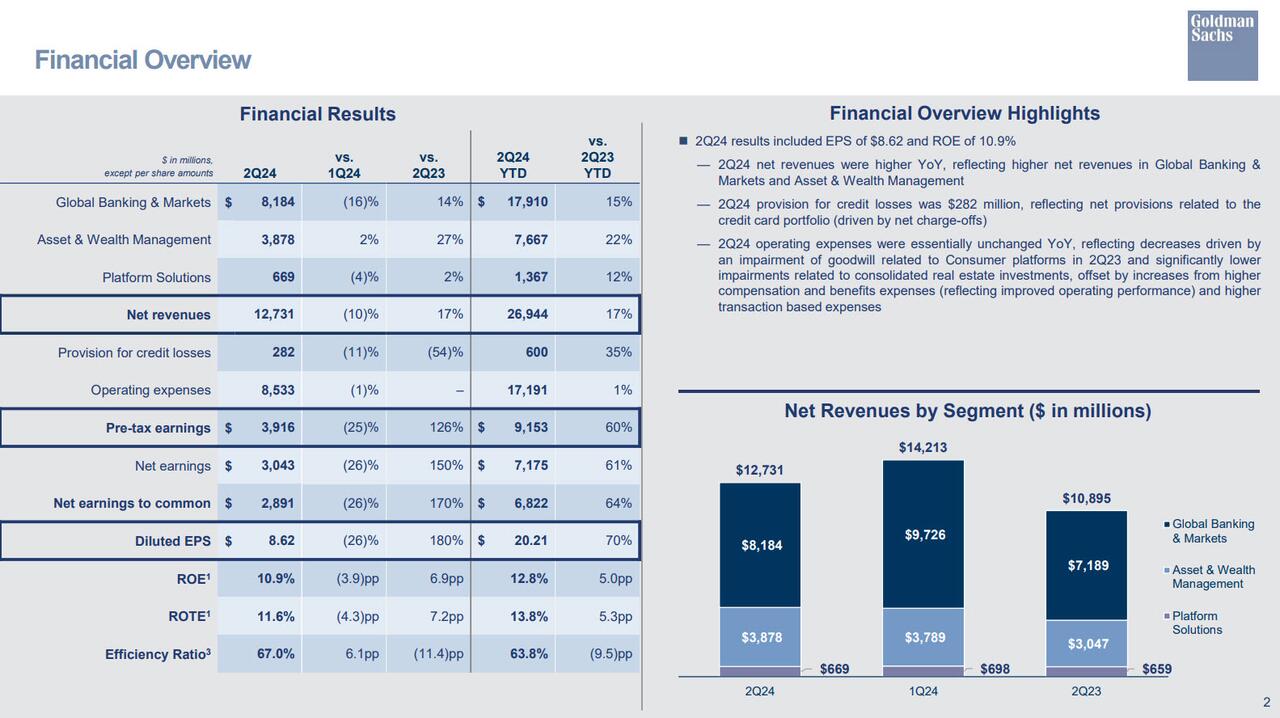

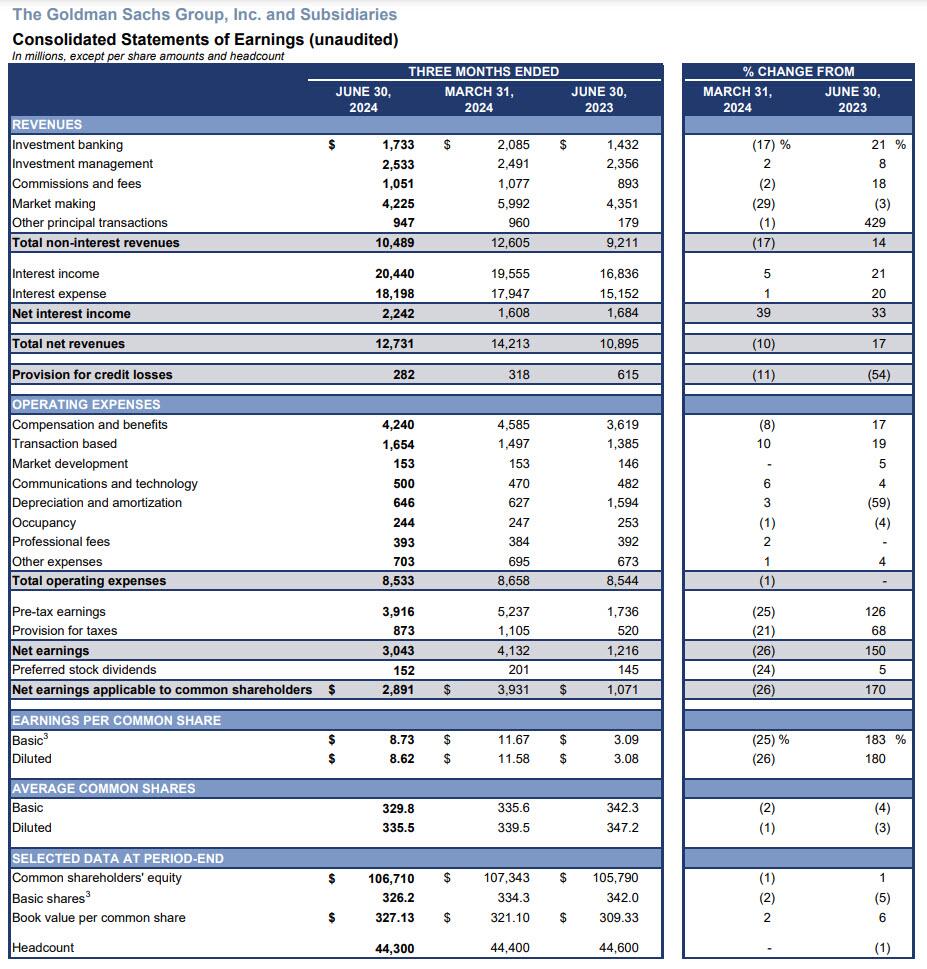

Net income of just over $3 billion exceeded the $2.8 billion analysts were expecting and was up 150% from $1.2bn a year earlier when it was plagued by losses in real estate investments and the consumer-banking unit in the middle of an industrywide dealmaking slowdown. This translated to a 180% increase in EPS to $8.62, beating estimates of $8.34, and was thanks to revenue of $12.73 billion which also beat estimates of $12.46 billion, and was 17%higher than a year ago.

{kind=link}

{kind=link}

Here are the top highlights from the reported Q2 earnings:

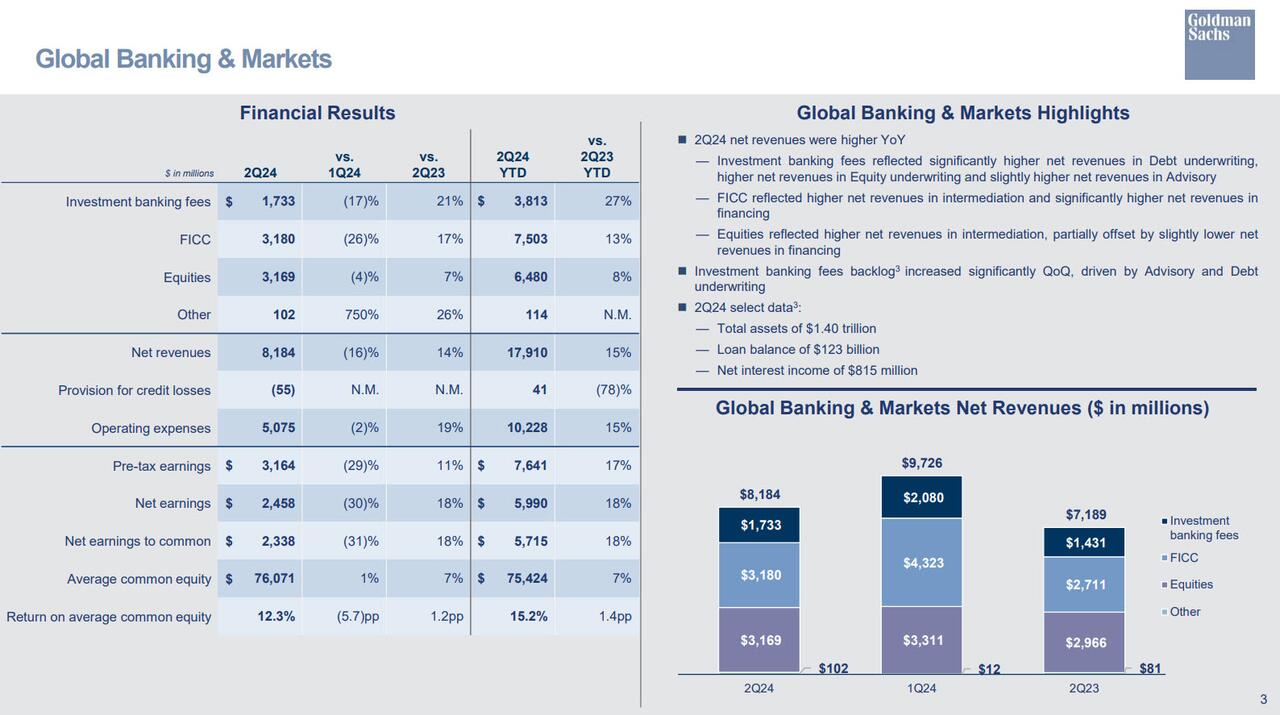

Global banking and Markets revenue $8.184BN, up15% YoY, and beating est of $7.95BN

FICC sales and trading $3.18BN, up 13% YoY and beating est of $3.02BN

Equity sales and trading $3.169BN, up 8% YoY and beating est $3.08BN

The one downside was the latest miss in Investment Banking revenue, which rose 27% YoY to $1.73BN, missing est of $1.82BN. Merger-advisory fees were $688 million. That was less than the $785 million that JPMorgan reported last week. According to Bloomberg, Goldman tends to lead the industry in that business and rarely falls behind its rival. As more businesses are on the prowl for deals, the approaching US elections could further delay a return to the pace of growth in the merger business seen in recent years. The business is especially important for Goldman because the firm has tried to showcase its strong investment bank and growing asset-management business, after abandoning an expansion into consumer banking

{kind=link}

Taking a closer look at results, Goldman said the following:

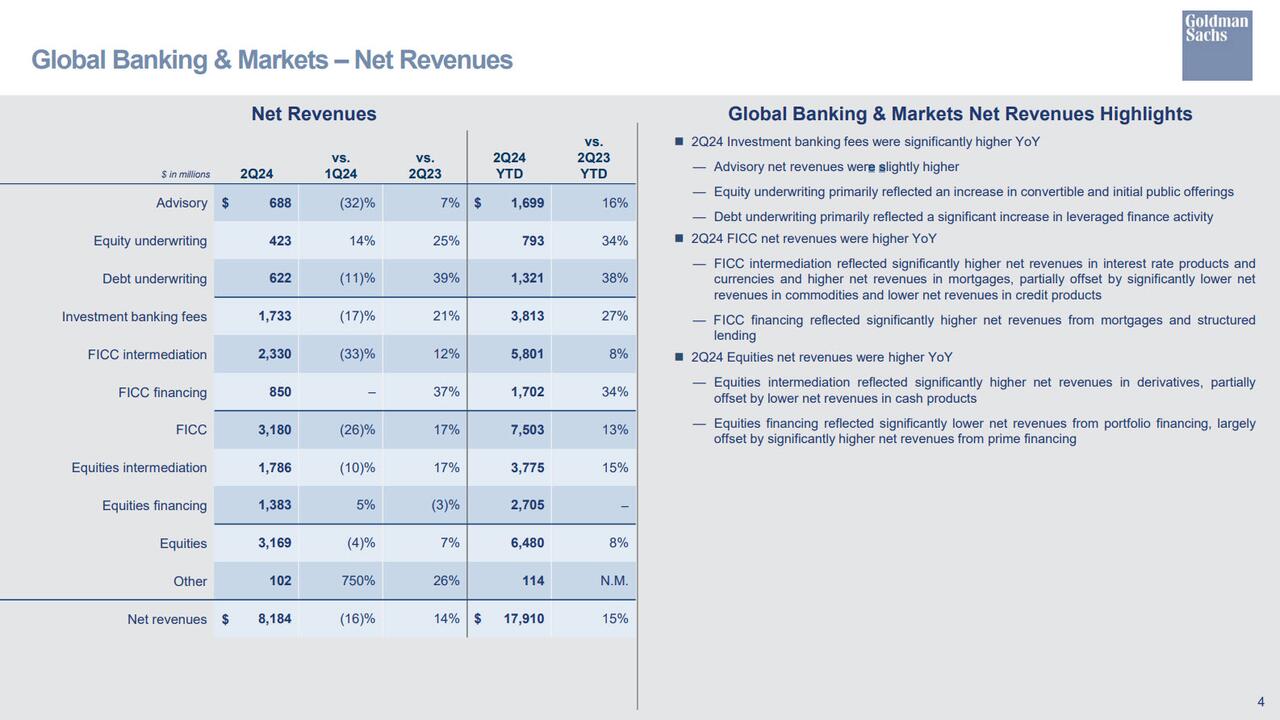

FICC reflected higher net revenues in intermediation and significantly higher net revenues in financing

FICC intermediation reflected significantly higher net revenues in interest rate products and currencies and higher net revenues in mortgages, partially offset by significantly lower net revenues in commodities and lower net revenues in credit products

FICC financing reflected significantly higher net revenues from mortgages and structured lending

Equities reflected higher net revenues in intermediation, partially offset by slightly lower net revenues in financing

Equities intermediation reflected significantly higher net revenues in derivatives, partially offset by lower net revenues in cash products

Equities financing reflected significantly lower net revenues from portfolio financing, largely offset by significantly higher net revenues from prime financing

investment banking fees reflected significantly higher net revenues in Debt underwriting, higher net revenues in Equity underwriting and slightly higher net revenues in Advisory

Advisory net revenues were slightly higher

Equity underwriting of $423 million primarily reflected an increase in convertible and initial public offerings

Debt underwriting revenue was $622 million and primarily reflected a significant increase in leveraged finance activity

{kind=link}

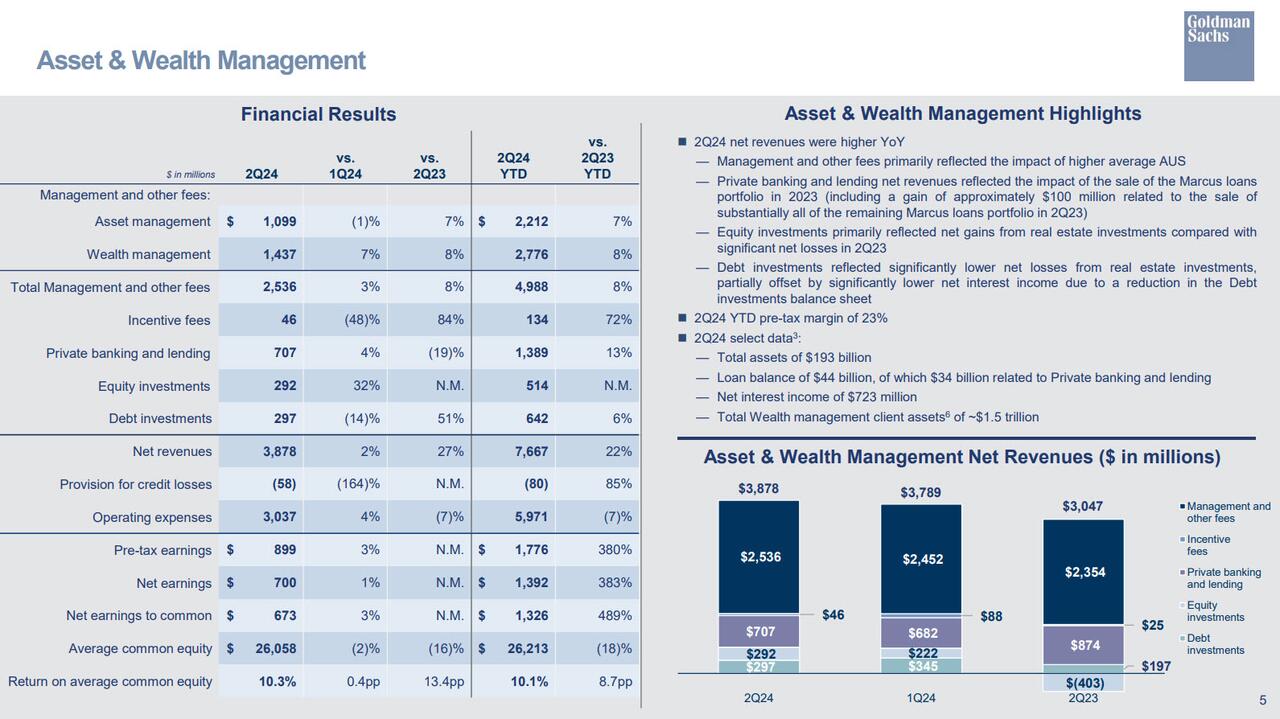

Meanwhile, revenue in asset and wealth management, a key division Goldman is relying on to diversify its revenue stream, increased 27% to $3.88 billion. Management fees climbed 8% as the bank seeks to shift growth to those fees instead of windfalls from balance-sheet investments.

{kind=link}

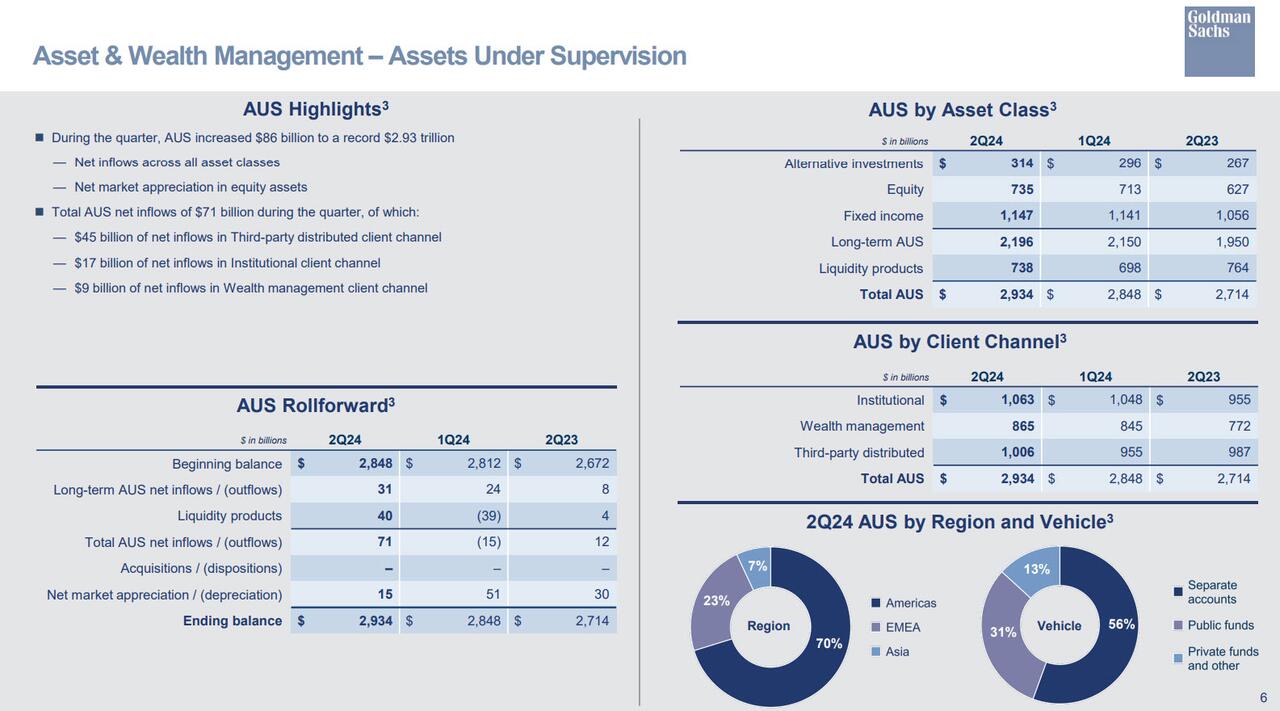

The bank’s total Assets Under Supervision rose to $2.934 trillion from $2.714 trillion a year ago, driven by a jump in assets across the board including alternative investments, equity and fixed income (see below).

{kind=link}

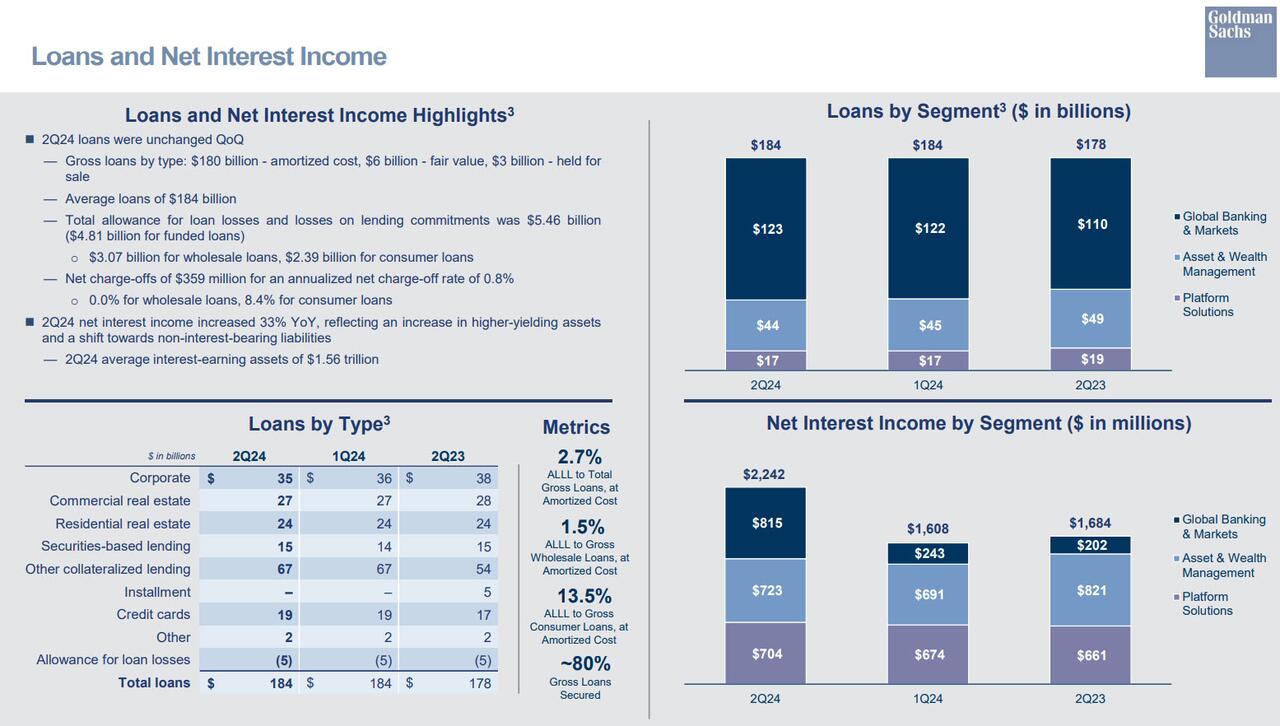

Some other numbers: total loans were unchanged sequentially at $184 billion (up from $178BN a year ago); net interest income increased 33% YoY “reflecting an increase in higher-yielding assets and a shift towards non-interest bearing liabilities”, i.e., the end of paying interest on deposits.

{kind=link}

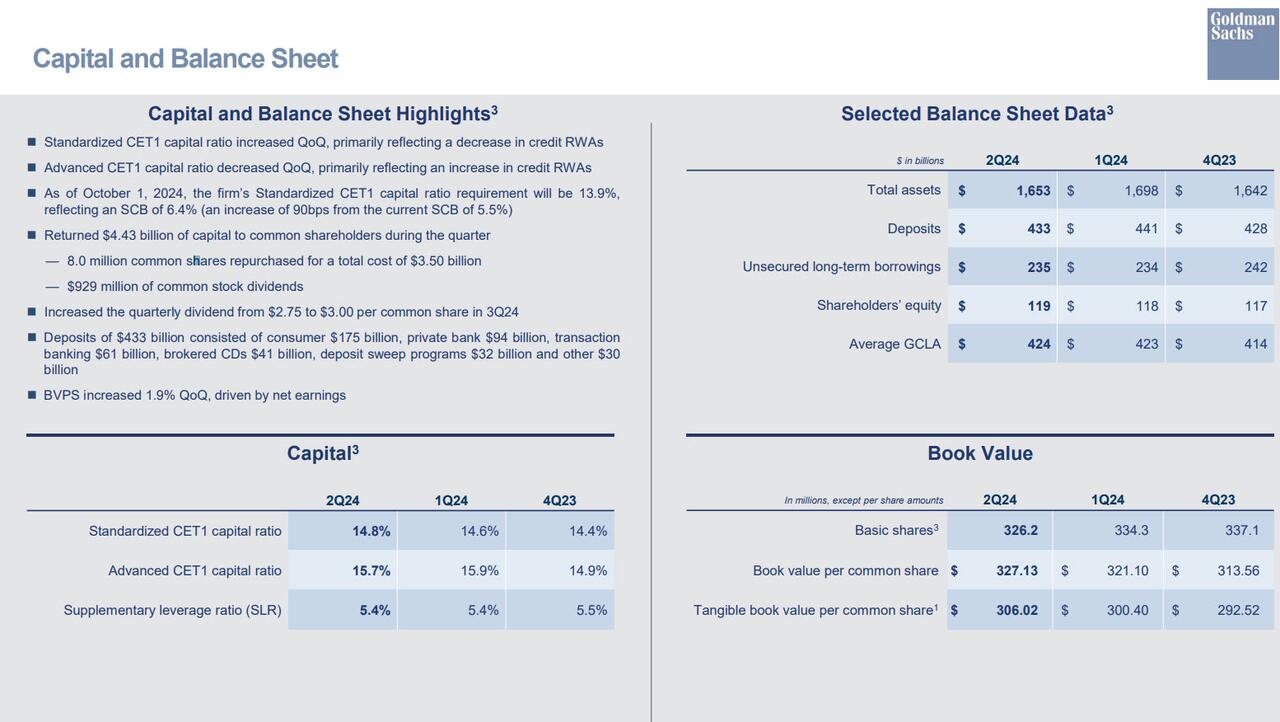

Meanwhile deposits declined 1.8% QoQ to $433 billion, and consisted of consumer $175 billion, private bank $94 billion, transaction banking $61 billion, brokered CDs $41 billion, deposit sweep programs $32 billion and other $30 billion.

{kind=link}

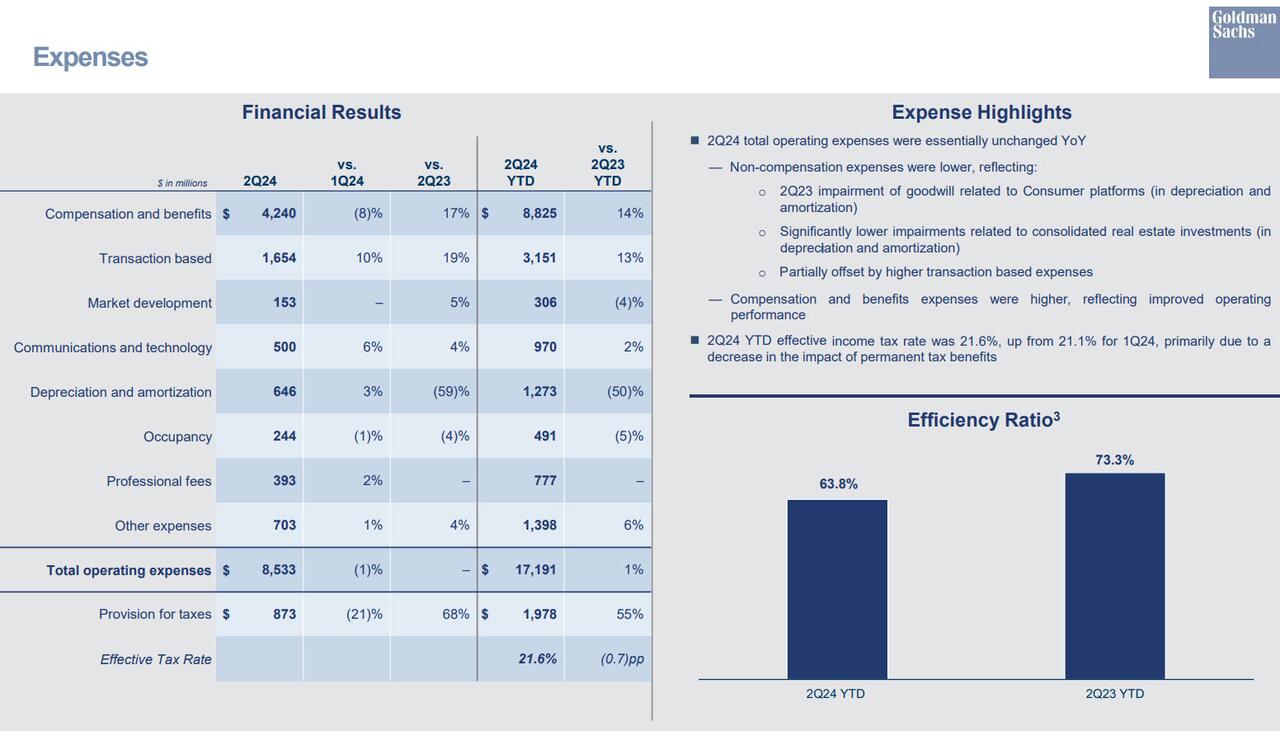

Finally, expenses of $8.5 billion were largely unchanged both MoM and YoY.

Non-compensation expenses were lower, reflecting:

2Q23 impairment of goodwill related to Consumer platforms (in depreciation and amortization)

Significantly lower impairments related to consolidated real estate investments (in depreciation and amortization)

Partially offset by higher transaction based expenses

Compensation and benefits expenses were higher, reflecting improved operating performance

{kind=link}

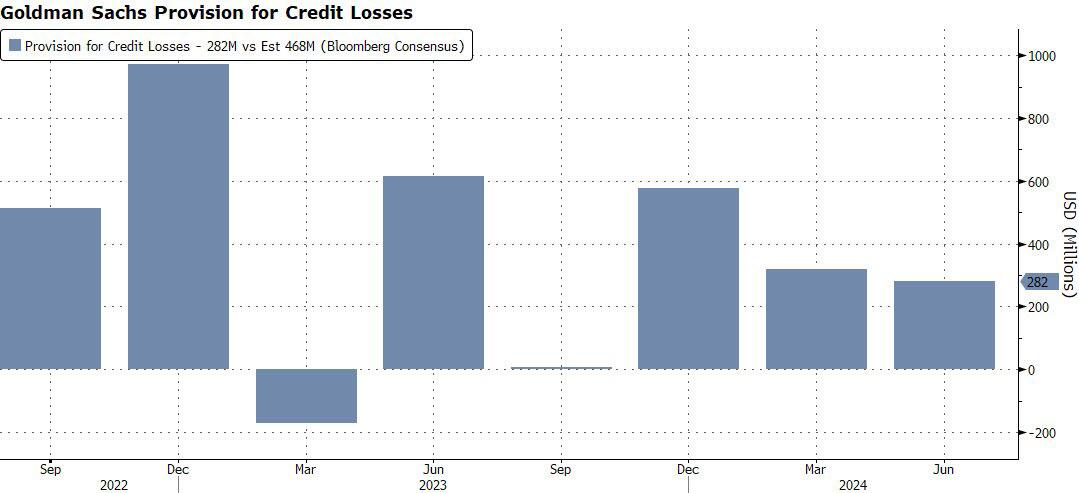

While Goldman’s revenue improved notably, it is worth noting that the bank’s $282 million provision for credit losses dropped sharply from a number that last year was more than twice as high, at $615 million; it was also down from last quarter’s $318 million. This is curious as it comes at a time when JPMorgan saw its own reserve build surge to the highest since the bank collapse quarter in Q1 2023.

{kind=link}

According to Bloomberg, the main culprit is the credit card portfolio and its net charge-offs: “That’s a simple, and important, story. The picture was foggier last year, when there were “net provisions related to the credit card and point-of-sale loan portfolios (driven by net charge-offs and growth) and wholesale loans (driven by impairments), partially offset by a reserve reduction related to the repayment of a term deposit with First Republic Bank.”

In any case, the rebound in mergers and acquisitions and debt deals has helped drive Goldman’s shares up by a quarter this year, outperforming the 13% rise in the KBW Bank index and the 18% advance in the S&P 500 over the same period.

Despite the modest miss, the continued recovery in investment banking will help Goldman draw a line under a fraught 12 months in which chief executive David Solomon’s management of the bank came under fire. “We are pleased with our solid second-quarter results and our overall performance in the first half of the year, reflecting strong year-on-year growth in both global banking and markets and asset and wealth management,” Solomon said in a statement.

Last month, in a surprise move, the bank tapped John Mahoney, a financial-services banker who has been with the firm since 1987, to oversee firmwide strategy. That’s a departure from recent years, when Goldman had been tapping younger, fast-rising executives destined for bigger jobs at the firm for a similar role. The firm is also turning to a merger banker for a strategy role at a time when it has preached caution about the need for acquisitions to grow, especially after pursuing multiple deals to build out a retail-banking business that flopped. Goldman has instead tried to pare its focus to expanding its investment bank and money-management business to achieve its mid-teens return-on-equity target. It fell short of that mark in the second quarter, notching 10.9%.

Goldman said last quarter that it raised its biggest war chest yet for private-credit wagers. The firm closed the latest iteration of its direct-lending fund, which along with separately managed accounts for the same strategy amounted to $21 billion. The bank also clinched a $43 billion mandate to invest pension-fund assets of parcel-delivery company UPS, in one of the largest deals of its kind.

Commenting on the results, Bloomberg’s Sridhar Natarajan writes that “both fixed-income and equity traders outpaced analysts’ estimates, while a rebounding capital-markets business helped drive better-than-expected results across much of the company’s Wall Street operations. Still, in a surprise reversal, the company pocketed less in fees from arranging mergers than JPMorgan”

Following a kneejerk move higher, the stock slumped to session lows before stabilizing largely unchanged. Goldman shares advanced 24% this year, propelling the stock to an all-time high of $479.88 on Friday.

{kind=link}

The full investor presentation can be found here (pdf link).

Tyler Durden

Mon, 07/15/2024 – 09:05