42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Wall Street Reacts To The Catastrophic Megatech Earnings… And Why There Is A Silver Lining

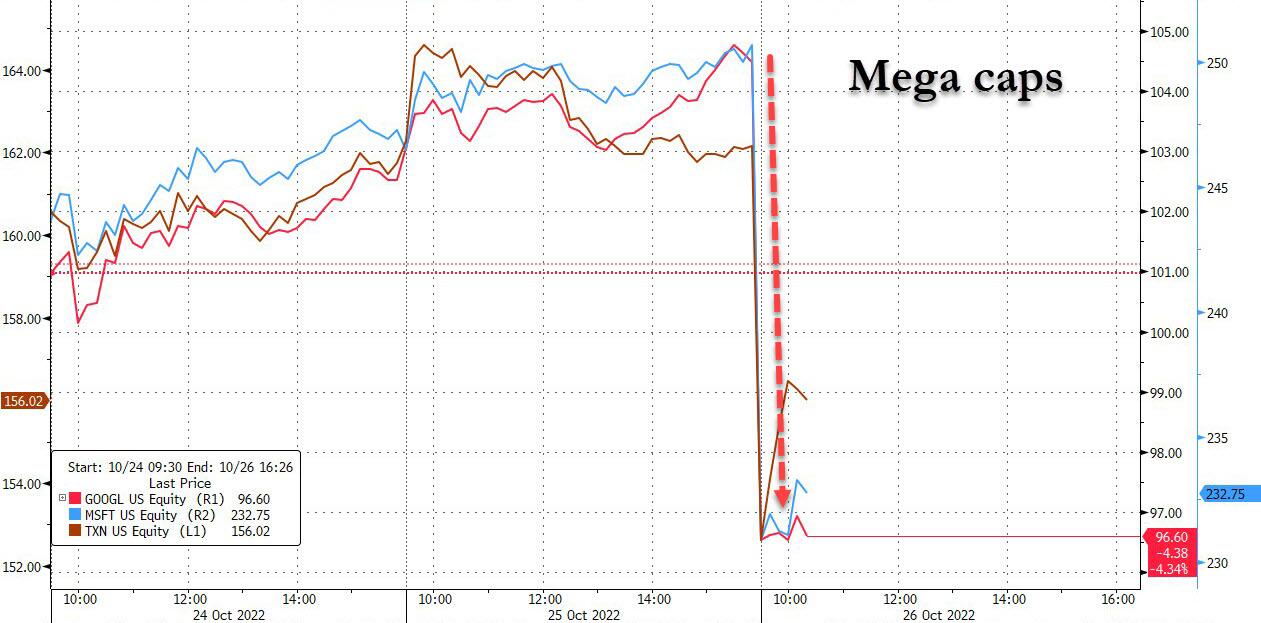

It’s been a terrible morning for the tech giants which reported yesterday, GOOGL, MSFT, TXN, all of which either missed or guided much weaker than expected. The results is this:

*ALPHABET FALLS 8% AT THE OPEN AFTER 3Q RESULTS DISAPPOINT

*MICROSOFT SINKS IN BIGGEST INTRADAY DROP SINCE MARCH 2020

*TEXAS INSTRUMENTS SLIDES 6.1% AT THE OPEN, MOST SINCE FEB. 3

Below we compile some of the most notable hot takes following the dismal earnings which started off the tech portion of earnings season on a decidedly wrong foot.

First Microsoft:

Microsoft shares tumbled after the software company reported its weakest quarterly sales growth in five years and gave a lackluster forecast for sales growth in its Azure cloud-computing services business. Analysts noted that Azure growth is expected to moderate, “elevating near-term concerns.” That echoed disappointing results from other industry giants, leading US tech stocks to tumble.

Here’s what analysts are saying

Piper Sandler (overweight, PT cut to $265 from $275)

FX headwinds and deteriorating macro conditions pressure outlook

Azure growth is expected to moderate, “elevating near-term concerns on competitive pricing and workload optimization efforts that could curb consumption patterns heading into a recession”

Jefferies (buy, PT cuts to $270 from $275)

Azure miss was due to a moderation in consumption across customer base and geographies

The personal computer markets deteriorated further in September

RBC Capital Markets (outperform, PT cut to $310 from $380)

Microsoft’s commercial outlook was mixed with Office 365 looking encouragingly resilient and Azure’s disappointing outlook

Morgan Stanley (buy, cuts PT to $307 from $325)

While investors were expecting some cyclical weakness, they might be surprised by the magnitude

Barclays (overweight, cuts PT to $296 from $310)

Results from Microsoft’s More Personal Computing and Productivity businesses “should calm investors,” though “not all was perfect, as Azure growth of 42% YoY in constant currency was slightly below consensus at 42.6% and gross margins came in slightly below”

Bloomberg Intelligence

“Microsoft’s sales growth of 16% in constant currency gives us confidence that tech spending is stable amid economic uncertainty”

* * *

Alphabet

Alphabet shares are also tumbling after the Google parent reported third-quarter revenue that was weaker than expected, reinforcing concerns about a slowdown in the ad market. Analysts also singled out a strong US dollar as a headwind.

Here’s what analysts are saying

Raymond James (outperform, PT to $120 from $143)

The soft results reflect difficult year-over-year comparisons and an “increasingly challenging macro environment”

“We are optimistic that margins can improve by later 2023”

Citi (buy, PT $120)

“The macro environment is likely to continue impacting the broader online advertising environment,” although “Alphabet remains one of the best positioned companies across the Internet sector”

Baird (outperform)

Most of the softness came from YouTube and Network, due to the sluggish performance in app installs, macro impact on video ads and some cannibalization from Shorts

Goldman Sachs (buy)

YouTube results were much weaker and “likely reflective of a mix of brand ad dollar volatility, revenue headwinds created by consumption mix to Shorts and one last quarter of tougher comps from direct response revenue growth last year”

Bloomberg Intelligence

“Alphabet’s weakness, particularly in its high- margin Google Network segment, shows the company isn’t immune to ad pricing”

Jefferies (buy, PT $130)

Ad revenue was weaker than expected, “likely due to FX and macro,” while Google Cloud was strong

Truist Securities (buy, PT $136)

“The top and bottom lines missed Street expectations,” with revenue pressured by a currency headwind

The miss “overshadows sustained momentum” in the US

* * *

Finally, Texas Instruments

Texas Instruments shares are down 6.1% on Wednesday, after the chipmaker’s fourth-quarter outlook signaled that the semiconductor industry’s slump is spreading beyond PCs and smartphones to the once-healthy industrial segment. KeyBanc analysts note that while chip softness broadens, the auto segment continues to hold up

Here’s what analysts are saying

KeyBanc Capital Markets (overweight, PT cut to $210 from $220)

Lowering guidance to be consistent with expectations as “a broader inventory correction” is commencing

Expect headwinds to persist over the next several quarters

Morgan Stanley (underweight, PT cut to $152 from $160)

TI remains more cautious than its analog peers

“The company’s sober outlook will be something of a negative outlier – but a broad-based inventory correction will eventually impact everyone”

Citi (neutral, PT cut to $155 from $165)

“TXN reported increasing cancellations as the downturn takes hold”

Truist Securities (hold, PT $172)

The outlook “represents a 12% sequential decline and is about 7% below both typical seasonality and consensus expectations”

Mizuho Securities

The outlook “is not a total shock” and “looks a bit worse on surface than reality,” writes Jordan Klein, a managing director and tech analyst

Given the stock’s year-to-date outperformance relative to chips, some investors may be looking to sell or short the stock

* * *

After the dismal earnings, all the three stocks were trading sharply lower, and dragging down their peer group, which early this morning was set to shed nearly $300 billion in market cap as the combined weight of just the three companies above amounts to more than 19% of the Nasdaq 100.

{kind=link}

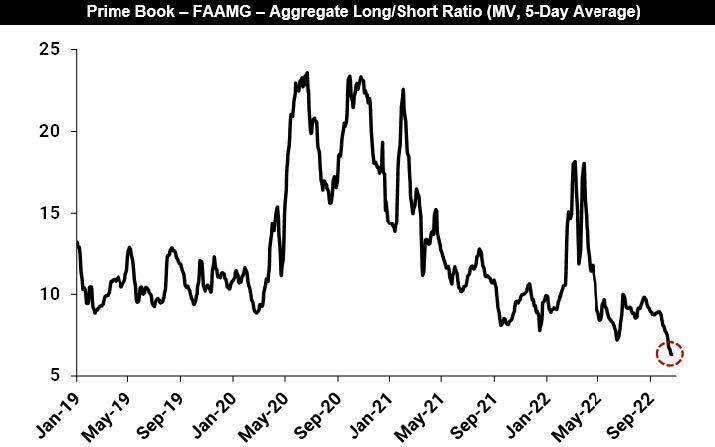

Despite the devastation unleashed by these three companies, there was a silver lining.

As Goldman’s Prime Brokerage notes, a possible bright spot is that institutional exposure in FAAMG has been reduced significantly and might soften some of the blow from these prints. Positioning data from the GS Prime book suggest a cautious stance on the mega caps (FAAMG) by hedge funds: indeed, the first chart below shows that the aggregate FAAMG long/short ratio on the Prime book now stands at ~6.3, a multi-year low. For perspective, the same metric was at ~18 in March and at 9.2 in mid-July.

{kind=link}

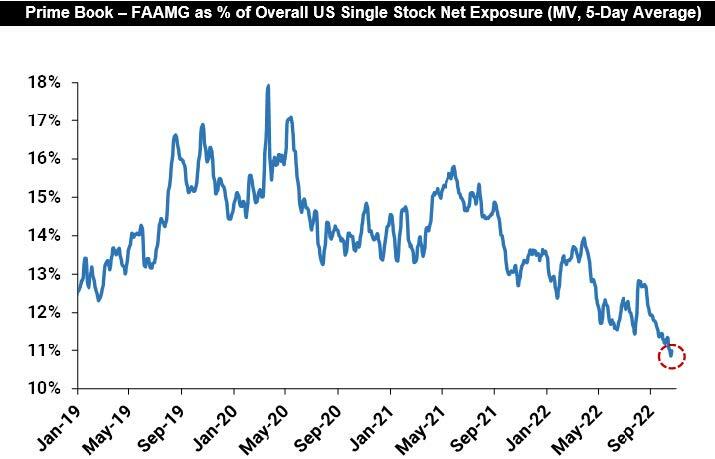

Another note: FAAMG collectively now make up ~11% of the overall US Single Stock Net exposure on the Prime book, also a multi-year low. The same metric was at ~14% in March and at ~12% in mid-July.

{kind=link}

Tyler Durden

Wed, 10/26/2022 – 11:00