42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

FedSpeak & Yentervention Spark Buying Panic In Bonds, Stocks, & Gold

With the Fed’s black out ahead of the November meeting beginning tomorrow, it seems they wanted to get as much jawboning in as possible today…

Fed’s Daly (bear in mind she is one of the more dovish FOMC members) built on earlier comments by WSJ Timiraos (conditioning investors for a smaller Dec hike without sparking a melt-up in stocks) offering the market a bone of dovishness (well less than hawkishness)…

*DALY: LITTLE BIT OF PENT-UP TIGHTENING WORKING THROUGH ECONOMY

*DALY: NEED TO WATCH HOW RESTRICTIVE; CAN’T OVERTIGHTEN EITHER; REQUIRES STEP DOWN INTO SMALLER INCREMENTS OF HIKES

But even she backed off from a real dovish perspective…

*DALY: THINK HARD ABOUT STEP DOWN BUT WE’RE NOT THERE YET

Fed’s Evans confirmed the ‘pause’ – not a ‘pivot’…

*EVANS: EXPECT FED TO RAISE RATES FURTHER, HOLD STANCE A WHILE

Fed’s Bullard was his usual hawkish self:

*BULLARD: STRONG JOB MARKET GIVES FED LEEWAY TO FIGHT INFLATION

The result of all this was a dovish drop in terminal rate expectations, but a hawkish shift in subsequent rate-cut expectations (i.e. a pause after Dec/Feb NOT a pivot)…

{kind=link}

Source: Bloomberg

75bps is still a lock for November but the odds of a 75bps hike in Dec tumbled from around 70% to around 30%. (and odds of a 50bps hike in Feb dropped to 30% from 50%)…

{kind=link}

Source: Bloomberg

Between WSJ and Daly, expectations for the yield curve (OIS) eased notably (5-10bps) from yesterday…

{kind=link}

Source: Bloomberg

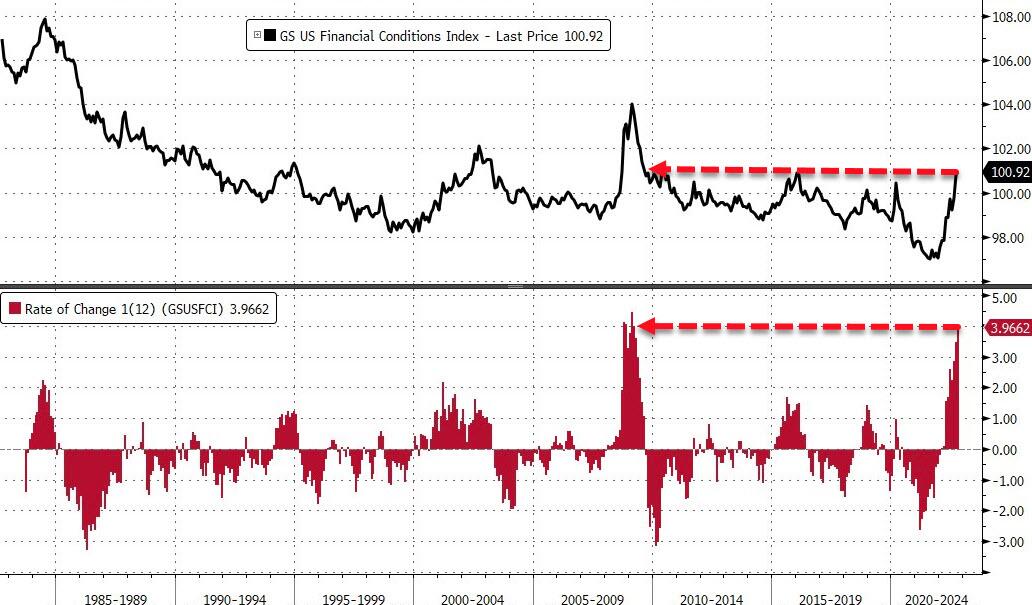

Has The Fed done enough damage? Financial Conditions are at their tightest (on a month-end basis) since July 2009 and the last 12 months has seen an almost unprecedented tightening of financial conditions…

{kind=link}

Source: Bloomberg

While The Fed was jawboning, The Bank of Japan (despite no comment) was clearly in the markets, smashing JPY almost 6 handles stronger after it crashed to 152/USD (in September the intervention sparked a 5.5 handle spike which was completely erased within 3 days)…

{kind=link}

Source: Bloomberg

Finance Minister Shunichi Suzuki, speaking to reporters this week, reiterated the country will take appropriate action against speculative moves.

“All the market talk is about intervention,” even though there’s no official confirmation, said Alan Ruskin, chief international strategist at Deutsche Bank AG.

“Intervention is only a short-term palliative in current circumstances.”

There’s no official confirmation of intervention, but it “smells like it for sure,” said Alex Etra, a senior strategist at Exante Data Inc. Intervention won’t stop the yen from weakening further because “they are rowing upstream against fundamentals: high energy prices and rate differentials,” he said.

Volumes in yen futures today were dramatically bigger than during the last major intervention…

{kind=link}

Kyodo separately reports the country’s top currency official, Masato Kanda, declined to comment on whether the country intervened when asked by reporters.

{kind=link}

But hey none of that matters because President Biden claims Republicans want to “crash the economy next year by threatening the full faith and credit of the United States…”?!

Joe Biden accuses Republicans of wanting to “crash the economy.” pic.twitter.com/d7iD9vt4Zv

— Townhall.com (@townhallcom) October 21, 2022

And after all that, US equities ripped higher today (Nasdaq was down over 1% in the pre-open, ended up over 2.5%)

{kind=link}

And US stocks had their best week since June (with Nasdaq outperforming)…

{kind=link}

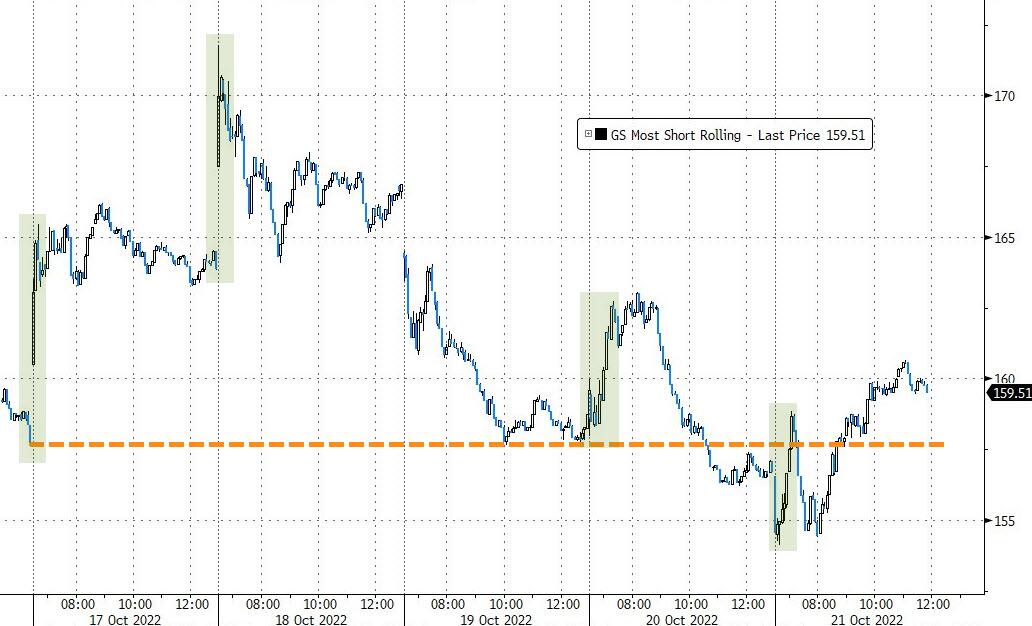

Interestingly, “most shorted” stocks were barely positive on the week…

{kind=link}

Source: Bloomberg

Perhaps even more notably, VIX was bid this afternoon as stocks soared – was the world and his pet rabbit buying calls (levered longs)?

{kind=link}

Source: Bloomberg

It appears so… S&P vol skew is at extremes (calls max bid over puts)…

{kind=link}

Source: Bloomberg

Credit markets are a bloodbath with LQD breaking back below $100 – the same level it traded at in Sept 2008 when Lehman collapsed and the credit market froze. For now, HYG is trading just marginally above the March 2020 COVID lockdown lows in price (when The Fed took the unprecedented action of buying junk bonds)…

{kind=link}

Source: Bloomberg

Thanks to today’s plunge in yields (with the short-end dramatically outperforming), 2Y yields ended the week -2bps while the long-end was up over 33bps…

{kind=link}

Source: Bloomberg

Today saw the yield curve (2s30s) steepen 20bps (the biggest daily steepening since March 2020) erasing most of the flattening (inversion) from September’s CPI print plunge. On the week, the curve steepened over 30bps – its biggest steepening since January 2009…

{kind=link}

Source: Bloomberg

For some context, this was the 12th straight week of 10Y yields increasing – equaling the record streak of all time from 1984…

{kind=link}

Yen’s gains today sent the dollar reeling to its worst day in almost 3 weeks and worst weekly drop since August…erasing all of its post-payrolls gains…

{kind=link}

Source: Bloomberg

Bitcoin puked back below $19000 this morning then ripped back above it on the dollar drop, dovish-ish FedSpeak. $19,000 seems like a key level now for over a month…

{kind=link}

Source: Bloomberg

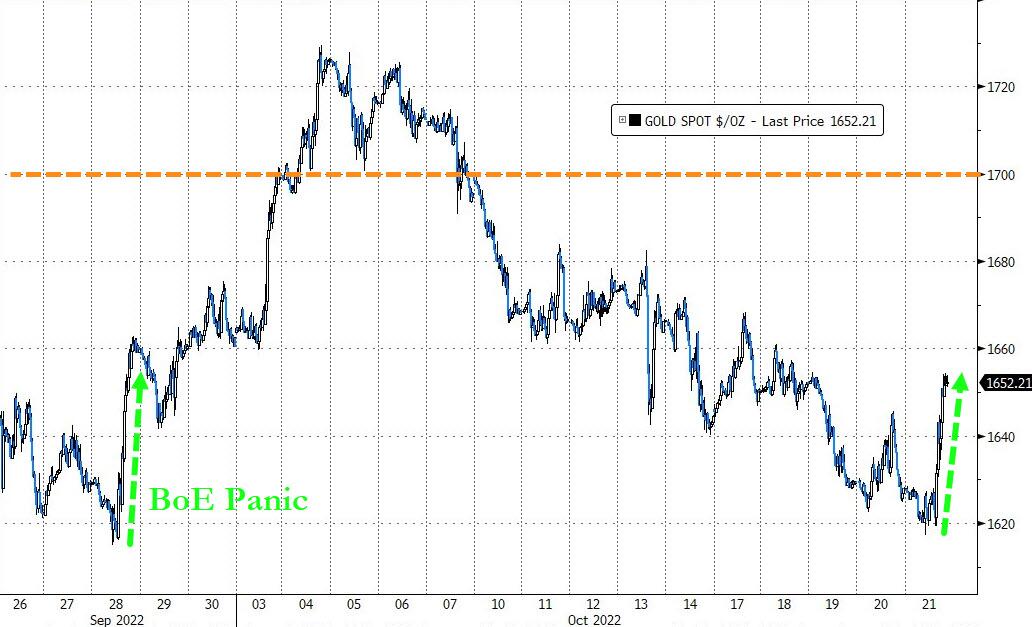

Gold saw its best day since the start of October today (finding support at Sept lows when the BoE panicked), pushing the precious metal higher on the week…

{kind=link}

Source: Bloomberg

Oil prices were flat on the week despite Biden’s promises with WTI ending around $85…

{kind=link}

Source: Bloomberg

Finally, here’s St.Louis Fed’s Jim Bullard explaining the situation to those who still don’t get it… “I would not call lower equity prices financial stress…”

{kind=link}

Source: Bloomberg

So, don’t hold your breath for a Fed Put reappearing anytime soon.

But this, on the other hand, could be a major problem, the all important FRA-OIS indicator of interbank funding stress (and money-market risk) is surging above 45bps (when The Fed last stepped in with unprecedented size to flood the lane during the COVID lockdowns)…

{kind=link}

Source: Bloomberg

In fact, on a month-end basis, FRA-OIS is at its most-stressed since Dec 2011

A very quick primer on this all important spread:

What is FRA? A forward rate agreement is a deal to swap future fixed interest payments for variable ones, or vice versa. The key rate for U.S. markets is the three-month London interbank offered rate, or Libor, in U.S. dollars. The benchmark is derived by major banks submitting rates based on transactions that are compiled to establish benchmark for five different currencies across seven different loan periods. Those benchmarks underpin interest rates on trillions of dollars of financial instruments and products from student and car loans to mortgages and credit cards.

What is OIS? The Overnight Index Swap rate is calculated from contracts in which investors swap fixed- and floating-rate cash flows. Some of the most commonly used swap rates relate to the Federal Reserve’s main interest-rate target, and those are regarded as proxies for where markets see U.S. central bank policy headed at various points in the future.

That’s the theory. But why does the FRA-OIS spread matter in practice?

Well, it’s regarded as the markets’ measure of how expensive or cheap it will be for banks to borrow in the future, as shown by Libor, relative to a risk-free rate, the kind that’s paid by highly rated sovereign borrowers such as the U.S. government. The FRA-OIS spread therefore provides another snapshot of how the market is viewing credit conditions because of the fact that traders are betting on where Libor-OIS – its underlying spread – will be.

As a further reminder, there are typically 3 reasons why it would blow out:

the risk premium for uncertainty of US monetary policy,

recently elevated credit spreads (CDS) of banks, and

demand for funds in preparation for market stress.

Whatever the reasons, a blow out in FRA/OIS means that dollar funding is becoming increasingly problematic, amid an ominous global dollar shortage.

In summary, if the FRA-OIS spikes another 10-15 points, the Fed will have no choice but to emerge from its paralysis and reassure markets that the financial system isn’t about to experience another paralysis… which is perhaps why all the sudden jawboning on rate-hikes and pauses are happening.

Never forget, we live in a world where “insider trading” is illegal, but Fed policy path leaks to Wall. St. Journal reporters move asset prices in the hundreds of billions of dollars.

— Lawrence McDonald (@Convertbond) October 21, 2022

Tyler Durden

Fri, 10/21/2022 – 16:01