42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

A Second-Quarter Recession This Year Looks Increasingly Likely

Authored by Mike Shedlock via MishTalk.com,

As I watch the evolution of consumer spending, housing starts, new home sales, and GDPNow trends, it appears the economy has peaked. Warning: I tend to be early.

{kind=link}

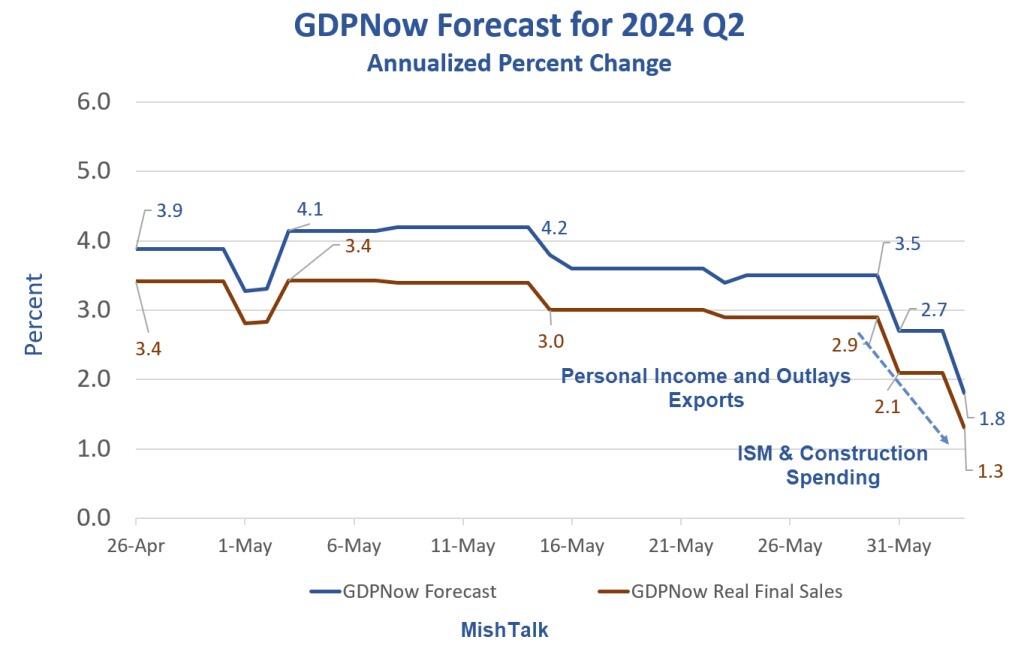

GDPNow forecast from the Atlanta Fed as of 2024-06-03. Chart by Mish

The GDPNow forecast has been weakening since a peak of 4.2 percent on May 8, 2024.

The best number to follow is not the overall forecast but rather Real Final Sales (RFS). The rest is inventory adjustment that nets to zero over time.

A steep plunge occurred in the base forecast from 3.5 to 2.7 then to 1.8 on May 1 and June 3. Importantly, RFS fell from 2.9 to 2.1 to 1.8 on the same dates.

Balance of Trade

This rates to smack GDPNow https://t.co/47ghxVTC2z

— Mike “Mish” Shedlock (@MishGEA) May 30, 2024

I made that call on May 30.

On June 1, I commented Soaring US Trade Deficit Smacks the Atlanta Fed GDPNow Forecast

On June 3, the GDPNow forecast took another dive.

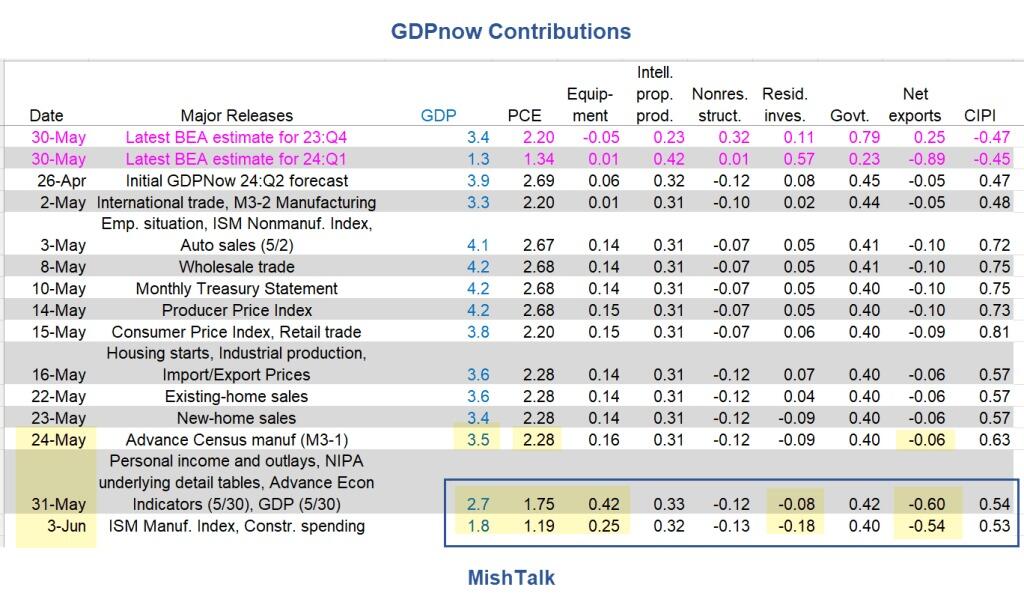

The following table that shows both moves.

GDPnow Contributions

{kind=link}

Advance Economic Indicators, specifically import-export data took the Net Exports contribution to GDP from -0.06 to -0.60 on May 31.

Also on May 31, Personal Income and Outlays took the contribution for Personal Consumption Expenditures (PCE) from 2.28 to 1.75.

It’s not always easy to assign the numbers to specific buckets, but the plunge in net exports is clear.

ISM Manufacturing New Orders and Backlogs in Steep Contraction

{kind=link}

ISM chart and excerpts below by permission from the Institute for Supply Management® ISM®

On June 3, I commented ISM Manufacturing New Orders and Backlogs in Steep Contraction

The Manufacturing ISM was in contraction for 16 months went positive for a month and is contracting again for two months with order backlogs falling for 20 months.

June 3 Impact to GDPNow

On June 3, the ISM and construction spending reports clobbered PCE with lesser negative impacts on Residential Investments, Equipment, and Net Exports.

Assigning percentages here is more difficult, and the Atlanta Fed might not be able to do so either. This is because the variables are entered at the same time and one can influence another.

However, the decline in Residential Investment from -0.08 to -0.18 is easy to attribute to the construction spending report. The big declines from 1.75 to 1.19 on PCE and 0.42 to 0.25 on equipment are harder to attribute precisely.

It’s important to note that what matters is not the reports but what GDPNow expected vs the reports. Bad data does not necessarily cause a decline in GDPnow, nor good data a rise.

Below Stall Speed

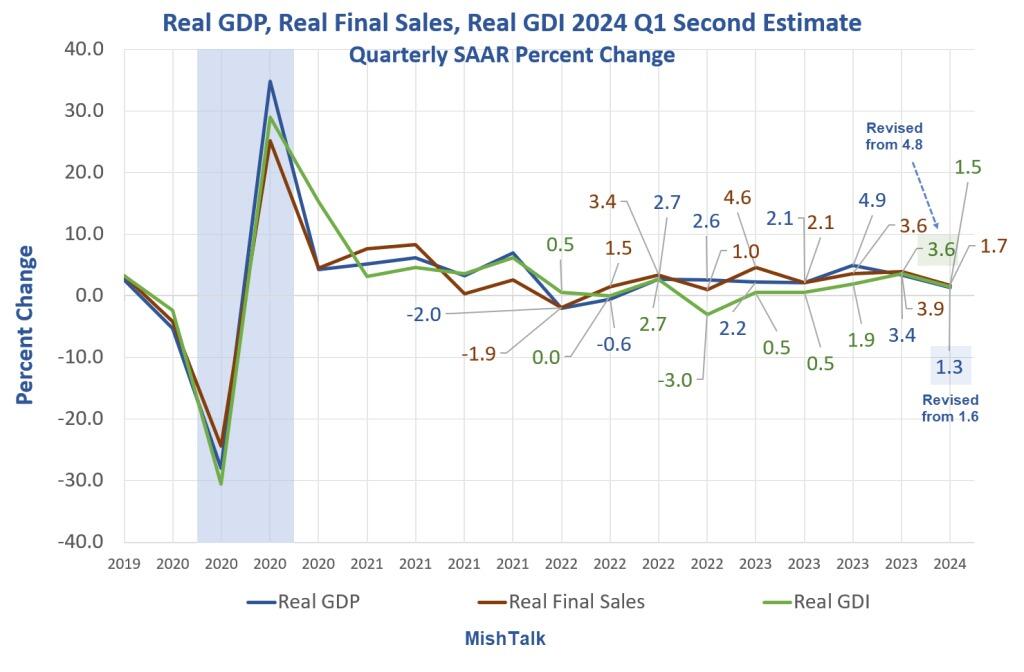

With Real Final Sales at 1.3 percent (lead chart) the economy is at stall speed. But will we stay there?

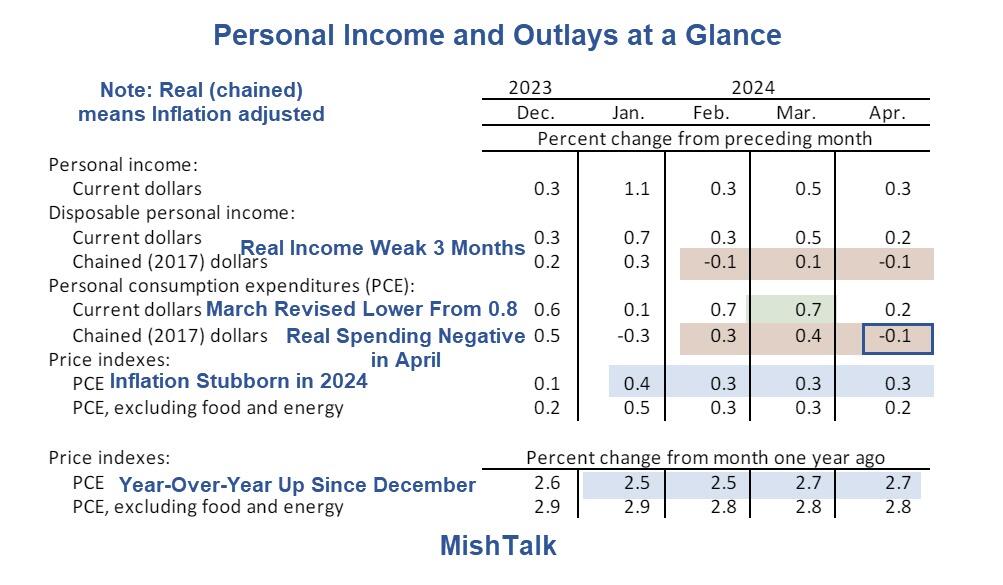

Real (inflation-adjusted) Income and spending was negative in April. Real income was negative two of the last 3 months.

{kind=link}

Chart from the BEA, annotations by Mish

For discussion of the above chart, please see The Fed’s Preferred Inflation Measure, PCE, Shows No Further Progress

Real (inflation-adjusted) Income and spending was negative in April. Real income was negative two of the last 3 months.

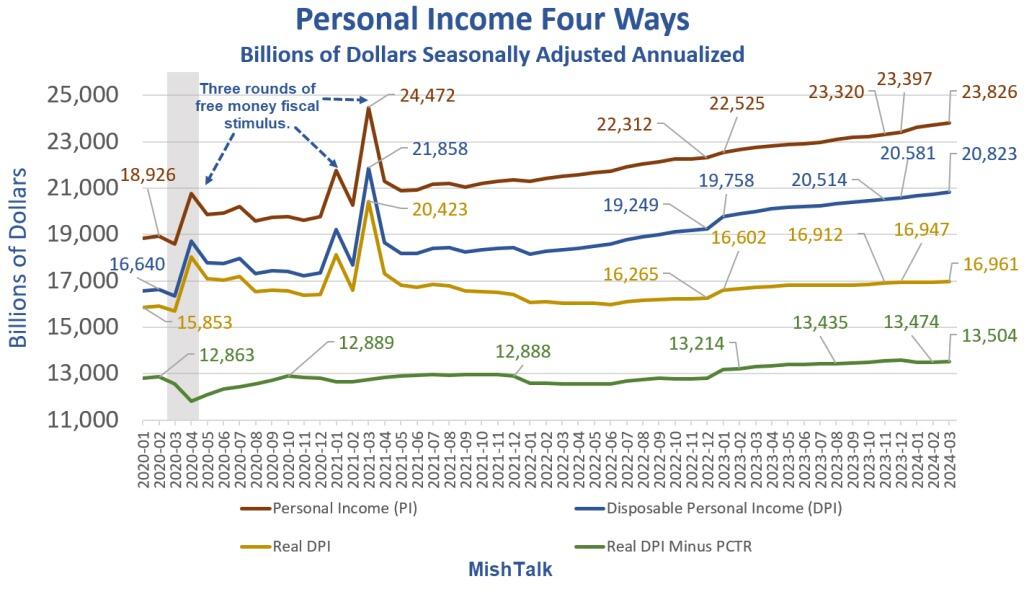

Personal Income Four Ways

{kind=link}

Real Disposable Personal Income (after taxes) has stalled.

For discussion, please see Why Consumers Are Angry About the Economy in Five Pictures

Anger Synopsis

Consumers are angry, and it’s reflected in the polls. I have been discussing the reasons for angry consumers all year.

But Biden and most economists still don’t get it. They think the economy is doing well. Tell that to renters looking to buy a home, stuck with rent going up month after month.

More Soft Economic Data, Q1 GDP Revised Lower, Q4 GDI Significantly Lower

{kind=link}

GDP and GDI data from BEA, chart by Mish

On May 30, I commented More Soft Economic Data, Q1 GDP Revised Lower, Q4 GDI Significantly Lower

The economic slowdown continues led by income and consumer spending.

The same story is repeating in April.

Revisions a Hallmark of Economic Turns

May 24: Another Massive Revision, This Time Durable Goods, What’s Going On

May 23: New Home Sales Sink 4.7 Percent on Top of Huge Negative Revisions

May 22: Discretionary Spending Tumbles at Target, Shares Drop 10 Percent

May 22: Existing-Home Sales Decline 1.9 Percent, Sales Mostly Stagnant for 17 Months

April 15: Elon Musk Fires 10 Percent of Tesla Workforce, Prepares for “Next Phase of Growth”

Misfiring on All Cylinders

For the past two years whenever one segment of the economy misfired, another picked up. Some labeled this a rolling recession.

Every time consumers appeared to throw in the towel, there was another surge in spending.

Now it appears the economy is misfiring on consumer discretionary spending, new home sales, existing-home sales, durable goods, EVs simultaneously, and income simultaneously.

Recession Q&A

Q: Mish aren’t you nearly always early on recession calls?

A: Guilty as charged.

Q: Did you call a recession that did not happen at all?

A: Guilty as charged.

Is the US in Recession Now? Two Prominent Competing Views

On May 28, I discussed the question Is the US in Recession Now? Two Prominent Competing Views

Danielle DiMartino Booth has been beating the drums for weeks that the US is in recession and has been since October. No so fast says Jim Bianco.

I also explain how I went wrong on my recession forecasts and why I believe Booth is early in her position that a recession started in October 2023.

Finally, I discuss when I think recession is likely.

In the above post I discuss the McKelvey indicator championed by DiMartino Booth. It has a pretty good but not perfect track record in forecasting recessions.

My follow-up post was on GDPplus, another recession indicator, discussed below. First, please note the big reason the economy avoided a recession in late 2022 and 2023 was amazingly enough a tax cut!

Tax Cuts Explain Surge in Consumer Spending in 2023

{kind=link}

Tax data from the BEA, chart by Mish

On January 29, 2024, I commented Tax Cuts, Not Bidenomics Explains Surge in Consumer Spending in 2023

Also, on January 1, 2023, 38 states had noteworthy tax changes. 37 of the changes put extra money in people’s pockets. The combination murdered the then-pending recession.

For details of the tax cut please click on the previous link.

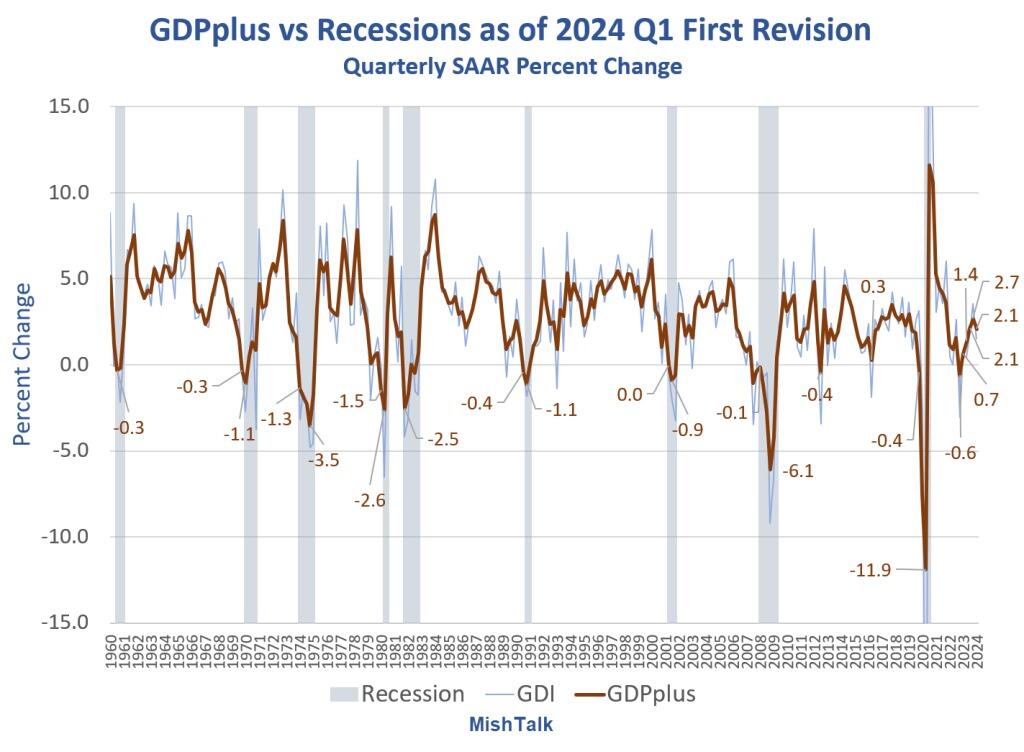

The GDPplus Indicator

GDPplus is a Philadelphia Fed method that blends, not averages GDP and GDI. The Philadelphia Fed revised the indicator significantly lower on Thursday.

It’s also a very good predictor of recessions.

{kind=link}

GDPplus from Philadelphia Fed and GDI from the BEA, chart by Mish

For discussion, please see Philadelphia Fed GDPplus Revised Significantly Lower, But No Recession Yet

By “yet” I was referring to the idea that a recession started in 2024 Q1.

Data is now weakening so fast, on so many fronts, that I expect a recession this year. Unlike 2023, there will be no tax cut or minimum wage hikes in 37 states to boost consumer spending now.

Judging from the recent slide, and assuming it continues, the economy may have peaked in April with a recession starting in May.

Label it recession by slow-acting poison of Bidenomics with a temporary 2023 reprieve due to tax cuts.

Tyler Durden

Thu, 06/06/2024 – 19:45