42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

There Isn’t Much That Can Stop This Market For Now

By Michael Miska, Bloomberg Markets Live reporter and strategist

With US inflation and retail sales both cooling, bets that the Federal Reserve will cut interest rates are back, and there isn’t much left that could stop stocks from hitting new highs.

After most equity markets fully erased April losses — brushing off a perceived delay in rate cuts, sticky inflation and signs of slowing in the US job market — nothing seems to be able to halt stocks. Financial conditions are loose, the economy is holding up and even recovering in Europe, the technical picture is bullish, and the earnings season was overall pretty reassuring once again.

“Sentiment seems to be boosted as inflation hasn’t surprised to the upside and retail sales are on the face of it slowing,” says Charles Hepworth, Investment Director, GAM Investments. “The landscape is moderating, and that means lower volatility and easier prognostics — all of which means market direction can continue to the upside.”

{kind=link}

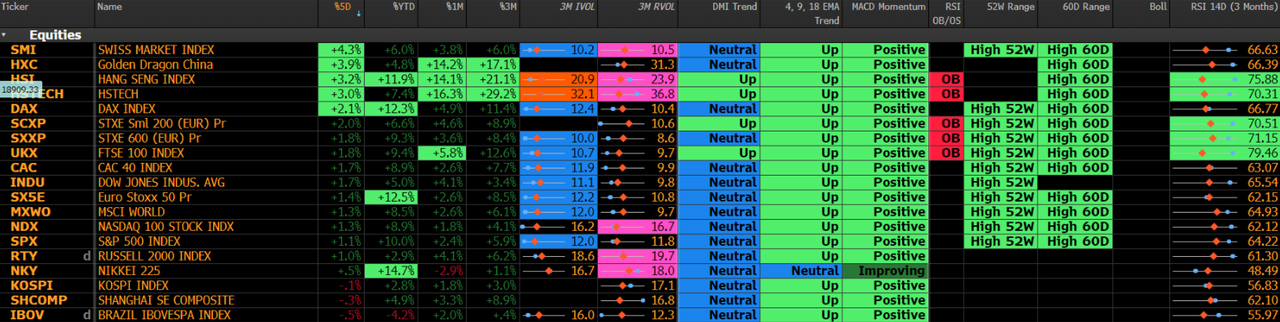

Momentum is running in favor of bulls as all major markets are moving firmly into higher gear, with only a few minor overbought warnings flashing so far. It leaves stocks with upside room, while also limiting setbacks for the time being unless there is a major change in the fundamental perception of the environment.

According to a BofA European fund manager survey this week, an increasing number of investors are bullish about the macro-economic outlook in Europe. A net 61% of respondents expect stronger European growth over the coming 12 months, up from 50% last month and the highest since July 2021. Meanwhile, only 22% of investors see growth slowing in the near term in response to the lagged impact of monetary tightening, down from 83% at the start of the year.

{kind=link}

To be sure, after a mild correction so quickly erased, the summer months could prove a bit more volatile if history is any guide. Further rate-cut repricing can’t be excluded while inflation has been slowing but is still above target.

“Real rate risk is not dead,” say Natixis strategists Emilie Tetard and Florent Pochon, adding the type of configuration seen in April, when real rates rising hit risk assets, may well come back in the medium term, with inflationary risk persisting, uncertainties over the level of the so-called ‘neutral’ rate and rising budget deficits. The best hedges against real rate shocks remain the dollar, as well as defensive sectors and low vol style, they say.

In the meantime, equity volatility risk gauges from VVIX to skew and tail risk pricing had edged higher ahead of CPI, although from a low level, but are already being compressed again after the inflation print.

{kind=link}

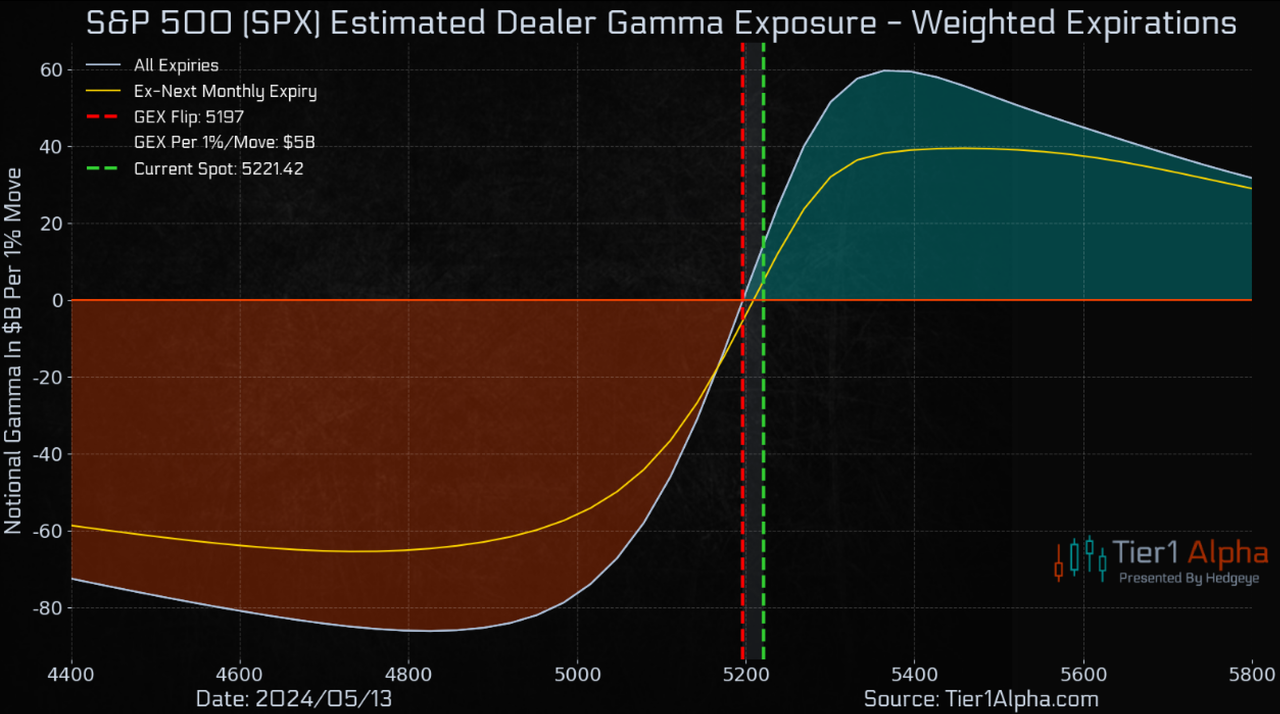

Option trading desks note that dealers are back into a long gamma environment and while that’s not helping the upside as such, long gamma acts as a stabilizer in markets and a volatility dampener. Both nice things to have at a time when there are enough upside catalysts in store.

“The put/call skew remains low, and premiums only saw a modest jump, suggesting that overall hedging demand remains subdued,” according to strategists at Tier 1 Alpha. “This implies that while there are some signs of potential volatility, the market is not yet in a state of high anxiety.”

{kind=link}

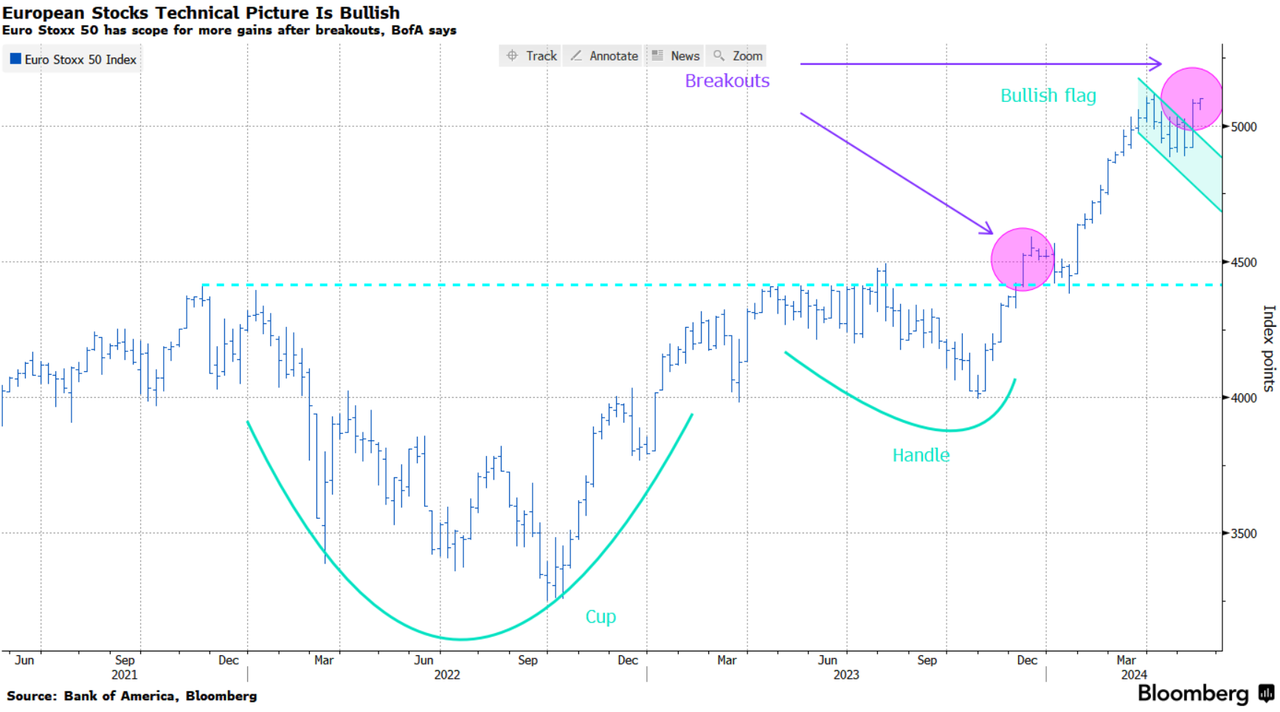

And the technical picture remains bullish, according to Bank of America technical analyst Stephen Suttmeier, flagging that the advancers-decliners line of 73 country indexes continues to hit new all-time highs and achieved another last week. Referring specifically to Europe, he says the Euro Stoxx 50 remains in a bullish trend after a breakout from a cup and handle pattern, suggesting further upside towards 5230-5360 and the 5500s, while the bullish flag breakout last week reinforces the view as long as the 5000 support level holds. “Equity market strength is global and broad,” he says. “We view this as bullish.”

{kind=link}

Tyler Durden

Thu, 05/16/2024 – 09:00