42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Global Rally Sputters With US Futures Flat Ahead Of Payrolls

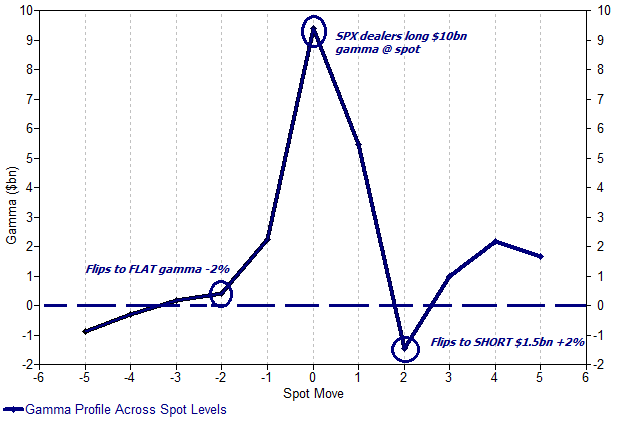

The global stock rally faltered as US equity futures were unchanged for the second day in a row this morning and trading right on top of the “gamma gravity” level of 5350, where as discussed yesterday there is a record $10 billion dealer long gamma pile up which has made the market “stuck” at the strike price.

{kind=link}

As of 7:30am ET, S&P futures are down -0.1%, at session lows after trading in a narrow range all night. Nasdaq futures are a mirror image, trading about 0.1% higher as Mega tech names outperform: GOOGL +27bp, NVDA +13bp, AAPL +12bps. Bond yields are 1-2bp higher this morning, with the OIS forwards sees ~60% prob. of first cut in September. Commodities are mixed: oil/ags are slightly higher this morning reversing an earlier loss. The Bloomberg dollar gauge eased. All eyes on NFP today (preview here): both Goldman (165K) and JPM (150k) are below the Street median estimate of 180k, which suggests we beat.

{kind=link}

In premarket trading, GameStop tumbled after surging as high as $67.5 after hours yesterday when the company confirmed that the latest meltup was another manipulative grift when it filed to sell up to 75 million shares. Tech names outperformed: Micron and Intel rose while tech giants gained (GOOGL +27bp, NVDA +13bp, AAPL +12bps). Here are some other notable premarket movers:

Biomea Fusion shares plunge 61% after the biotech said the FDA had placed a clinical hold on its ongoing Phase I/II trials of BMF-219 in type 1 and type 2 diabetes. Analysts slashed their price targets on the stock.

Braze shares jump 14% after the cloud-based software company boosted its revenue guidance for the full year; the guidance beat the average analyst estimate.

Concrete Pumping shares slide 13%. William Blair analysts cut the rating on the stock to market perform from outperform.

DocuSign shares are down 8.4% after the e-signature company forecast billings for the second quarter that fell short of the average analyst estimate.

Geron shares rise 16% after the biopharmaceutical company secured approval for its blood disorder drug named Rytelo from the FDA.

Lyft shares gain 3.5% after Loop Capital lifted its rating on the ride-hailing firm, citing a positive investor day and recent stock retreat.

Samsara shares fall 6.2% despite the application software company reporting first-quarter results that beat expectations and raising its full-year forecast.

Vail Resorts shares slump 8.5% after the ski resort operator cut its full-year Ebitda outlook. The guidance missed the average analyst estimate.

With traders wary of placing big bets either way ahead of the payrolls report, global stocks are on track to snap a two-week losing stretch. Rate-cut expectations have escalated in the past week, encouraged by a slew of weaker-than-forecast US data, as well as easing by the Bank of Canada and ECB. A Bloomberg gauge of global government bonds posted its longest rising streak since November.

“All focus on the payrolls and the potential aftermath,” said Michael Brown, senior strategist at Pepperstone Group Ltd. “A number that’s bang in line with expectations will reaffirm where current market pricing is for Fed cuts and could give the market the fuel it needs to keep moving higher.”

As previewed earlier, Friday’s report is expected to show the US added 180,000 jobs in May, slightly more than in April, with the unemployment rate seen holding steady. Swap markets are pricing a full Fed rate cut by November, with a strong likelihood of one in September. In its preview, Goldman’s trading desk wrote that the set up into the print remains favorable for stocks (“I have goldilocks zone in the low 100s as stocks continue to cheer for a palatable slowdown”), and provided the following trading framework:

<50k S&P + 50bps

50k – 100k S&P +75 – 100bps

100k – 150k S&P +100bps

150k – 200k S&P + / – 50bps

200k – 250k S&P -50bps

250k – 300k S&P -75bps

>300k S&P sells off more than 100bps

Meanwhile, as bond yields drop and as rate-cut bets build, investors are pouring money into stocks, with US equity funds getting $4.6 billion in a seventh week of inflows, BofA’s Michael Hartnett said, although the strategist warned a Fed rate cut may not be entirely good news, calling it the “first hint of trouble.” Chances of a hard landing could increase if the market grows more confident of lower borrowing costs, he added.

European stocks and bonds fall after several ECB policymakers offered wary assessments of the possibility of future interest-rate cuts. The move lower extended after the ECB’s preferred measure of pay showed acceleration at the start of 2024. The Stoxx 600 is down 0.4% with technology and retail stocks the biggest outperformers, while property and insurance stocks lagged, given the ECB’s signal that it wouldn’t rush additional rate cuts. Here are the biggest movers Friday;

ING Groep NV shares rise as much as 1.5% after Barclays upgrades the Dutch lender to overweight from equal-weight, with models pointing to €7.5 billion more in buybacks before the end of next year

Bellway shares rise as much as 2.1% after it delivered an upbeat trading update that shows the UK housebuilder on track to build 7,500 homes this year at a higher selling price than previously expected

Tecnicas Reunidas climbed as much as 8.9% after Oddo BHF raised the recommendation on the Spanish company to outperform from neutral as risk/reward profile seen attractive.

Daimler Truck drops as much as 2.5%, Volvo -2.4% after Citi says it has been a “roller coaster” for truck stocks this year, as it opens 90-day downside catalyst watches on the two companies with likely weaker orders and margins set to drive downgrades

Rexel shares fall as much as 3.4% to hit a one-month low after the French provider of electrical supplies released new and upgraded medium-term financial targets ahead of a capital markets day on Friday

Arcadis NV shares slip as much as 3.5% after the Dutch engineering firm is downgraded to accumulate from buy at KBC Securities, which highlights an absence of “substantial” short-term triggers for the stock

Burckhardt Compression declines as much as 6.1%, snapping four days of gains, as Baader Helvea downgrades to reduce from add, saying it’s time to take profits with shares of the piston compressor manufacturer having surged to record highs

C&C shares fall as much as 13% after the UK alcoholic beverage manufacturer announced an €150 million impairment charge and as CEO Patrick McMahon has resigned due to previously disclosed accounting adjustments.

Earlier, Asian stocks gained, set for their best week in three weeks, as a rally in South Korean shares tempered losses in most other markets. The MSCI Asia Pacific Index rose as much as 0.4%. South Korean equities were among the biggest advancers on the regional gauge after the market reopened from a holiday. The country’s stock markets were supported by foreign buying of local chipmakers. Indian shares also climbed, as the central bank held its benchmark interest rate while tweaking growth projection higher. Chinese stocks declined for the third straight session, with stronger-than-expected exports for May failing to boost sentiment. There are also concerns that a growing backlash among trade partners would dent overseas demand even as consumer spending remained weak at home.

While “we are constructive on Asia markets,” the second half has risks including a stronger dollar, geopolitical uncertainty and possible volatility around the US elections, Timothy Moe, an Asia equity strategist at Goldman Sachs Group Inc., told Bloomberg TV.

In FX, the Bloomberg Dollar Spot Index was little changed with focus on the US non-farm payrolls data, which is expected to show a steady unemployment rate and 180k jobs added in May, according to a Bloomberg survey of economists

USD/JPY dropped as much as 0.3% before paring to trade unchanged at 155.59; Japanese Minister of Finance Shunichi Suzuki said authorities should resort to currency intervention only on a limited basis

GBP/USD steadied around 1.28; Data showed the UK housing market extended its stagnation in May, a measure of property values fell 0.1% after no change the month before

EUR/USD was little changed at 1.09; The ECB’s preferred measure of euro-zone pay showed acceleration at the start of 2024

In rates, Treasuries dipped ahead of the jobs report, with US 10-year yields rising 1bps to 4.30%. German 10-year yields rise 3bps to 2.58%.

In commodity markets, gold prices fell after the People’s Bank of China said it hadn’t added to its bullion holdings last month, pausing an 18-month long buying spree that lifted the precious metal to record highs. Brent crude futures edged up, but were set for a third weekly loss. Spot gold fell ~$37 to around $2,338 after data showed the Chinese central bank halted gold purchases in May.

Today’s focus will be on the payrolls report at 8:30am; data also includes April wholesale trade sales (10am), 1Q household change in net worth (12pm) and April consumer credit (3pm). Fed officials are expected to refrain from commenting until after their June 12 policy announcement

Market Snapshot

S&P 500 futures little changed at 5,366.75

STOXX Europe 600 down 0.1% to 523.93

MXAP up 0.3% to 180.71

MXAPJ up 0.3% to 563.66

Nikkei little changed at 38,683.93

Topix little changed at 2,755.03

Hang Seng Index down 0.6% to 18,366.95

Shanghai Composite little changed at 3,051.28

Sensex up 1.8% to 76,403.28

Australia S&P/ASX 200 up 0.5% to 7,860.02

Kospi up 1.2% to 2,722.67

German 10Y yield little changed at 2.56%

Euro little changed at $1.0890

Brent Futures down 0.4% to $79.59/bbl

Gold spot down 1.0% to $2,351.54

US Dollar Index little changed at 104.10

Top Overnight News

Japan’s largest banks plan to sell 1.32 trillion yen ($8.5 billion) of Toyota shares, people familiar said, the strongest sign yet that the country’s big businesses are serious about unwinding their cross-shareholdings. BBG

China’s May exports beat expectations, climbing 7.6% in dollar terms from a year earlier. Still, Bloomberg Economics said the lift from firmer overseas demand probably won’t be enough to offset domestic weakness, which showed through in May’s unexpectedly weak import growth of 1.8%. BBG

China halts its 18-month gold purchase spree (the PBOC didn’t purchase any gold last month, the first time it hasn’t done so since Oct ’22). BBG

The ECB’s preferred measure of euro-zone pay showed acceleration at the start of 2024, in the latest sign that price pressures in the region are proving stubborn. Compensation per employee rose by 5.1% from a year ago in the first quarter, up from a revised 4.9% in the previous three months, ECB data showed Friday. That exceeded a Bloomberg Economics forecast of 4.6%. BBG

The European Commission has recommended that the EU start accession talks with Ukraine this month, in an effort to signal support to the war-torn country before Budapest takes over the rotating presidency of the bloc, according to people familiar with the matter. FT

The estimated $4.6 trillion cost of extending expiring portions of Donald Trump’s 2017 tax cuts isn’t damping Republican enthusiasm for renewal next year. However, this time the nation’s debt load and interest costs are heavier burdens, requiring unprecedented budget pain to offset the lost revenue. BBG

Moody’s warns 6 regional banks, including FRME (First Merchants), FNB (F.N.B Corp.), FULT (Fulton Financial), ONB (Old National), PGC (Peapack-Gladstone), and WAFD (WaFd), are at risk of being downgraded over their CRE exposure. BBG

A risky style of trading is roaring back in popularity, driven by amateur traders who call themselves “degens” and pile into long-shot trades that proudly have nothing to do with conventional ways of assessing investments. Some are flinging cash at specific stocks or cryptocurrencies just to be part of a movement. Others are sticking around for the jokes and memes. Degens are part of the fuel for meme-stock mania, like the logic-defying action in GameStop shares in recent weeks. When these internet-fueled traders stick together, they have the potential to spark wild swings in assets. All it takes is for a meme to catch fire. WSJ

A federal judge in San Francisco dismissed a proposed class action against Google (GOOG), which had alleged the company misused personal and copyrighted data to train its AI systems, including its Bard chatbot, according to Reuters.

South African ANC Leader Ramaphosa said they have agreed that they will invite parties to form a government of national unity, according to Reuters.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed in cautious and tentative trade and macro newsflow on the quieter side ahead of the US jobs report. ASX 200 was kept afloat by gains in gold miners, alongside Resources and Materials names. while Real Estate and Healthcare lagged. Nikkei 225 was subdued following softer-than-expected household spending data. On an index level, gains in Pharma and Mining failed to counter the downside from Banking and Autos, with the latter continuing to feel the woes from its domestic safety scandal. Hang Seng and Shanghai Comp both dipped into the red after opening modestly firmer, whilst CATL shares tumbled some 7% after US lawmakers said Chinese EV battery manufacturers rely on forced labour and should be blocked from importing goods into the US. No reaction was seen on the Chinese trade data.

Top Asian News

Japanese Foreign Reserves USD 1.2316tln at end-May (vs USD 1.2790tln at end-April), according to MOF. “Japan’s holdings of foreign securities dropped sharply in May, indicating that the government likely financed most of its recent record currency market intervention by selling Treasuries and other foreign securities and still has ample firepower to step into markets again.” – via Bloomberg.

Japanese Finance Minister Suzuki said the drop in Japan’s foreign reserves as of end-May partially reflects FX intervention; and will take action against excessive forex moves. Forex intervention was conducted to address excessive moves. Forex intervention should be done in a restrained manner. Not taking into account the limit to reserves for forex intervention.

BoJ offered to buy JPY 150bln in up to 1yr JGBs, JPY 375bln in 1-3yr JGBs, JPY 425bln in 5-10yr JGBs and JPY 150bln in 10yr-25yr JGBs; all unchanged.

PBoC injected CNY 2bln via 7-day reverse repos with the rate at 1.80%.

RBI maintained its Repo Rate at 6.50% as expected and maintained its policy stance as expected. FY25 real GDP growth was upgraded to 7.2% vs 7% previously. RBI Chief said risks to growth and inflation are evenly balanced and the RBI will remain resolute in commitment to aligning inflation to target.

TSMC (TSM / 2330 TT) May Sales TWD 229.6bln, +30.06% Y/Y

BoJ may drop clue on bond tapering plans next week, via Reuters citing sources; there is no consensus yet. Could trim monthly purchases or clarify plans to proceed with a slow but steady taper, according to the sources.The decision could be delayed if the bond market becomes too volatile. Focus would be to avoid abut spikes in yields.

China extends anti-dumping duties on the imports of some chemicals from India for a five-year period as of 8th June.

European bourses, Stoxx 600 (-0.2%) began the session on a tentative footing, in what was initially directionless trade. However, as the morning progressed, sentiment quickly waned and stocks trundled lower to session lows, where they currently reside. European sectors hold a negative bias, and with the breadth of the market fairly narrow. Tech takes the spot, continuing to build on the past week’s outperformance. Real Estate is found at the foot of the pile after Morgan Stanley downgraded Vonovia (-3.7%) and Leg Immobilien (-3.8%). US Equity Futures (ES U/C, NQ +0.1%, RTY U/C) are mixed and with trade tentative ahead of today’s US employment report, where expectations are for the headline to tick higher to 185k from 175k.

Top European News

German Economy Minister says if things go well will have 1-1.5% growth next year.

ECB Speakers

ECB’s Kazaks says victory over inflation is not yet on hand; any further rate cuts should be gradual; the next steps are data dependent and will be meeting by meeting, via Bloomberg.

ECB’s Muller says they need to be cautious when making decisions and should not be in a rush to cut.

ECB’s Nagel says ECB policy is not on auto pilot when it comes to rate cuts; inflation is proving to be stubborn, especially in the case of services. Negotiated wages are expected to rise particularly sharply this year and continue to see strong growth thereafter. The decision to cut was logical, tendency is there that inflation is going down. Decision to cut was not premature. Still acting restrictively despite lowered rates. Not on autopilot, will look at the data and make a decision at each meeting. Says “well on the way” when it comes to the balance sheet reduction

ECB’s Vasle says cannot predetermine path of ECB interest rates.

ECB’s Simkus says more than one cut this year is a possibility. Data clearly show disinflation and inflation returning to target but the road is bumpy.

ECB’s de Guindos says inflation will be around 2% next year, sees huge uncertainties on the economy.

ECB’s Rehn says inflation will continue to decline, rate cuts will also bolster the economies recovery.

ECB’s de Guindos says sometimes in order to attain cross-border merger, need to engage with national consolidation first.

ECB’s Makhlouf says unsure how fast the ECB will carry on with rate reductions, or if at all.

ECB’s Schanbel says the lack of fiscal consolidation, despite high debt levels may impede monetary policy and heighten the risk of fiscal dominance.

ECB’s Holzmann says “my decision on rates was based on the latest data and forecasts; fight against inflation is not over yet”. “Currently I see little risk of a second inflation wave but inflation is stickier than expected”.

FX

USD is steady vs. peers ahead of the crucial jobs report due at 13:30BST. Levels to the downside for DXY include; 103.99 a double bottom from overnight and Tuesday. To the upside, focus remains on whether the index can move beyond its 200 and 100DMAs at 104.40 and 104.43 respectively.

EUR is flat vs. the USD as the dust settles on yesterday’s ECB rate cut, and unreactive to the slew of ECB speakers today. As it stands, the next 25bps reduction is not fully priced in until December. Upside for EUR/USD sees the 1.09 mark.

GBP is flat against both USD and EUR. Cable remains within yesterday’s 1.2763-1.2809 range, which could be tested by the upcoming NFP release. Tuesday’s 1.2818 high was the highest since March 14th.

JPY is the marginal outperformer vs the Dollar, currently within a 155.13-93 range. NFP could prove an inflection point for the pair ahead of BoJ next week.

Antipodeans are both steady vs. the USD in quiet newsflow with not much follow-through from Chinese trade data overnight. AUD/USD for now is contained within yesterday’s 0.6633-83 range with the pair having traded on a 0.66 handle all week.

PBoC sets USD/CNY mid-point at 7.1106 vs exp. 7.2430 (prev. 7.1108)

Fixed Income

USTs are marginally in the red, with no real reaction to the morning’s data points or extensive ECB speak. Focus entirely on payrolls before CPI and the FOMC next Wednesday; USTs in narrow 110-06 to 110-10 bounds which are entirely contained by Thursday’s 110-03 to 110-13 parameters.

Bunds is softer, weighed on by the softer than expected German Industrial Output data, though were unreactive to the extensive number of ECB officials this morning; speak for the most part stuck with the party script of meeting-by-meeting and data-dependency; Bunds were essentially unchanged and at the top-end of initial 130.78-131.05 parameters but dipped to a 130.65 base on the latest EZ Q1 wage number; ECB’s Q1 Key wage indicator accelerated to 5.1% Y/Y vs. prev. 4.9% (Q4’23)

Gilts are rangebound and unreactive to the morning’s Halifax House Price data which unexpectedly declined on the month, though the note described this as essentially unchanged.

Commodities

Crude benchmarks are marginally in the red but have essentially been pivoting the unchanged mark in limited APAC/European trade ahead of the NFP print. Brent currently around USD 79.80/bbl.

Precious metals were relatively contained but tumbled on the release of China’s monthly gold reserves which showed they were maintained at 72.8mln/oz. XAU slipped from USD 2373/oz to USD 2358/oz over the course of five minutes; thereafter, tumbled further to a USD 2342/oz fresh low for the session.

Base metals are entirely in the red, with sentiment hit following the Chinese gold reserves headline.

Chinese gold reserves 72.8mln/oz vs. prev. 72.8mln/oz; The maintained figure for the China gold reserves seemingly breaks the 18-month streak of purchases for the yellow metal.

Chinese May iron ore imports 102.03mln tons (vs 101.82mln tons in April) Jan-May iron ore imports +7% Y/Y.

Chinese May crude oil imports 46.97mln metric tons (vs 44.72mln tons in April); Jan-May crude oil imports -0.4% Y/Y.

SPDR Gold Trust GLD reports holdings up 0.4% to 837.10 tonnes by June 6th.

Chile’s state-run Codelco is said to be looking for partners on a major new lithium project slated to begin production in 2030, according to documents cited by Reuters.

Goldman Sachs said, “Even assuming comfortable European end-October 2024 storage, we still see winter global gas price risks skewed to the upside, led by TTF.”

Natural gas flow has restarted from the UK to Norway via Langeled pipeline, according to UK national gas data.

Geopolitics

Hamas reportedly said that it will reject the Israeli ceasefire proposal, arguing that the proposal does not ensure a permanent end to hostilities. Hamas will continue to reject proposals until it secures a “permanent ceasefire”, via Critical Threat on X

Israeli PM Netanhayu is to address US Congress on July 24th, according to Punchbowl’s Sherman. However, Times of Israel sources suggested July 27th.

US military said it destroyed eight Houthi drones and two Houthi uncrewed surface vessels in the Red Sea, according to Reuters.

Philippine Coast Guard reports that the Chinese Coast Guard intentionally rammed a Philippine Navy rubber boat transporting sick personnel, according to Reuters.

US Event Calendar

08:30: May Change in Nonfarm Payrolls, est. 180,000, prior 175,000

May Change in Private Payrolls, est. 165,000, prior 167,000

May Change in Manufact. Payrolls, est. 5,000, prior 8,000

May Unemployment Rate, est. 3.9%, prior 3.9%

May Underemployment Rate, prior 7.4%

May Labor Force Participation Rate, est. 62.7%, prior 62.7%

May Average Hourly Earnings MoM, est. 0.3%, prior 0.2%

May Average Hourly Earnings YoY, est. 3.9%, prior 3.9%

May Average Weekly Hours All Emplo, est. 34.3, prior 34.3

10:00: April Wholesale Trade Sales MoM, est. 0.5%, prior -1.3%

April Wholesale Inventories MoM, est. 0.2%, prior 0.2%

12:00: 1Q US Household Change in Net Wor, prior $4.84t

15:00: April Consumer Credit, est. $10b, prior $6.27b

DB’s Jim Reid concludes the overnight wrap

For markets, it was another day of milestones yesterday, with the ECB becoming the latest central bank to cut rates this cycle. They announced a 25bp cut in their deposit rate to 3.75%, which is the first cut they’ve delivered since 2019. And even though the tone was a bit hawkish in several respects, it now makes them the fourth G10 central bank to have cut rates, after Canada, Sweden and Switzerland . In turn, the move has cemented the idea that the global monetary policy cycle is moving towards an easing mode, with investors expecting further cuts on the horizon. So it marks a big shift from much of the last couple of years, when central banks were rapidly hiking rates to try to bring down inflation.

In terms of the ECB’s decision, the rate cut itself was widely expected, so didn’t come as much surprise to markets. But there were several aspects of the decision that leant in a hawkish direction. For instance, they took out the line from the last statement that “ it would be appropriate to reduce the current level of monetary policy restriction ” if their confidence grew that inflation was returning to target. Moreover, they actually upgraded their inflation forecasts, with 2024 revised up by two-tenths to 2.5%, and 2025 also up two-tenths to 2.2%. On top of that, in the press conference President Lagarde said, “Are we today moving into a dialing back phase? I wouldn’t volunteer that”. So investors grew more sceptical that this would kick off a rapid series of rate cuts.

The rate cut was supported by all but one of the ECB’s Governing Council and our European economists observe that garnering the support of most hawks came at the cost of a clear signal on the direction of travel. An implicit easing bias persists, but recent data did not give the ECB the collective confidence to present the move as the first in a series of cuts. Our economists maintain a baseline view of two more rate cuts this year (in September and December), but with a September cut not being a done deal. See their full reaction here.

This hawkish leaning was echoed in markets, and sovereign bond yields rose across the Euro Area after yesterday’s decision. By the close, yields on 10yr bunds (+3.8bps), OATs (+4.3bps) and BTPs (+4.7bps) had all moved higher, and the Euro also strengthened after the decision, ending the day up +0.17% at $1.088. Looking forward, overnight index swaps see a July cut as in the balance, with a 38% chance of a cut priced in as we go to press this morning. But a cut by September is still seen as more likely than not, with the chance of a cut by that meeting at 91%.

Looking forward, attention will now turn to the US jobs report for May, which comes at an important point ahead of the Fed’s decision on Wednesday. This report could see an important milestone, as i f the unemployment rate stays beneath 4%, then it would mark the longest stretch of sub-4% unemployment for the US since the early 1950s, at 28 months. Indeed, we pointed out several parallels with the early 1950s earlier this week (link here), including a strong performance for risk assets, a temporary burst of inflation, and heightened geopolitical risks.

When it comes to today’s report, our US economists are looking for nonfarm payrolls to come in at +200k, which would be an uptick from April, when nonfarm payrolls growth was at a 6-month low of +175k. Otherwise, they see the unemployment rate holding steady at 3.9%, and average hourly earnings ticking back up a tenth to +0.3%. See their full preview and how to sign up to their webinar afterwards here.

Ahead of the jobs report, the US weekly initial jobless claims were a bit weaker than expected yesterday, rising to 229k over the week ending June 1 (vs. 220k expected). That’s a 4-week high, but some of the other economic news was more positive. Indeed, the Atlanta Fed’s GDPNow estimate for Q2 was upgraded again to an annualised rate of 2.6%. We also had data yesterday showing the US trade deficit was a bit smaller than expected in April, at $74.6bn (vs. $76.5bn expected), even if the number was still the highest since October 2022.

US equities saw little change against that backdrop, with the S&P 500 (-0.02%) narrowly ending a run of four consecutive gains and coming off of its record high the previous day. Small-caps underperformed, with the Russell 2000 down -0.70%, whereas the Magnificent 7 saw a slight gain (+0.19%) that left it at another all-time high. European equities posted a relatively stronger performance though, with the STOXX 600 (+0.66%) closing just shy of its record high from mid-May. In the meantime, US Treasuries posted marginal losses with the 10yr yield up +1.2bps to 4.29%, whilst the 10yr real yield (+2.9bps) ticked back up above 2% again. Overnight that trend has continued, with the 10yr Treasury yield up a further +1.0bps to 4.30% as we go to press.

In the commodity space, oil prices continued to recover some of the c. 5% decline seen earlier in the week after the weekend’s OPEC+ agreement to begin phasing out production cuts from October. Brent crude was up +1.86% to $79.87/bbl, its largest daily advance since March, supported by comments from OPEC+ ministers that production changes could be paused or reversed if needed. That trend has continued overnight, with Brent crude up another +0.20% to $80.03/bbl.

Overnight in Asia, equity markets have put in a mixed performance as investors focus on the upcoming US jobs report. Several indices have lost ground, including the Nikkei (-0.19%), the Shanghai Comp (-0.23%), the Hang Seng (-0.42%), and the CSI 300 (-0.72%). However, the KOSPI (+0.94%) has advanced after returning from a public holiday, and US equity futures are also pointing in a positive direction, with those on the S&P 500 up +0.10%. Separately, data showed that China’s exports grew by more than expected in May, with a year-on-year increase of +7.6% (vs. +5.7% expected). Imports also grew by less than expected, with a year-on-year growth increase of +1.8% (vs. +4.3% expected).

To the day ahead now, and data releases include the US jobs report for May and German industrial production for April. From central banks, we’ll hear from ECB President Lagarde, and the ECB’s Nagel, Simkus, Holzmann, Schnabel and Centeno, along with the Fed’s Cook.

Tyler Durden

Fri, 06/07/2024 – 08:10