42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

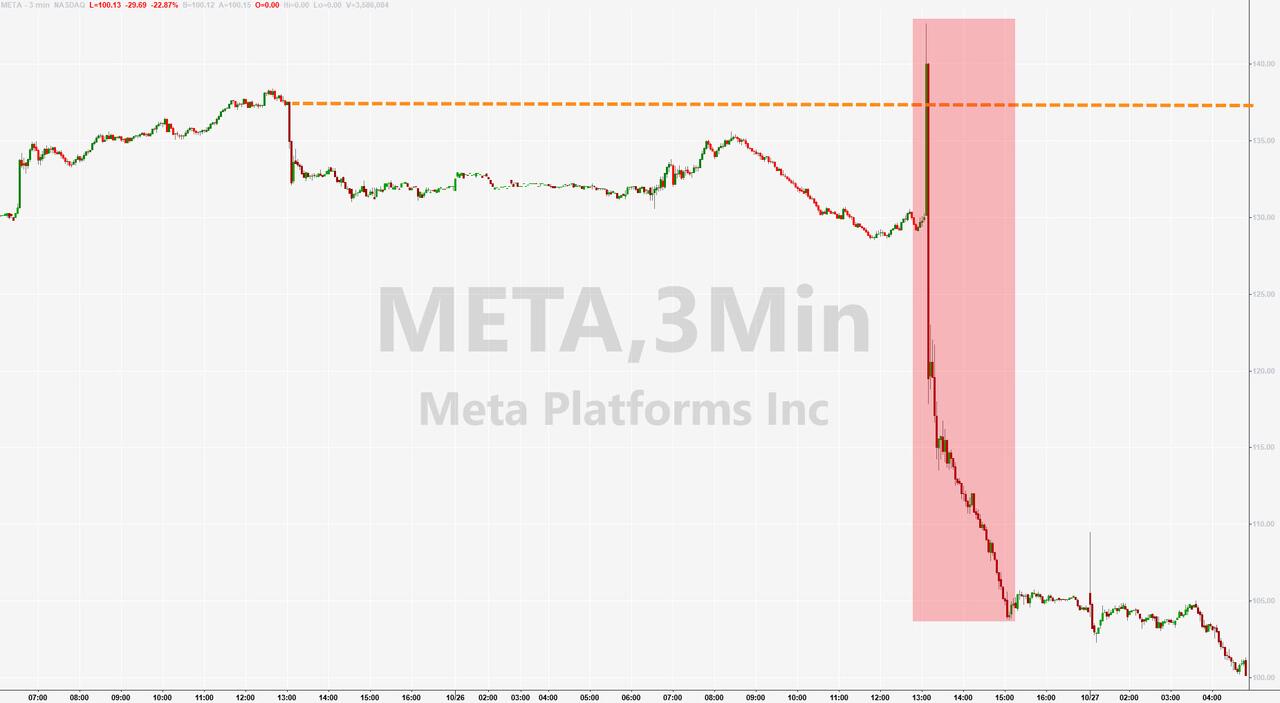

As META Plunges To Double-Digits, Wall Street Gives Up On Facebook

META shares are down a stunning 23% from Tuesday’s close after last night’s earnings signals Zuckerberg’s ‘Reality Labs’ moneypit is growing with the second straight quarter of revenue declines from the year earlier (after the first decline ever last quarter), and disappointing revenue forecasts.

This is the second largest drop in META’s history and the stock just trading back below $100 for the first time since Jan 2016…

{kind=link}

Results also highlight the recent weakness in the advertising market that’s hitting other businesses heavily reliant on ad sales like Alphabet and Snap. Multiple firms downgraded the stock…

Here’s what analysts are saying:

Cowen (downgrades to market perform from outperform, PT to $135 from $205)

Spending growth at Meta is much higher than expected; “we expected the company to rein in costs given macro headwinds”

“The company expects metaverse losses to expand significantly without a clear timeline of returns for investors”

Morgan Stanley (cut to equal-weight from overweight, PT $105 from $205)

These investments signal higher “required structural capital intensity going forward” as META adjusts to new social media landscape post Apple’s privacy update

Although these investments could make the company stronger over 5 years, expect 2023 free cash flow heading 60% lower

KeyBanc Capital Markets (cut to sector weight from overweight)

Next year’s costs “were meaningfully higher than expected”

“Meta appears to have limits on how fast it can pull back expenses – even with Meta targeting flattish headcount growth, opex should still increase ~$13B y/y at the midpoint”

Bloomberg Intelligence

“Meta’s outlook for a high-teens gain in operating costs and capital spending in 2023 might prove a far greater drag on consensus”

Jefferies (buy, PT $200)

There are “no signs of expense discipline,” and this is “going against what investors want”

Vital Knowledge

The expense outlook is “the big negative” of the report; “investors were hoping for mgmt. to aggressively slash costs, but it doesn’t seem like that’s happening”

The results and outlook “weren’t great, but neither was any worse than SNAP or GOOGL”

Truist Securities (buy, PT $240)

The revenue outlook is “still decent all things considered,” but the guidance for total expenses is “materially higher than our estimate”

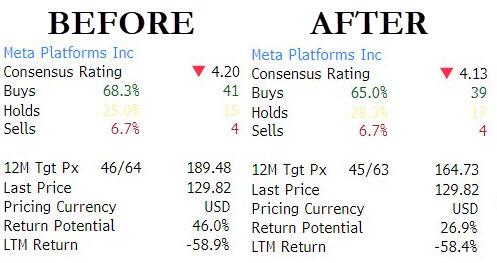

But, after all that there are still 39 Buys and only 17 Sells…

{kind=link}

Tyler Durden

Thu, 10/27/2022 – 07:57