42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

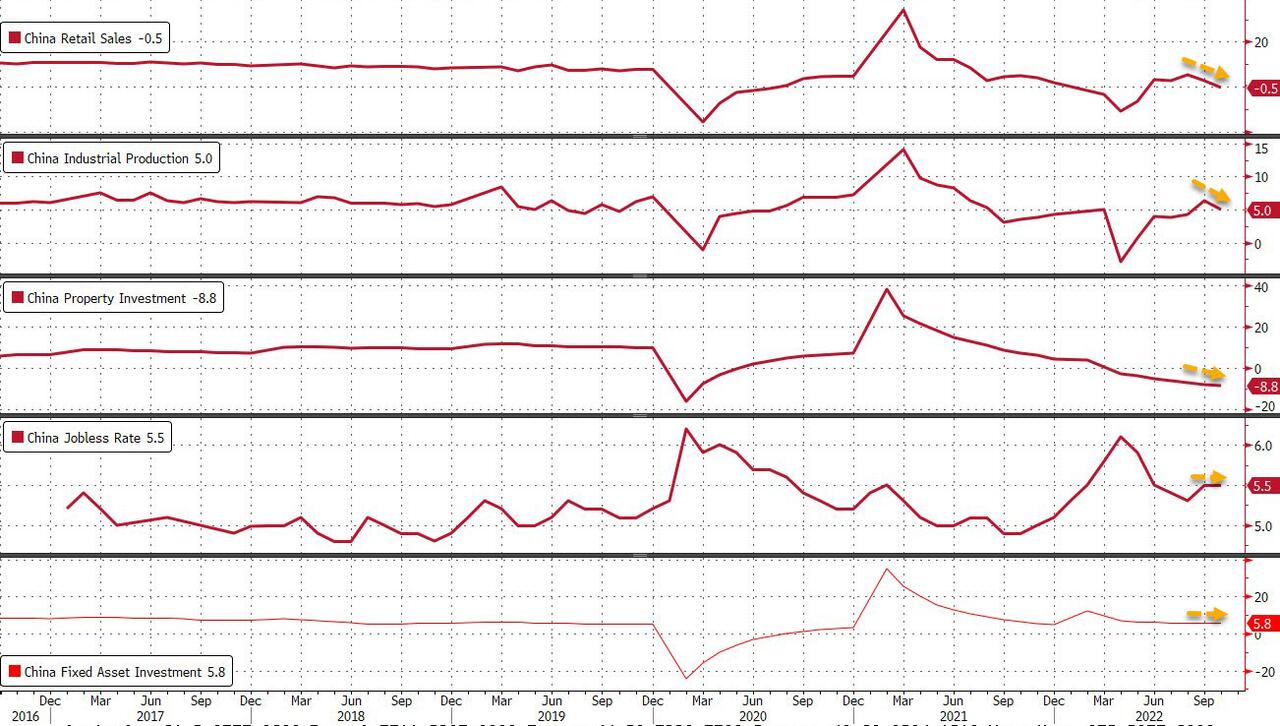

Ugly Chinese Data Dump Misses Across The Board, Pushing Futures Higher On Stimmy Hopes

Instead of delaying the largely meaningless GDP print, maybe Xi should have instructed his henchmen to push back on the latest retail sales/industrial production data dump which was once again confirmed that China’s economy is a walking, tocking timebomb.

In short, everything missed:

October Retail sales -0.5% Y/Y, missing exp. +0.7%

October Industrial Output +5.0% Y/Y, missing exp. +5.3%

Jan-Oct Fixed Investment 5.8%, missing exp. 5.9%

Jan-Oct. residential property sales -28.2% y/y vs -28.6% in Jan.-Sept.

Oct jobless rate 5.5% vs 5.5% in Sept.

And visually:

{kind=link}

Some more details: retail sales missed by 1.1 standard deviations, and industrial production by 0.6 standard deviations; fixed asset investment which reflects government efforts to stimulate the economy was the closest to consensus. Property investment missed by 0.9 standard deviations, and remains in deep contraction for the year. Unemployment met consensus for 5.5%.

While stocks initially slid on the news, futures traded up to session highs as the across the board miss – similar to last week’s US CPI – was seen as encouraging for equities and negative for yuan on the expectation that these numbers could spark further easing. Also, recall that the latest Chinese CPI and PPI data showed that China is now in outright deflation, meaning the bar for further easing is getting lower by the day, especially since the post congress environment seems focused on economic revival.

{kind=link}

To be sure, as Bloomberg notes, policy, especially monetary, still has a lot to do — note that the total social financing data last week registered a 2.5 standard deviation miss versus consensus, the biggest shortfall since April.

One final quick note: Beijing was quick to blame the dismal economic data on the latest round of covid outbreaks and resulting lockdowns, which is precisely why Xi continues to use Covid Zero as a “justification” for every economic miss, and why as long as China’s economy continues to stagnate – mostly due to the ongoing collapse in housing and property markets – the covid zero scapegoat will remain to divert attention from the real source of economic devastation – the bursting of the housing bubble.

And yet, with China’s massive population becoming increasingly angry at the relentless lockdowns, the latest property “rescue package” which just passed this weekend, was right in time to allow China to miraculously exit its “national covid nightmare” some time in Q1 2023.

Tyler Durden

Mon, 11/14/2022 – 21:31