42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

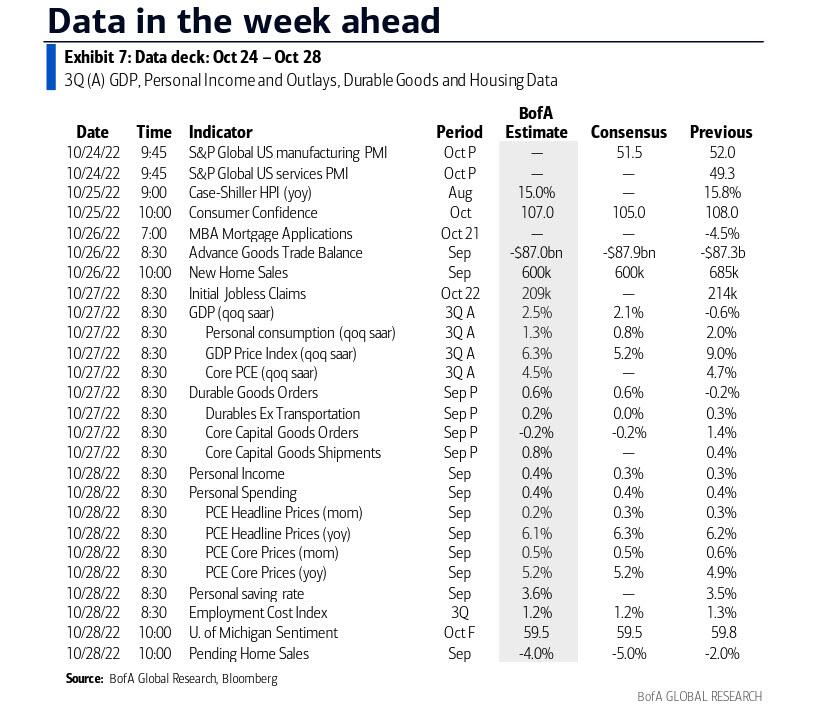

Key Events This Extremely Busy Week: GDP, Employment Costs, PCE, Income & Spending, And An Earnings Avalanche

In his preview of the week’s economic calendar, DB’s Jim Reid writes that maybe the most interesting data this week comes on Friday with the Q3 employment cost index (exp. at +1.2% vs. +1.3% last month) and the September personal income (+0.4% vs. +0.3%) and consumption (+0.4% vs. +0.4%) report, including the core PCE deflator (+0.5% vs. +0.56%). Q3 GDP will also be closed watched, with consensus expecting a bounce from -0.6% to 2.3%. With respect to core PCE, economists expect the Fed’s preferred measure of inflation to rise by 30bps to 5.2%. DB economists highlight that as the median forecast for 2022 core PCE inflation in the Fed’s Summary of Economic Projections from the September 21st meeting was 4.5%, it’s going to be tough to signal a downshift in December.

Elsewhere this week the main highlights are the ECB (Thursday) and the BoJ (Friday) decisions and a huge round of earnings with big Tech the highlight. We also have a new UK Prime Minister as of this moment, after ex-Chancellor Sunak was effectively declared PM tonight. We’ll also see US Q3 GDP (Thursday) and flash PMIs in the US and Europe (today) and October CPIs and GDP for many European countries (Friday). There are other data which are in the day by day guide at the end as usual for a Monday but let’s take a brief look at the highlights outside the already discussed PCE. The ECB’s decision on Thursday will be a big event with our European economists expecting another +75bps hike (72.3bp priced in), followed by +75bps in December (c.62bps priced in), +50bps in February (c.38bps priced), and +25bps in March, reaching a terminal rate of 3%. The press conference as ever will be a focal point and there’ll be lots of attention on technical things surrounding TLTROs and excess reserves. For more on the options here see our fixed income strategists blog from Friday here.

{kind=link}

Staying with central banks, over in Japan, the BoJ announces its decision on Friday amidst continued downward pressure on the yen, which hit a 32-year low against the dollar of 151.95 on Friday before surging again to end the week at 147.65 – c.3.5% swing while the Japanese slept after Nikkei reported fresh intervention from the Japanese authorities. The Yen has again seen a wild session in Asia. After falling again to 149.67 it surged to 145.65 and now trades at 148.88 as we go to press with no clarity on if and what intervention has been done.

For US Q3 GDP this week, DB’s US economists expect real growth to rebound to +3.0% from Q2’s -0.6%. Q3 GDP figures will also be out for European countries on Friday, including for Germany and France with the former likely to be slightly negative and the latter slightly positive. Overall it’s likely to be the start of growth grinding towards or below zero and then staying negative for a few quarters. On European CPI on Friday remember September readings saw Germany’s CPI reaching 10% for the first time since 1950.

Finally, earnings will come thick and fast this week, featuring the big tech, oil majors and key automakers and staples. In tech alone we have Microsoft, Alphabet (tomorrow), Meta (Wednesday) and Apple and Amazon (Thursday). A huge slug (20% by market cap) of the S&P 500 in 48 hours. One thing to not: The GAMMA stocks (Google, Apple, Microsoft, Meta, Amazon) have lost $3 trillion in market cap this year and yet they are still larger than the utilities, energy and consumer sectors combined. Other notable tech firms reporting results will include Intel, Twitter, SAP and Samsung. The other main reporters are in the day by day week ahead at the end.

{kind=link}

Day-by-day calendar of events

Monday October 24

Data: US October PMIs, September Chicago Fed national activity index, Japan, UK, Germany, France and the Eurozone October PMIs

Tuesday October 25

Data: US October Conference Board consumer confidence index, Richmond Fed manufacturing index, August FHFA house price index, Japan September nationwide department store sales, Germany October Ifo survey

Central banks: Eurozone bank lending survey, Fed’s Waller speaks, BoE’s Pill speaks

Earnings: Microsoft, Alphabet, Visa, Coca-Cola, Novartis, UPS, Texas Instruments, Raytheon Technologies, HSBC, SAP, General Electric, 3M, UBS, General Motors, ADM, Valero Energy, Chipotle, Biogen, Halliburton, Spotify, Norsk Hydro

Wednesday October 26

Data: US September wholesale inventories, retail inventories, new home sales, advance goods trade balance, Japan September PPI services, France October consumer confidence, Eurozone September M3

Central banks: BoC decision

Earnings: Meta, Thermo Fisher Scientific, Bristol-Myers Squibb, Boeing, Canadian Pacific, Iberdrola, Boston Scientific, Mercedes-Benz, Heineken, SK Hynix, Ford, Kraft Heinz, Santander, BASF, Twitter, Barclays, Telenor, Puma

Thursday October 27

Data: US Q3 GDP, September durable goods orders, October Kansas City Fed manufacturing activity, initial jobless claims, China September industrial profits, Germany November GfK consumer confidence, Italy October consumer confidence index, manufacturing confidence, economic sentiment, August industrial sales

Central banks: ECB decision, BoE’s Woods speaks, ECB’s Villeroy speaks

Earnings: Apple, Amazon, Mastercard, Samsung, Merck, Shell, McDonald’s, T-Mobile, Linde, TotalEnergies, Comcast, Honeywell, Intel, S&P Global, Caterpillar, AB InBev, American Tower, Gilead Sciences, EDF, Neste, STMicroelectronics, Shopify, PG&E, Repsol, EDP, Pinterest, First Solar, Credit Suisse, Deutsche Lufthansa, Hertz, Ubisoft, Spirit Airlines

Friday October 28

Data: US Q3 employment cost index, September personal income, personal spending, PCE deflator, pending home sales, Japan September jobless rate, Germany, France, Q3 GDP, October CPI, Italy October CPI, France September consumer spending, PPI, Italy September PPI, hourly wages, Eurozone October economic and industrial confidence, Canada August GDP

Central banks: BoJ decision, ECB Survey of Professional Forecasters

Earnings: Exxon Mobil, Chevron, AbbVie, NextEra Energy, Equinor, Sanofi, Porsche, Airbus, Volkswagen, Colgate-Palmolive, Eni SpA, BBVA, LyondellBasell

* * *

Finally, looking at just the US, Goldman writes that the key economic data releases this week are the Q3 GDP advance release on Thursday, and the employment cost index, core PCE, and University of Michigan consumer sentiment reports on Friday. There are no scheduled speaking engagements from Fed officials on monetary policy this week, reflecting the FOMC blackout period.

Monday, October 24

09:45 AM S&P Global US manufacturing PMI, October preliminary (consensus 51.0, last 52.0): S&P Global US services PMI, October preliminary (consensus 49.5, last 49.3)

Tuesday, October 25

09:00 AM FHFA house price index, August (consensus -0.6%, last -0.6%)

09:00 AM S&P/Case-Shiller 20-city home price index, August (GS -0.7%, consensus -0.70%, last -0.44%): We estimate that the S&P/Case-Shiller 20-city home price index declined 0.7% in August, following a 0.44% decline in July.

10:00 AM Conference Board consumer confidence, October (GS 106.0, consensus 105.3, last 108.0): We estimate that the Conference Board consumer confidence index decreased to 106.0 in October.

10:00 AM Richmond Fed manufacturing index, October (consensus -5, last 0)

01:55 PM Fed Governor Waller speaks: Governor Christopher Waller will discuss FedNow at an event hosted by Money20/20. A moderated Q&A is expected; however, he is not expected to comment on monetary policy, reflecting the FOMC blackout period.

Wednesday, October 26

08:30 AM Advance goods trade balance, September (GS -$87.0bn, consensus -$87.5bn, last -$87.3bn): We estimate that the goods trade deficit narrowed by $0.3bn to $87.0bn in September compared to the final August report, reflecting a larger drop in imports than in exports.

08:30 AM Wholesale inventories, September preliminary (consensus +1.0%, last +1.3%)

10:00 AM New home sales, September (GS -17.0%, consensus -15.3%, last +28.8%): We estimate that new home sales declined 17.0% in September, following a 28.8% increase in August.

Thursday, October 27

08:30 AM GDP, Q3 advance (GS +2.4%, consensus +2.3%, last -0.6%): Personal consumption, Q3 advance (GS +1.4%, consensus +0.9%, last +2.0%): We estimate that GDP growth rose +2.4% annualized in the advance reading for Q3, following the 0.6% annualized decline in Q2. Our forecast reflects a slowdown in consumption growth (to +1.4% qoq ar) and large declines in structures investment (residential -23%, nonresidential -6%). We also expect a negative contribution to GDP growth from inventories (-0.7pp) but estimate a large boost from normalization in net exports (+3.1pp contribution). We estimate domestic final sales rose just 0.3% annualized. We will finalize our forecast after Wednesday’s foreign trade and inventory data.

08:30 AM Durable goods orders, September preliminary (GS +1.2%, consensus +0.6%, last -0.2%); Durable goods orders ex-transportation, September preliminary (GS flat, consensus +0.1%, last +0.3%); Core capital goods orders, September preliminary (GS flat, consensus +0.3%, last +1.4%); Core capital goods shipments, September preliminary (GS +0.2%, consensus +0.3%, last +0.4%): We estimate that durable goods orders rebounded 1.2% in the preliminary September report, reflecting strength in commercial aircraft orders but a possible pullback in defense orders. We expect softness elsewhere in the report, including a slowdown in growth for shipments of core capital goods (+0.2%) and unchanged core capital goods orders, reflecting weaker foreign demand and some softening in domestic industrial data.

08:30 AM Initial jobless claims, week ended October 22 (GS 215k, consensus 220k, last 214k); Continuing jobless claims, week ended October 15 (consensus 1,383k, last 1,385k): We estimate initial jobless claims edged up to 215k in the week ended October 22.

11:00 AM Kansas City Fed manufacturing index, October (consensus -2, last +1)

Friday, October 28

08:30 AM Employment cost index, Q3 (GS +1.2%, consensus +1.2%, prior +1.3%): We estimate that the employment cost index (ECI) rose 1.2% in Q3 (qoq sa), which would lower the year-on-year rate by one tenth to 5.0%. Our forecast reflects sequential slowing in the private wages ex-incentives category, based on slowing growth in the Atlanta Fed wage tracker and in production and nonsupervisory average hourly earnings. However, we expect another strong reading for the benefits category as firms expand health insurance and supplemental pay programs in order to attract and retain talent. We see two-sided risk from incentive-paid industries, as fewer home sales commissions (and production bonuses more generally) could be offset by rebounding commissions on home equity loans and HELOCs.

08:30 AM Personal income, September (GS +0.4%, consensus +0.4%, last +0.3%): Personal spending, September (GS +0.6%, consensus +0.4%, last +0.4%); PCE price index, September (GS +0.26%, consensus +0.3%, last +0.29%); PCE price index (yoy), September (GS +6.19%, consensus +6.3%, last +6.25%); Core PCE price index, September (GS +0.36%, consensus +0.5%, last +0.56%); Core PCE price index (yoy), September (GS +5.07%, consensus +5.2%, last +4.91%): Based on details in the PPI, CPI, and import price reports, we forecast that the core PCE price index rose by 0.36% month-over-month in September, corresponding to a 5.07% increase from a year earlier. Additionally, we expect that the headline PCE price index increased by 0.26% in September, corresponding to a 6.19% increase from a year earlier. We expect that personal income increased by 0.4% and personal spending increased by 0.6% in September.

10:00 AM Pending home sales, September (GS -7.5%, consensus -5.0%, last -2.0%): We estimate pending home sales declined 7.5% in September, following a 2.0% decline in August.

10:00 AM University of Michigan consumer sentiment, October final (GS 59.3, consensus 59.6, last 59.8); University of Michigan 5–10-year inflation expectations, October final (GS 2.9%, consensus 2.9%, last 2.9%): We expect the University of Michigan consumer sentiment index decreased by 0.5pt to 59.3 in the final October reading.

Source: DB, BofA, Goldman

Tyler Durden

Mon, 10/24/2022 – 10:15