42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Bid Despite Macro Meltdown")

Bonds, Bullion, Bitcoin, & Big-Tech (Ex-NVDA) Bid Despite Macro Meltdown

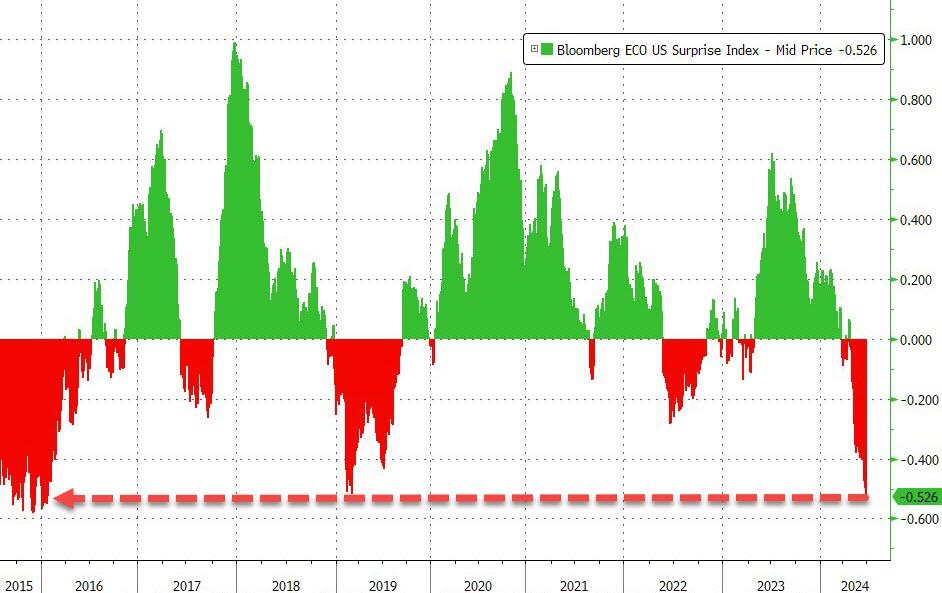

Macro was ugly – really ugly – today: Personal Consumption ugly (Q1 downgraded on 3rd look), continuing jobless claims ugly (highest since Nov 2021), core capital goods new orders and shipments ugly (not a great signals for Q2 GDP), pending home sales ugly (puke to record lows SAAR), and finally, Kansas City Fed manufacturing ugly (21st month in a row without expansion)…

This smashed the US Macro Surprise Index to its weakest since January 2016 (and we have May’s PCE tomorrow)…

{kind=link}

Source: Bloomberg

Micro was not pretty: Micron spooked the AI trade (NVDA lower too)…

{kind=link}

…Consumer weakness exhibited by Walgreens (lowest since 1997)

{kind=link}

…and Levi Strauss (biggest daily drop ever)…

{kind=link}

But Small Caps outperformed strongly on the day, as Nasdaq managed small gains and The Dow and S&P lagged, all just holding green into the close…

{kind=link}

Once again the range in the S&P 500 was very low and realized vol over the last 10 days has dropped to multi-year lows (thanks long gamma and 0-DTE)

{kind=link}

Source: Bloomberg

MAG7 stocks managed gains despite NVDA’s loss…

{kind=link}

Source: Bloomberg

Bank stocks were mixed after the stress tests (GS down on ccard losses, JPM up on strong capital, which ironically they came out and said was too generous)…

{kind=link}

Source: Bloomberg

Bonds were bid across the curve with the belly modestly outperforming (down 3-4bps). Today’s rally pushed 2Y yields lower on the week…

{kind=link}

Source: Bloomberg

The macro was ugly enough to send rate-cut expectations (dovishly) higher on the day…

{kind=link}

Source: Bloomberg

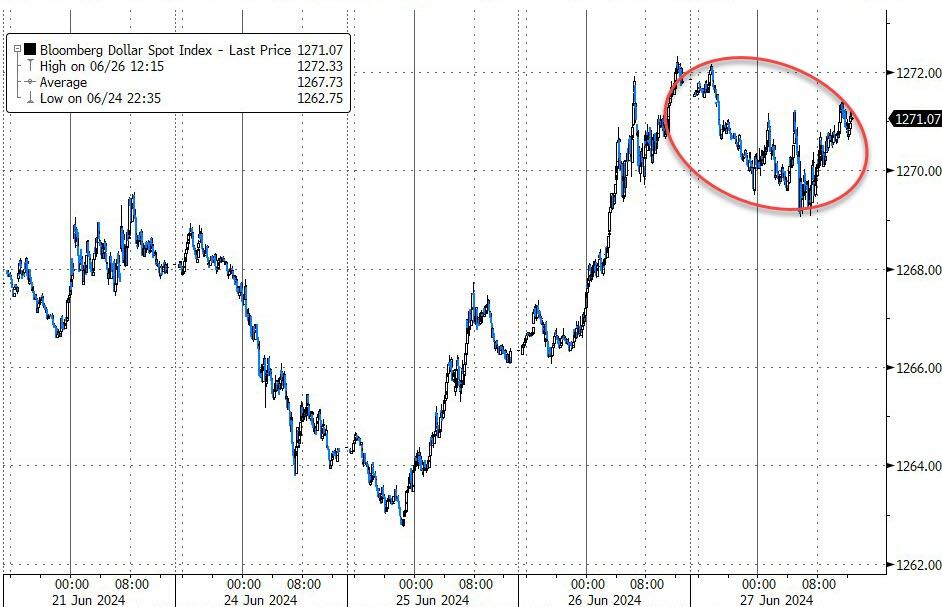

The dollar was flat to slightly lower after yesterday’s yen-driven melt-up…

{kind=link}

Source: Bloomberg

Dollar weakness prompted a rally in gold, finding support at $2300…

{kind=link}

Source: Bloomberg

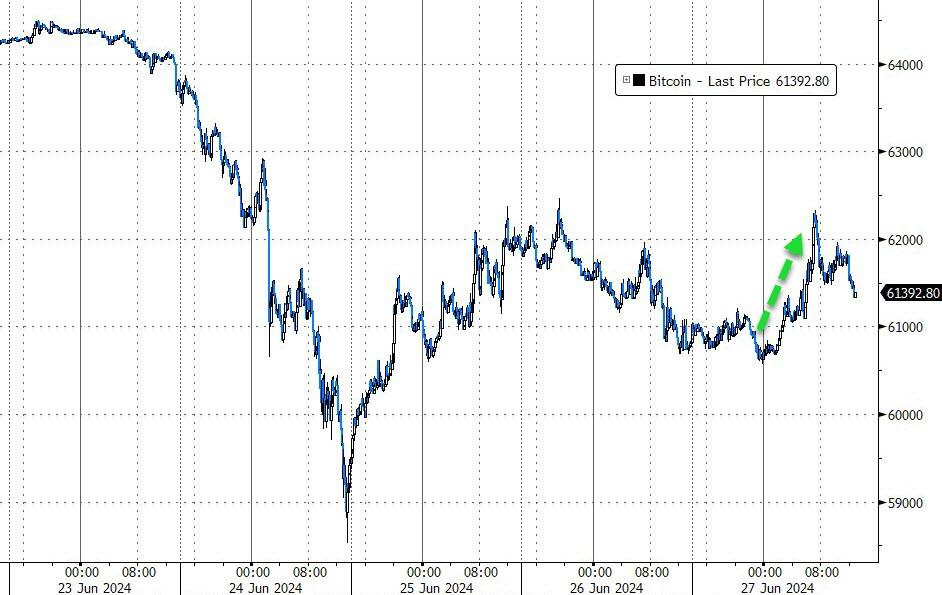

Bitcoin managed to bounce back above $62,000…

{kind=link}

Source: Bloomberg

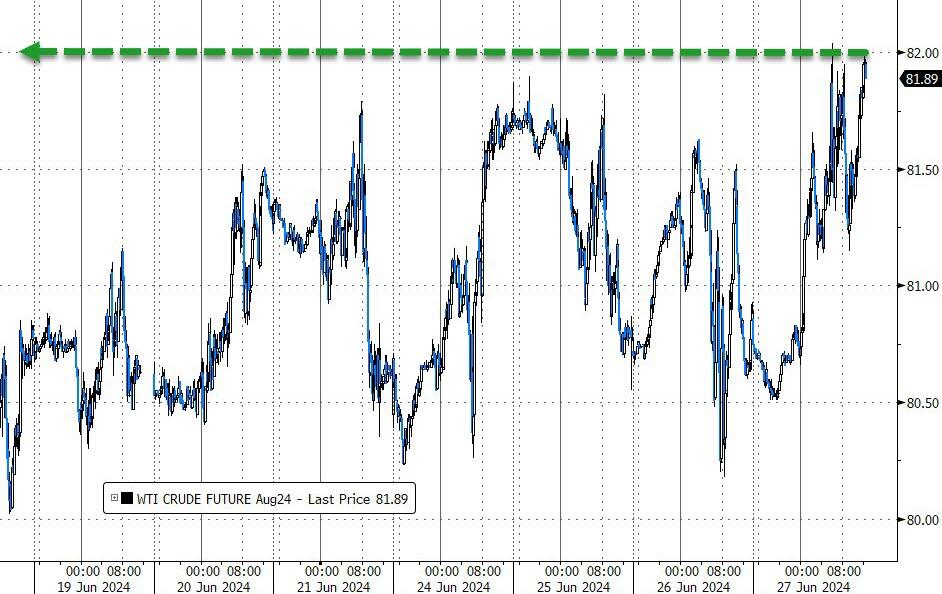

Oil prices rebounded once again, with WTI breaking out above $82, its highest since April…

{kind=link}

Source: Bloomberg

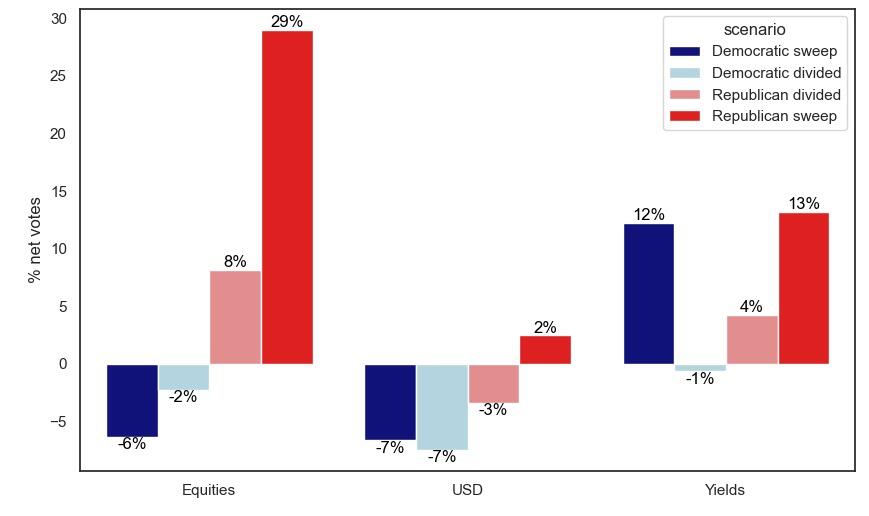

Finally, of course, today was to some extent about positioning for tonight’s debate. Goldman Sachs shows us this chart shows how institutional investors view November’s outcome…

{kind=link}

Source: Goldman Sachs

Simply put, Unified government is a major risk for bonds – Equities most sensitive to a Trump win.

Tyler Durden

Thu, 06/27/2024 – 16:00