42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Tech Wrecks But Bonds, Bullion, & Bitcoin Bid As Rate-Hike Odds Slide

A surprisingly violent day across markets today. FX saw Yuan explode higher; yields plunged everywhere; stocks pumped and dumped (with tech wrecked by MSFT and GOOGL); crypto spiked dramatically higher; oil and gold ramped as the dumped…

Former NYFed President Bill Dudley unleashed another of his infamous op-eds today, calling for The Fed to be hawkish for longer (but not higher)…

“Emphasizing “longer” rather than “higher” has some advantages. It presumably reduces the risk of a hard landing: If monetary policy is somewhat tight, but not very tight, activity and employment should slow gradually. It gives Fed officials time to assess the consequences of their efforts, recognizing that monetary policy entails uncertainty and affects the economy with long and variable lags.

That said, the downside risks are significant. Because less-aggressive tightening takes longer to bring down inflation, it might allow inflationary expectations to become unanchored – a dynamic that only even-higher interest rates could counteract.

…

Volcker did what was necessary and beat inflation. Burns didn’t, and failed. How does Powell want to be remembered?”

So that really doesn’t help does it!

But, rate-hike odds slipped (Nov is still a lock for 75bps but Dec now only 25% odds of 75bps hike, down from around 75% on 10/20)…

{kind=link}

Source: Bloomberg

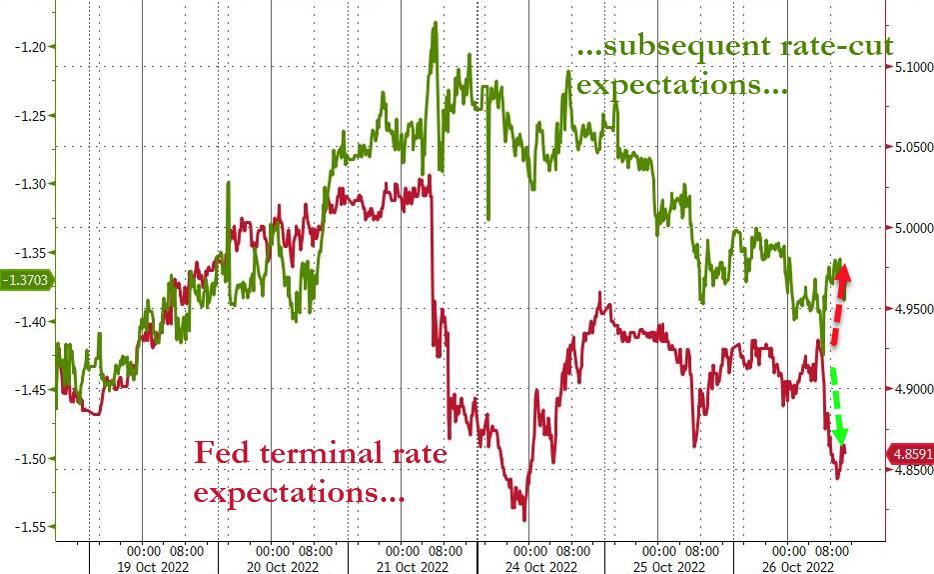

And overall the terminal rate expectation slipped while subsequent rate-cut expectations fell (hawkish)- more pause than pivot…

{kind=link}

Source: Bloomberg

US Majors pumped and dumped today, with MSFT/GOOGL weighing most heavily on Nasdaq overnight. The US cash open sparked another buying panic but the European close ended that fun and games (Nasdaq did not make it back to unch), By the close, the majors were all back the lows of the day with only Small Caps holding any gains…

{kind=link}

Boeing crashed after some early gains, dragging down the Dow also…

{kind=link}

The S&P 500 broke back above its 50DMA (following The Dow and Small Caps) but was unable to hold those gains. Nasdaq remains below its 50DMA…

{kind=link}

Just a reminder, stocks are decoupling from Fed terminal rate expectations on hopes of a pause… but haven’t priced in the actual hikes to the pause (and the pivot is evaporating)…

{kind=link}

Source: Bloomberg

Treasuries were bid across the curve with the long-end outperforming (30Y -9bps, 2Y -5bps). On the week, 2Y yields are down around 4bps (underperforming the rest of the curve), while 10Y is leading the charge, down around 20bps..

{kind=link}

Source: Bloomberg

10Y Yields tumbled back below 4.00% for the first time in a week (10Y yields are down 35bps from Friday’s highs)…

{kind=link}

Source: Bloomberg

Here’s Academy Securities’ Peter Tchir explaining why the market is suddenly so bullish on rates:

There are several reasons, the simplest being the Fed Blackout period. That is important for several reasons:

Fed members, such as Daly, in the moments before the blackout period started, seemed to shift gears in terms of what the Fed would do after November.

The alleged Fed mouthpiece, Nick at the WSJ, posted a note that also seemed to support that view.

So the last few things before the quiet period passed as dovish (at least by recent standards).

Finally, we are not subject to hearing how weak data isn’t changing their trajectory three times after any weak data hits (and weak data is hitting).

The Fed messaging and blackout period helps but isn’t sufficient. Fortunately, if you are bullish rates here, there are other influences that will help support rates:

Lots of signs that inflation is abating (tomorrow’s Inflation Dumpster Dive T-Report).

Earnings calls seem to reflect caution, which can be self-fulfilling.

FX and geopolitics. It is clear that at least Japan and the U.K. have been reaching out directly and through back channels for support. It seems impossible that the ECB hasn’t. So there is pressure on the Treasury and the Fed to throttle back the dollar’s strength. Since we need cooperation for Russia and China, there could be some give or take.

China is un-investible. Expect U.S. investors to pull back from China, with U.S. asset prices likely to benefit.

Post-election policy shifts. I think there are two shifts that are plausible, regardless of who wins the November mid-terms:

Peace in Ukraine? Virtually no effort has been made to figure out an exit ramp for Putin even as his nuclear threats escalate, backed up by increasingly devastating attacks on infrastructure. Maybe, just maybe after the elections, the messaging will suddenly shift from ensuring a Ukrainian “win” to some sort of “global” win.

Inflation fighting at all costs? Given signs the economy is slowing, will politicians stick to the inflation is the devil policy stance? Would that allow the Fed to wait and see? It isn’t a pivot when their work is almost done.

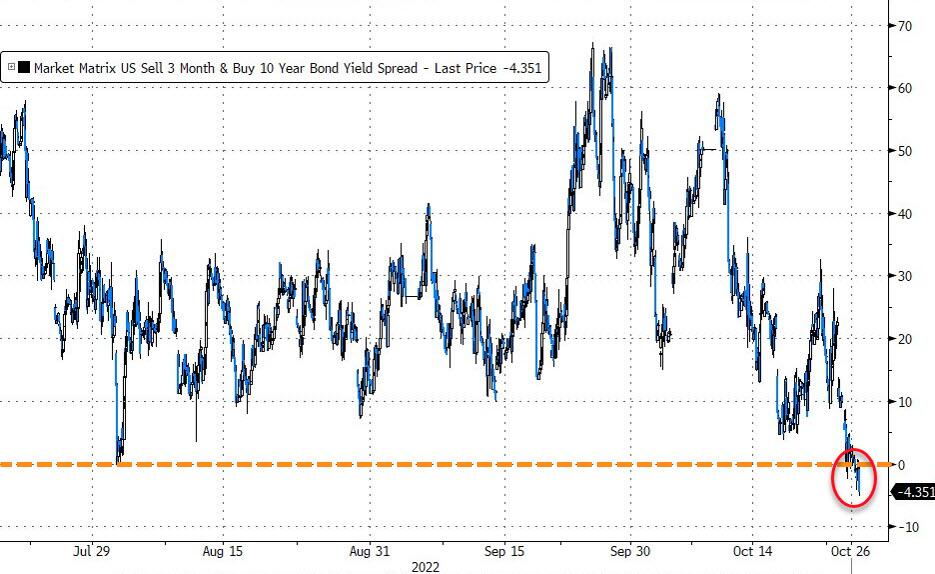

The yield curve flattened further with the all-important 3m10Y finally inverting…

{kind=link}

Source: Bloomberg

The dollar was clubbed like a baby seal, tumbling to 5-week lows today (anyone else smell coordination?)…

{kind=link}

Source: Bloomberg

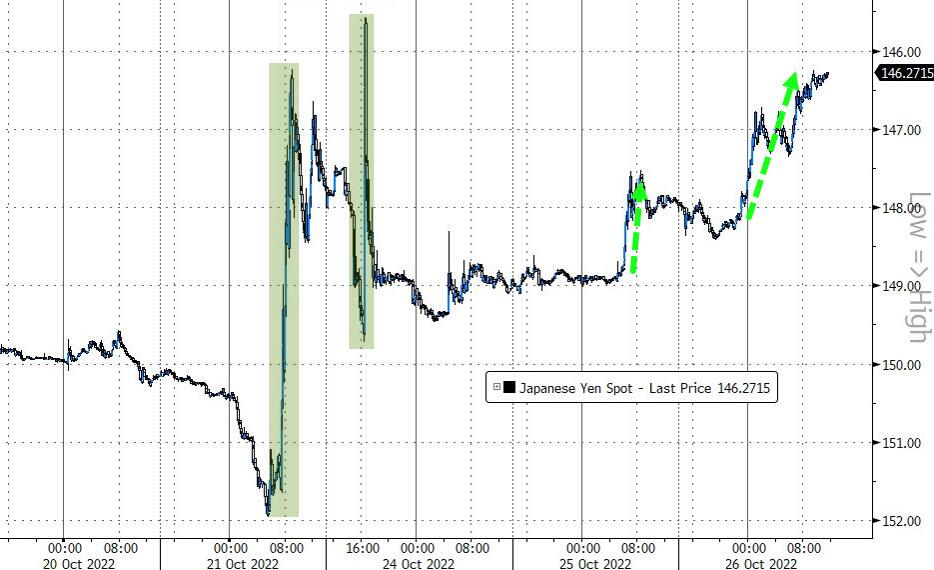

As JPY rallied back to recent yentervention highs…

{kind=link}

Source: Bloomberg

And Offshore Yuan soared by the most on record…

{kind=link}

Source: Bloomberg

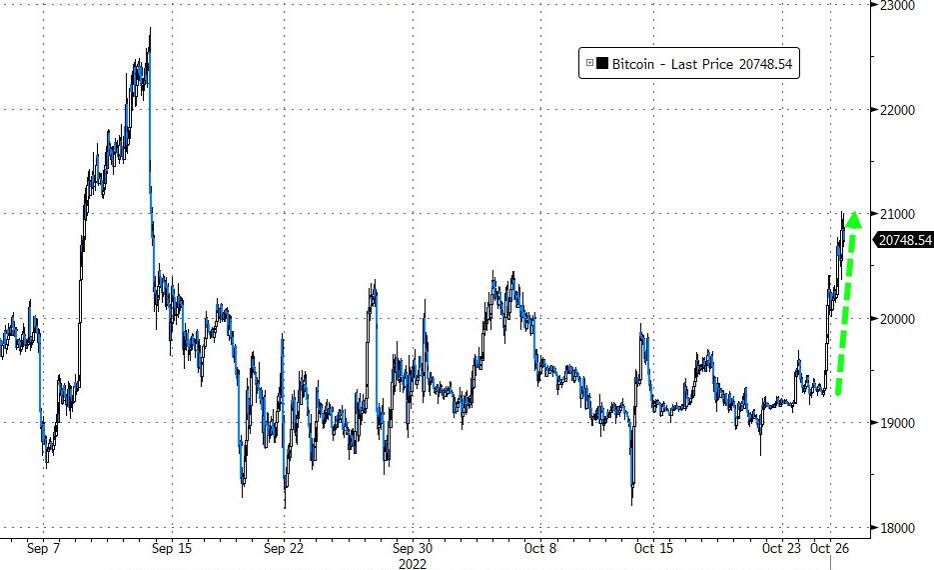

The dollar’s weakness inspired some crypto gains with Bitcoin back above $21,000 (six-week highs)…

{kind=link}

Source: Bloomberg

And gold rallied with futures back above $1675…

{kind=link}

Oil prices extended gains today with WTI back above $88 (2 weeks higher)…

{kind=link}

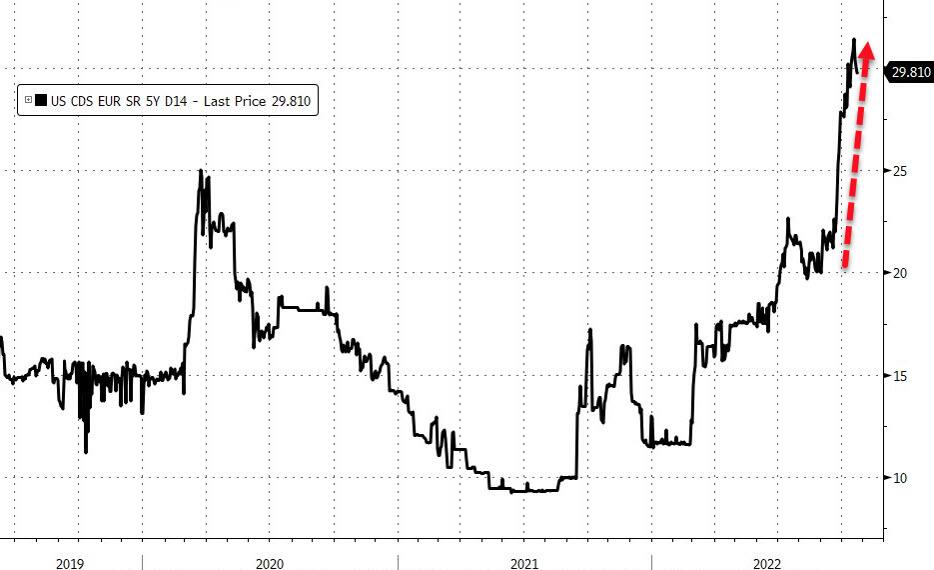

Finally, amid all the chaos, here’s two charts that should help to do anything but calm the nerves. The Sovereign risk of USA and China has been soaring in recent weeks…

{kind=link}

{kind=link}

Source: Bloomberg

Default – unlikely; Devaluation – you decide?

And then there’s this… ‘dad joke of the decade’ by the richest man in the world…

Entering Twitter HQ – let that sink in! pic.twitter.com/D68z4K2wq7

— Elon Musk (@elonmusk) October 26, 2022

And what Friday will be like…

Tyler Durden

Wed, 10/26/2022 – 16:00