42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

US Services Surveys “Paint A Concerning Picture” Into Year-End, Export Orders Collapse

Following the disappointing drops in US Manufacturing surveys, this morning’s US Services surveys were also expected to show declines.

S&P Global’s Services PMI final print for October was 47.8 (better than the flash print of 46.6 but lower than September’s 49.3). This is the 4th straight month of contraction according to this signal.

ISM Services fell from 56.7 to 54.4 in October (worse then the 55.3 expected). This is the weakest print since May 2020.

{kind=link}

Source: Bloomberg

Under the hood of the Services PMI print, new export orders collapsed and employment contracted…

{kind=link}

Source: Bloomberg

Anthony Nieves, ISM Chair warned:

“Growth continues at a slower rate for the services sector, which has expanded for all but two of the last 153 months. The sector had a pullback in growth for the second consecutive month in October due to decreases in business activity, new orders and employment.”

ISM Respondents are not exactly exuberant:

“Despite the negative inflation news, higher gas prices and concerns of a recession, our restaurant sales have been resilient during what is typically a seasonal slump. We are positive to 2019 (pre-coronavirus pandemic), and traffic is down only about 4 percent, so it’s recovering. Staffing and supply chain challenges are improving, (and we are) seeing some decline in key commodities.” [Accommodation & Food Services]

“Business remains tepid. We have a general concern that sales volumes are trending down as buyers communicate that they’re planning to buy only what they need for immediate sales.” [Agriculture, Forestry, Fishing & Hunting]

“Customers are starting to delay projects and/or entering smaller-scale scopes of work. We believe this is a continuation of an uncertain economic environment.” [Construction]

“There are supply chain challenges for some paper- and tech-related products.” [Educational Services]

“Shortages and delays stabilizing. Labor availability and patient volume continue to be a challenge.” [Health Care & Social Assistance]

“Electronic components lead times are becoming longer, pushing out almost a year. Not seeing much change in pricing based on inflation pressures at this point, but we expect to see changes after the first of the year. Business volume remains strong.” [Other Services]

“As we prepare for a recession, our stakeholders, clients and vendors are all tightening their belts and reducing new spend. We are focusing on strategic renewals and expanding only where necessary with our closest vendor partners for our most critical tech projects.” [Professional, Scientific & Technical Services]

“Prices seem to continue increasing for commodities, including plumbing, flooring materials, floor adhesives, door locks, and bedroom and bathroom doors. Delays in delivery have increased after leveling off in the middle of the year.” [Real Estate, Rental & Leasing]

“We are in the final preparations for a successful holiday, despite lower sales. Labor is more available this year, and supply chain delays seem caught up for now.” [Retail Trade]

“It has become more challenging to maintain our level of service, due to increased demand, extended supplier lead times and the hyper-competitive employment market.” [Transportation & Warehousing]

“We are experiencing a bullwhip of oversupply on some goods … while still desperately short on other goods. The market is recovering very inconsistently.” [Wholesale Trade]

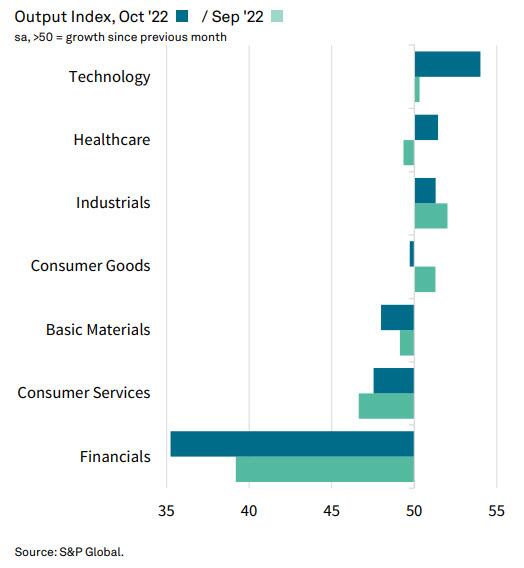

Four out of seven US sectors monitored by S&P Global PMI data recorded lower business activity during October with Financials the worst-performing sector for the fifth month in a row…

{kind=link}

Siân Jones, Senior Economist at S&P Global Market Intelligence, said:

“Service sector firms faced a challenging start to the final quarter of 2022, as a renewed contraction in new business dragged output down further. Demand conditions were hampered by tighter financial conditions and elevated rates of inflation, leading to reports of postponements and the delayed placement of orders as customers assess their spending.

“Subdued demand and weaker confidence in the outlook for output led to a near-stagnation in employment. Reports of the non-replacement of voluntary leavers brought signs that firms were evaluating costs and future demand more closely before advertising vacancies and expanding staffing levels.

“Nonetheless, momentum in previously soaring inflation slowed again. Hikes in costs softened, as service providers and manufacturers saw slower upticks in supplier and input prices. Meanwhile, private sector firms sought to boost demand through a slower increase in selling prices. Although softening, further elevated rises in prices paid by consumers present obstacles to firms in an already challenging demand environment and paint a concerning picture as we head towards the end of the year.“

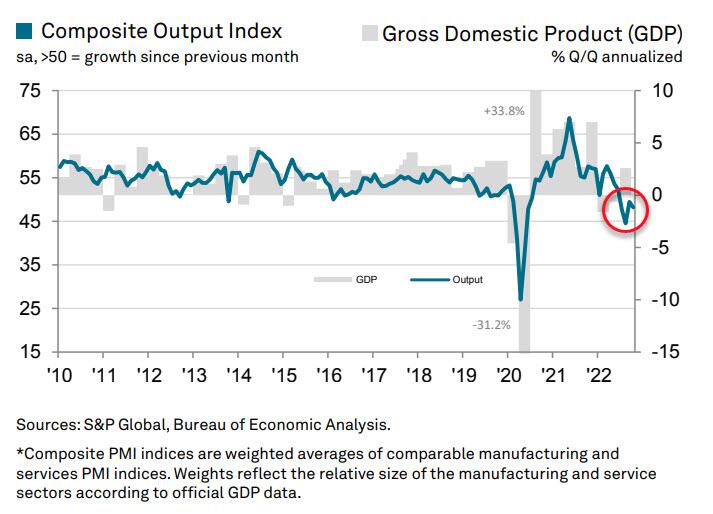

Finally, The S&P Global US Composite PMI Output Index posted 48.2 in October, down from 49.5 in September.

{kind=link}

Not a pretty picture for US economic growth in Q4.

Tyler Durden

Thu, 11/03/2022 – 10:07