42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

What Is Happening To Incomes?

Authored by Jeffrey Tucker via The Epoch Times,

Yesterday I paid a visit to my favorite local grocery, a family-owned boutique with wonderful products from around the world. It does tremendous business because of its customer focus and excellent selection due to stable supplier relationships. This is what allowed them to survive these terrible years, including the inflation that has rattled its customer base.

{kind=link}

I went in to replenish my olive oil. Three years ago, a gallon of the brand I like was $20. Now it is $40, and at least half of that increase happened in the last several months. I expressed shock and alarm. The proprietor assured me that he is making no more money off this price than the old. His markup is the same, just that the supplier has gone way up in price.

“Believe me, I’m not making any money,” he said. “Just the opposite. These prices are killing us too.”

Curious, I found that this olive oil problem is worldwide. It has hit European economies so hard that several nations have removed all sales taxes on olive oil to keep the prices as low as possible. Even so, everyone is feeling the pain. It hits customers but also retailers and suppliers.

What is the cause? You find all sorts of explanations from bad crops to climate change to broken supply chains. But nothing really accounts for it. The real problem is simply inflation, which traces to a fundamental issue: too much money creation via the central banks that has eaten away the purchasing power of the existing money stock. That’s the issue.

Why has the inflation hit olive oil so hard now? That’s the mystery but it is always a puzzling thing in a high-inflation environment why some products and services get hit in different ways than others. The new money enters the economy and moves about in unpredictable ways, creating what the 18th century economist Richard Cantillon called injection effects. You cannot predict what precise form they will take.

For more than three years, the virus of money printing has hit sectors in ways that are shocking and then it goes away only to end up hitting something else. It is like watching a whack-a-mole game in which the stupid thing can pop up anywhere. It hits gas hard and then gas goes down, then hits eggs and it gets better, only to land in cardboard and copper and then go away, but only before it hits utilities, and so on.

This is one reason inflation is so difficult to calculate. It is never uniform. It is sporadic, crazy, and unpredictable. It is now making housing completely unaffordable for anyone in the middle class. Those families that cobble together enough to buy a house for $350K only to find that every contract is outbid by a cash buyer.

Another area hit that is not usually thought of as inflation is financials. For some reason, people are always excited by rising stock prices even though it makes them all more expensive. When the underlying values have not changed, this is only another expression of inflation. Only in this case, people think it is good news not bad. This is really an illusion.

Now to the core point. Is your income up or down? Probably it is up but you are quick to add that everything you buy is up too. Surely you should adjust your sense of personal well-being by an inflation number. But with no real reliable number, this is tricky. You go to your employer and ask for an inflation adjustment but the only one available is that provided by the Bureau of Labor Statistics (BLS).

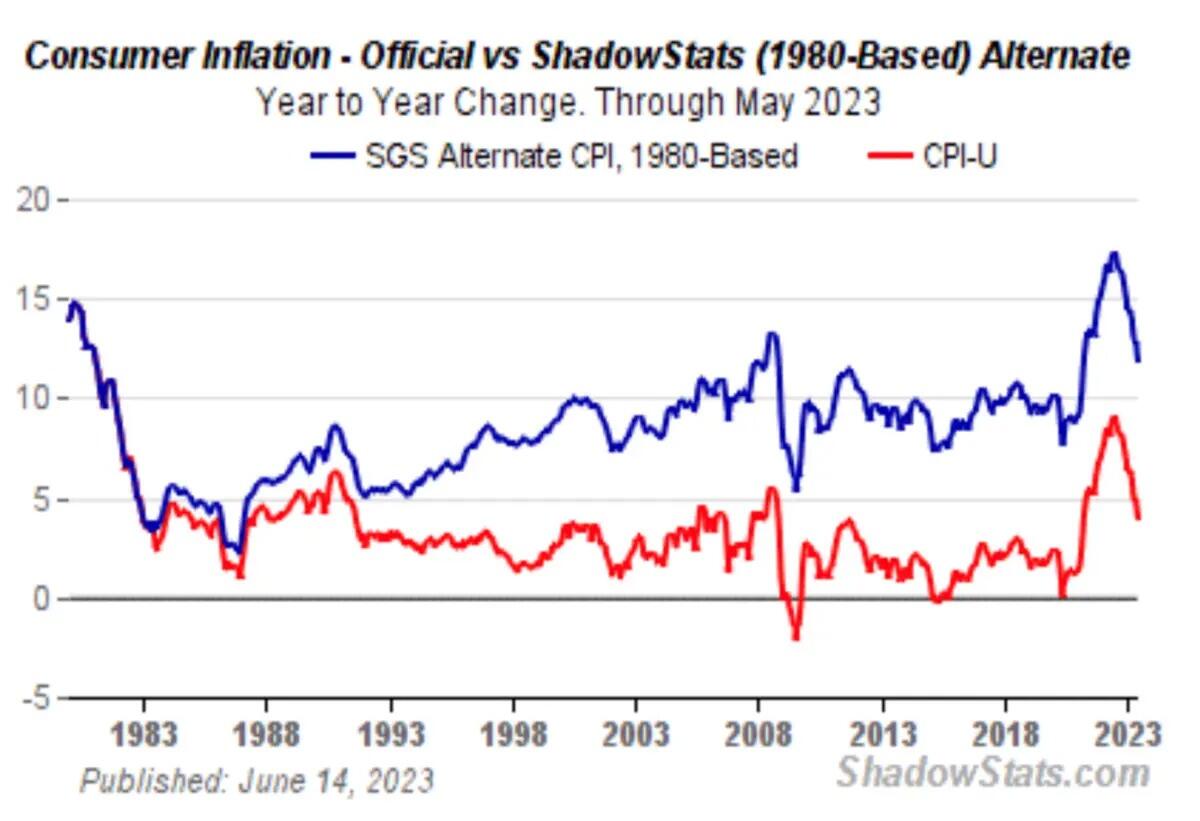

The BLS offers an estimate but it is a weird one. It is subject to vast numbers of “hedonic” adjustments so that an obvious increase can actually be rendered as a decrease because the economists say you are getting a better product or service. The folks at ShadowStats are still calculating inflation the old way and come up with numbers that are consistently double what the government admits.

{kind=link}

ShadowStats seems high but it is likely very low. The exclusions in the Consumer Price Index (CPI) are also notable. The CPI excludes taxes, all interest on everything, most types of insurance, and new forms of fees. It cannot account for vast substitutions in buying nor shrinkflation. It runs housing and rent through a statistical model that is so complicated it cannot be checked for reliability. And the same is true with health insurance, which the BLS says is down over three years, if you can believe it.

These aggressive miscalculations are devastating for people. They are looking for adjustments in their pay but end up with changes that do not come close to matching the real increase in price. But keep in mind that this affects suppliers and businesses too. My friend who runs the grocery store dreads it when employees ask for wage increases because everything else is increasing too.

For example, he had several freezers die on him last week, ruining thousands of dollars of product. Fixing them this time cost nearly twice as much as fixing them last time. Buying new ones would absolutely break the bank. His whole job right now is to keep the company from running too much in the red. It’s not easy.

Notice that suppliers don’t have to beg buyers in order to increase prices to match inflation. The inflation just happens. But when it comes to wages and salaries, it is a different matter entirely. Those increases happen at the discretion of employers, who are loath to boost payments in the midst of a cost squeeze.

There is simply no way that personal income has kept up with inflation over three years. The BLS calculates this using bad inflation statistics and comes up with a flat rate over three years, but still up over 2020. I simply do not believe this is true.

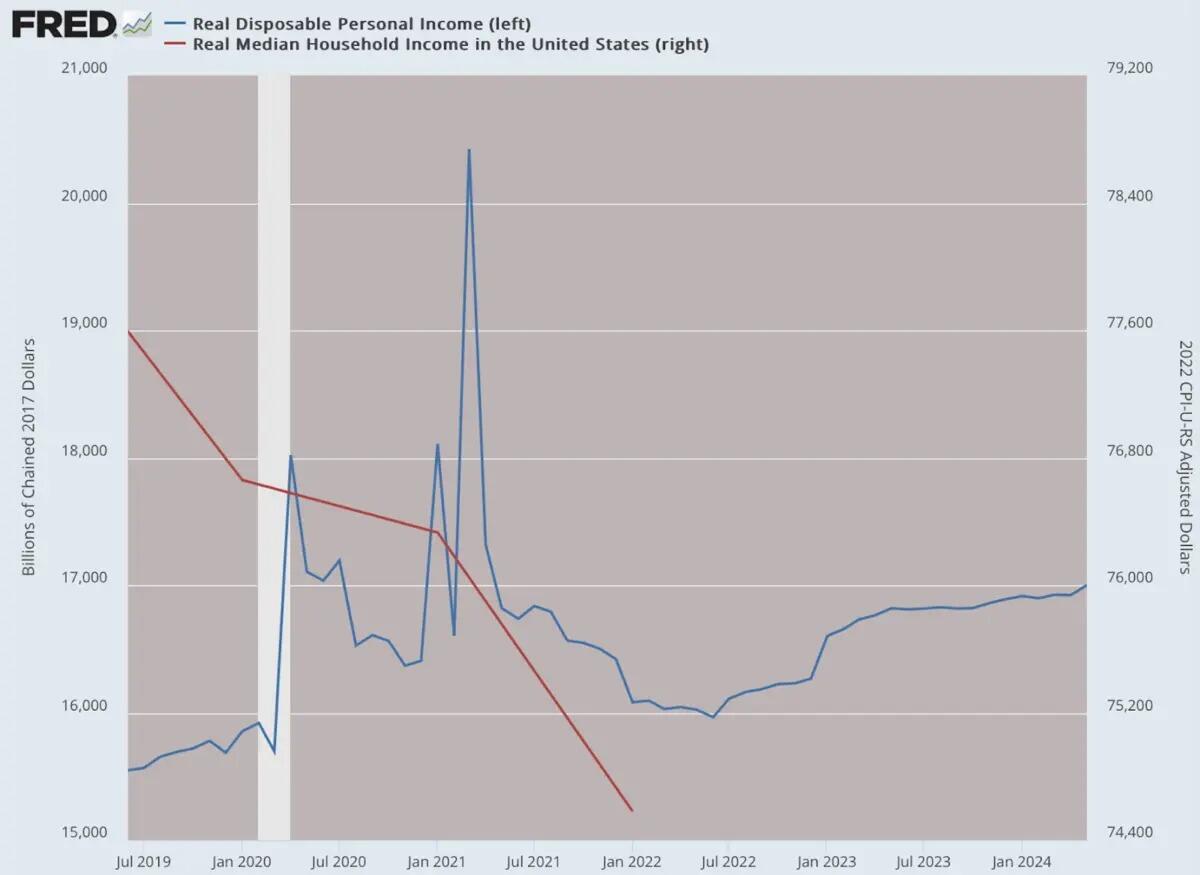

A more accurate trend line comes from the Census Bureau and it is reported only once per year in September. Even with bad CPI data, I feel sure that the results are going to be devastating when they are reported in the fall. The news will be buried as usual.

{kind=link}

(Data: Federal Reserve Economic Data (FRED), St. Louis Fed; Chart: Jeffrey A. Tucker)

So yes, incomes are way down. People keep pressing me to put a number on inflation over three years. Based on everything I can figure out and everything I know, I would estimate it at 35–50 percent since 2021, which is to say that the dollar might have lost half its value. If that is true, we have to adjust output (GDP) accordingly, which puts us as a nation as having lost 13 percent in output since 2020.

Doesn’t that fit more closely with your experience? In other words, we never left recession in 2020. It’s been four years of hard decline with only inflation 401Ks to show for it. This is a realistic understanding of what is happening. As for your own real income, unless you are very lucky to be on the other side of the great wealth transfer, perhaps working at a bond-dealing firm or major financial company, you are experiencing a dramatic decline in your standard of living.

A friend the other day sported a black t-shirt with white letters and the word “Disgruntled.” That pretty much sums up the feeling in the air these days. We are disgruntled with media, government, academia, elites in general, and so many features of the system under which we live that has failed us. Underlying it all, however, is the feeling that we are losing our standard of living. This is the mysterious part because we know it is true and yet official sources keep denying it.

Tyler Durden

Tue, 07/09/2024 – 12:45