42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Manufacturing Surveys Signal Slowdown Continues; New Orders, Prices Plunge

Despite better-than-expected US macro data in the last few weeks, the ‘soft’ survey data on the Manufacturing side of the economy has been rapidly losing momentum.

However, according to this morning’s final October print for S&P Global’s PMI, things improved throughout the month from a 49.9 (contractionary) preliminary print to a final of 50.4 (still notably down from September’s final print of 52.0). That is the weakest print since June 2020.

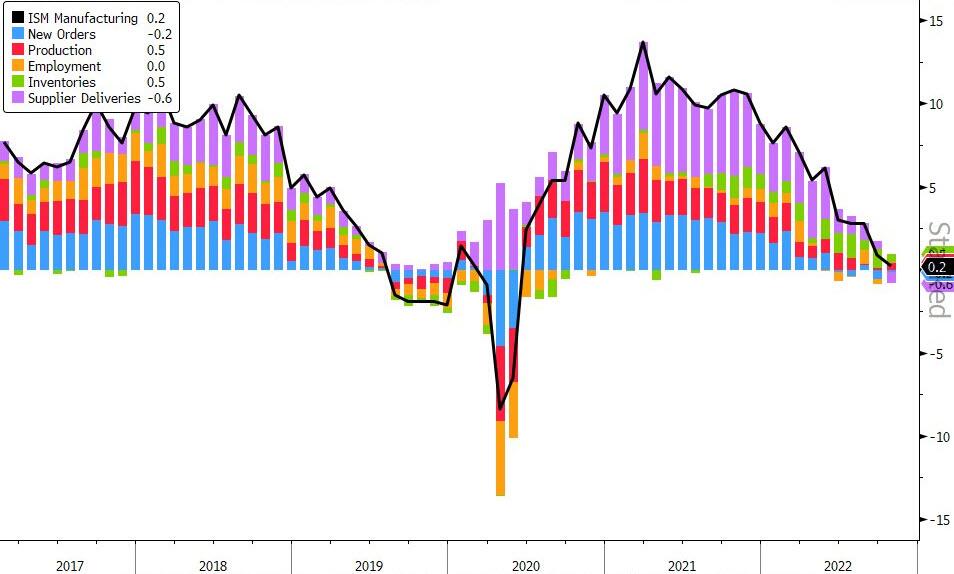

The ISM Manufacturing survey also printed slightly better than expected at 50.2 (50.0 exp) but was lower than the September print of 50.9. That is the weakest since May 2020.

{kind=link}

Source: Bloomberg

This comes after the overnight session saw China and UK PMIs remain in contraction (deepening in the latter).

The PMI data showed the sharpest drop in new orders since May 2020, but on the positive side, inflationary pressures softened further.

On the ISM side none of the major components are in expansion with new orders at 49.2 and employment at 50.0, but, like PMI, prices plunged to 46.6…

{kind=link}

Source: Bloomberg

Inventories and production added very marginally to PMI…

{kind=link}

Source: Bloomberg

ISM Respondents did not sound upbeat at all:

“Flat business activity: continued electronics market challenges.” (Computer 8 Electronic Products]

“Customers are canceling some orders. Inventories of finished goods increasing. Expect some bounce back as some customers may be waiting for commodity prices to decline (further).” (Chemical Products]

“Challenges with labor and parts delivery are easing. Order levels are slowing down after pent-up demand in the previous month.” [Transportation Equipment]

“Growing threat of recession is making many customers slow orders substantially. Additionally, global uncertainty about the Russia-Ukraine (war) is influencing global commodity markets.” (Food. Beverage 8 Tobacco Products]

“We have seen a general pullback in available capital budgets from our customers, and that is having a significant impact on our sales in the fourth quarter.” (Machinery]

“Housing market is down, so our business is affected. Capacity has increased over the last two years due to high orders of consumer goods and appliances, so now we re trying promotions to get our orders up to where we can use all our capacity.” [Electrical Equipment. Appliances 8 Components]

“Customer demand has been slower for two months. Production is decreasing our inventory and (we are) implementing forecasts carefully. The headwind seems to be very strong, so we need to be prepared for that.” (Fabricated Metal Products]

“International conditions loom large and seem very foreboding. Overall, we still think 2023 will be a positive year, with at least some moderate growth.” (Nonmetallic Mineral Products]

“Lead times are improving. Plastic prices are coming down.” [Plastics 8 Rubber Products]

“Prices are continuing a slight decline. Suppliers are trying to hold off decreases, but competition is increasing.” [Miscellaneous Manufacturing]

Looking forward, things are bleak as output expectations for the coming 12 months weakened in October. Although still generally upbeat, the degree of confidence was the lowest since May 2020 as firms expressed concerns regarding inflation and overall demand conditions.

Siân Jones, Senior Economist at S&P Global Market Intelligence, said:

“October PMI data signalled a subdued start to the final quarter of 2022, as US manufacturers recorded a renewed and solid drop in new orders. Domestic and foreign demand weakened due to greater hesitancy among clients as prices rose further and amid dollar strength. As such, efforts to clear backlogs of work, rather than new order inflows, drove the latest upturn in production.

“Confidence in the outlook waned as underlying data also highlighted efforts to cut costs and adjust to more subdued demand conditions in the coming months. Input buying fell sharply and resilience in employment stumbled, as the pace of job creation eased to only a marginal rate.

“On a more positive note, input costs rose at the slowest pace in almost two years amid signs of reduced disruption in supply chains. Lower demand for inputs was a contributing factor to this, however. Nevertheless, softer hikes in costs were reflected in a slower uptick in output charges, as firms sought to pass on cost savings where possible to try and boost sales.”

Finally, this ISM print is important as JPMorgan warned this morning:

“The Fed may have comments on economic risks becoming more balanced between growth and inflation; in that regard, ISM numbers matter as once the US falls into contractionary territory, the market will increasingly look for a change to the Fed’s hawkish behavior.“

The question is – are these ISM/PMI prints on the day the FOMC begins its deliberations enough to spook Powell into pausing or ‘stepping down’?

Tyler Durden

Tue, 11/01/2022 – 10:05