42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Netflix Soars After Q3 Results, Subscriber Growth And Forecast All Tops Forecasts

Recent earnings reports from streaming giant Netflix had been a veritable horrorshow… until last quarter: the stock tumbled two years ago when the company reported a huge miss in both EPS and new subs, which at 2.2 million was tied for the worst quarter in the past five years, while also reporting a worse than expected outlook for the current quarter. This reversed seven quarters ago when Netflix reported a blowout subscriber beat and projected it would soon be cash flow positive, sending its stock soaring to an all time high – if only briefly before again reversing and then tumbling six quarters ago when Netflix again disappointed when it reported a huge subscriber miss and giving dismal guidance, leading to the second quarter when Netflix slumped again after the company missed estimates and guided lower. This again reversed one year ago when Netflix soared after it blew away expectations and guided to a blowout Q4, only to plummet three quarters ago when the company’s stock crashed after NFLX reported a dismal subscriber miss for Q4 and gave horrific guidance for the current quarter. Then two quarters ago, the stock absolutely imploded, plummeting 20% in seconds after the company reported the loss of 2 million subs in Q2 and forecast catastrophic earnings. Finally, one quarter ago when there was no more muscle to cut, the stock finally jumped after reporting a smaller than expected subscriber loss.

{kind=link}

Heading into the earnings, and based on Netflix’s published weekly Top 10 list, Wedbush Securities analyst Michael Pachter estimates viewing hours were up about 14% from a year earlier. That, according to Bloomberg, gave him confidence that Netflix is underestimating its subscriber growth. Pachter forecast 1.45 million new customers (turned out he was low). Meanwhile, Wells Fargo analyst Steven Cahall uses his own approach to calculate Netflix customer additions. He gets data on new Netflix app downloads from a service called Apptopia and compares those numbers with Netflix’s historical subscriber results. Based on that data, he’s forecasting 1.2 million new subscribers in the quarter (he was even lower).

In short, after the shares tumbled on 5 of the past 8 earnings releases, and have lost 60% of their value YTD – one of the most oversold tech stocks of 2022 – many said that purely based on statistics, NFLX is long overdue for a continuation bounce today.

And they were right: moments after the close, NFLX reported solid results for Q3 and a somewhat weak outlook but because the company’s streaming subs outlook was very strong, and expects the best quarter for subs in Q4 since a year ago, the stocks surged after hours.

Specifically, after Netflix had forecast one million more customers in the quarter, it got 2.41 million, more than enough to offset losses earlier in the year. The company cited new hits, including Monster: The Jeffrey Dahmer Story and Stranger Thing season four. “After a challenging first half, we believe we’re on a path to reaccelerate growth,” the company said in a letter to shareholders.

To be sure, there were some concerns, such as the company’s announcement that it will stop giving a forecast for subscriber growth starting in Q4, even though it will continue to provide revenue, operating income and net income guidance: “As discussed in previous letters, we are increasingly focused on revenue as our primary top line metric,” Netflix said in its letter. Traditionally, this is viewed as a death knell to growth, but for now the market is giving NFLX a pass.

Here are the details (from the letter to shareholders):

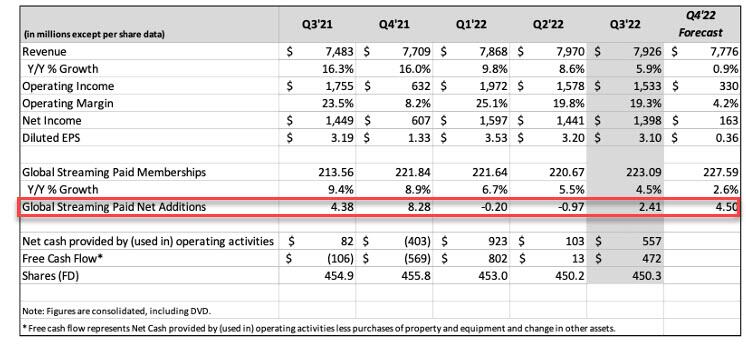

Q3 revenue $7.93BN, +5.9% Y/Y, and beating the median exp of $7.85BN

Q3 EPS $3.10, down modestly from $3.19 Y/Y, but also beating the median exp. $2.12

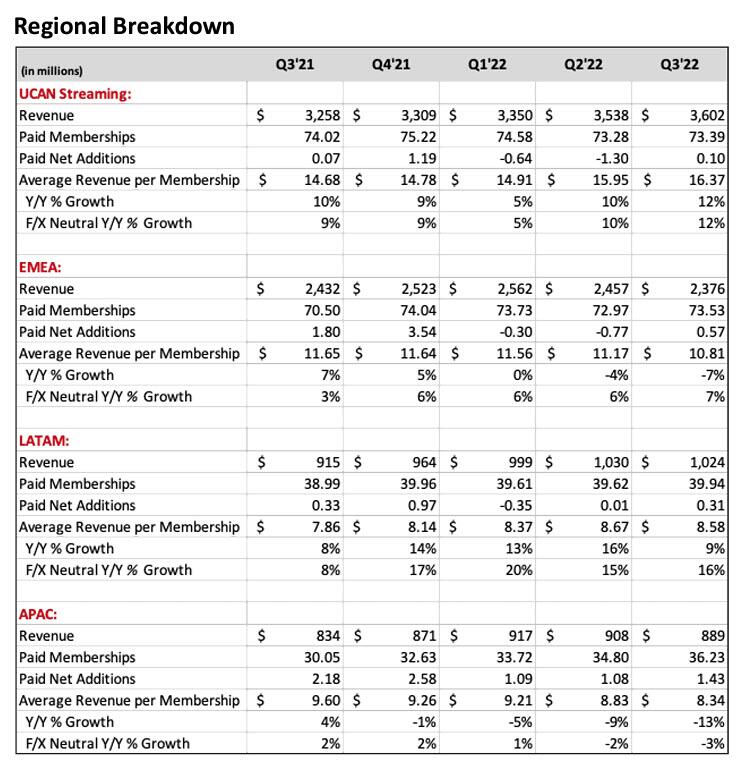

Streaming paid net change +2.41MM smashing the Exp. +1 M. The company beat subs in all four regions:

US/Canada streaming paid net change +100,000, +43% y/y, beating the estimate 271,376 million

EMEA streaming paid net change +570,000, -68% y/y, beating the estimate +12,640

LATAM streaming paid net change +310,000, -6.1% y/y, beating the estimate +219,320

APAC streaming paid net change +1.43 million, -34% y/y, beating the estimate +1.3 million

Streaming paid memberships 223.09MM, +4.5% Y/Y, beating the exp. 221.7MM

Operating margin 19.3% vs. 23.5% y/y, estimate 15.9%

Operating income $1.53 billion, -13% y/y, estimate $1.26 billion

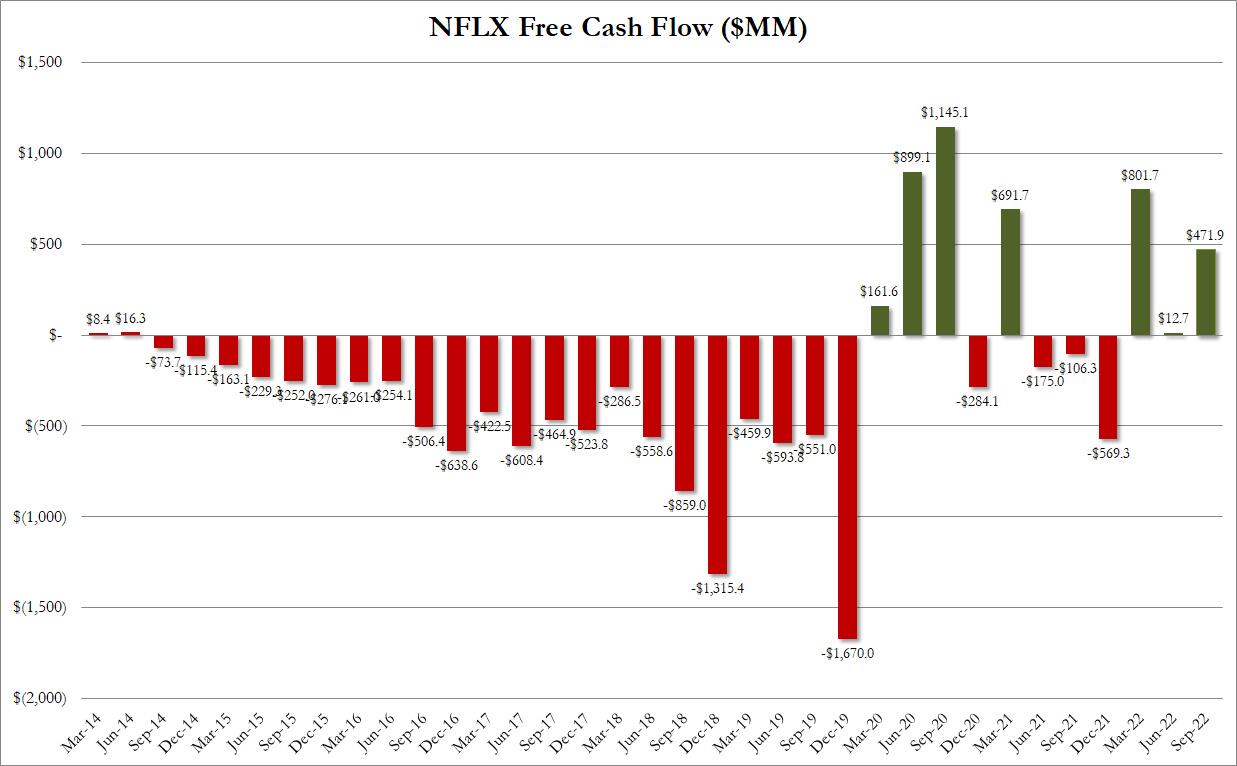

Free cash flow $472 million vs. negative $106 million y/y, beating the median est. of $184.2 million

{kind=link}

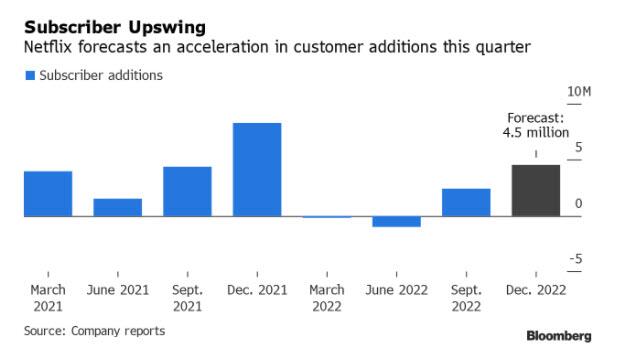

The good news: after two quarter of subscriber declines, the company finally saw a rebound in Q3.

More importantly, Netflix now forecasts that it will see even more growth in Q4 and will add a whopping 4.5 million subscribers, well above the est. 3.9 million. The bad news – the associated revenue and EPS will be less than expected due to FX headwinds: the company’s a 36-cents-per-share profit is well below the street’s estimate of $1.20. Looking ahead the company also expects the following Q3 metrics:

Q4 revenue $7.78BN, missing the consensus exp. $7.98BN

Q4 streaming paid subscribers +4.5MM, beating the estimate of 3.9 million

Q4 EPS 36c, missing the exp. $1.20

{kind=link}

Here is the bottom line, and what everyone will be focusing on today: Netflix is growing again: the streaming giant added 2.41 million customers in the third quarter, more than doubling internal forecasts and Wall Street expectations. Netflix grew in all regions and said it expects to sign up another 4.5 million globally this period.

{kind=link}

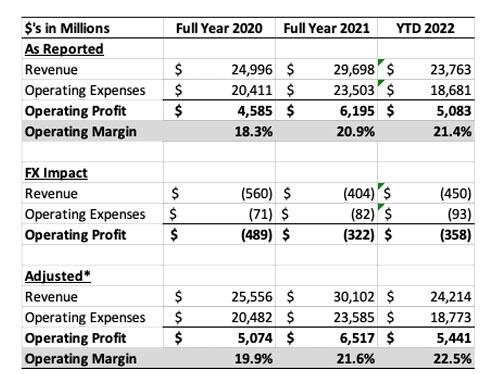

Additionally, after warning last quarter that FX would hit earnings, NFLX said that “to provide additional transparency around our operating margin, we disclose each quarter our year-to-date (YTD) operating margin based on F/X rates at the beginning of each year. This will allow investors to see how our operating margin is tracking against our target (which was set in January of 2022 based on F/X rates at that time), absent intra-year fluctuations in F/X.”

{kind=link}

Why the table above? Because NFLX was quick to explain that the sequential decline in revenues was was entirely due to FX:

Our 6% year-over-year revenue growth in Q3 was driven by a 5% increase in average paid memberships and a 1% rise in ARM. Excluding the impact of foreign exchange (F/X), revenue and ARM grew 13% and 8% year-over-year, respectively. The sequential decline in revenue was entirely due to F/X. We under-forecasted paid net additions, which totaled 2.4 million vs. our 1.0m forecast and compared to 4.4m in the year ago quarter.

In APAC, revenue grew 19% excluding F/X as average paid memberships rose 23% year-over-year. ARM was -3% year-over-year, excluding F/X, partially driven by lower ARM in India, somewhat offset by higher ARM in Australia and Korea. We added 1.4m paid memberships in the region (vs. 2.2m last Q3).

Excluding F/X, EMEA revenue and ARM grew 13% and 7%, respectively. Paid net adds totaled 0.6m vs. 1.8m in the year ago quarter.

In LATAM, revenue increased 19% year-over-year, supported by ARM growth of 16% vs. the year ago quarter excluding F/X. We added 0.3m paid memberships, in-line with membership growth in Q3’21.

In UCAN, our most penetrated market, ARM and revenue grew by 12% and 11%, respectively, excluding F/X. Paid net adds totaled 0.1m (similar to the 0.1m in Q3’21).

Looking ahead, NFLX also sees challenges due to the soaring USD:

The appreciation of the US dollar remains a significant headwind for us (and US-based multinationals in general). For Q4’22, we’re expecting revenue of $7.8 billion with the sequential decline entirely due to the continued strengthening of the US dollar vs. other currencies. On a constant currency basis, this equates to 9% year-over-year revenue growth. Our revenue growth forecast is driven by our expectation for 4.5m paid net adds (vs. 8.3m in Q4’21) and ARM growth of 6% year-over-year, excluding F/X. Our paid net adds forecast assumes that we experience our usual seasonality as well as the impact of a strong content slate, counterbalanced by macroeconomic weakness which leads to less-than-normal visibility.

Away from premium subs, the new ad-supported tier is unlikely to add much to sales in 2022 as the business ramps up, Netflix said:

While we’re very optimistic about our new advertising business, we don’t expect a material contribution in Q4’22 as we’re launching our Basic with Ads plan intra-quarter and anticipate growing our membership in that plan gradually over time. Our aim s to give our prospective new members more choice – not switch members off their current plans. Members who don’t want to change will remain on their current plan, without ads, at the current price

Netflix also says it’s on track to meet its 2022 and 2023 operating margin target of 19% to 20%. However, if the US dollar remains strong it may fall short of that goal. The company insists it can adjust its pricing and cost structure if the dollar stays at its current level.

As a reminder, our 2022 and 2023 operating margin target of 19%-20% is based on F/X rates in January 2022, as we discussed in our Q4’21 letter and subsequent earnings calls. We’re on track to meet this F/X neutral operating margin objective for 2022 (excluding the $150m of restructuring costs in Q2) and for 2023. With the appreciation of the US dollar though, our reported operating margin would be lower than 19%-20% should the US dollar remain above January 2022 levels relative to other currencies.

Over the medium term, we believe we can adjust our pricing and cost structure for a stronger US dollar world. Our long term goal remains unchanged – to sustain double digit revenue growth, increase operating profit even faster (as we expand margins) and deliver growing positive free cash flow.

Next, this is how NFLX revealed that it is stopping its paid subscriber guidance:

As discussed in previous letters, we are increasingly focused on revenue as our primary top line metric. This will become particularly important heading into 2023 as we develop new revenue streams like advertising and paid sharing, where membership is just one component of our revenue growth. So starting with our Q4’22 letter in January of 2023, we’ll continue to provide guidance for revenue, operating income, operating margin, net income, EPS and fully diluted shares outstanding for the following quarter, but not paid membership. Similar to our regional membership disclosure, we’ll continue to report our global and regional membership each quarter as part of our earnings release.

Digging further though its Q3 letter, Netflix touts the benefits of its content model: “We think our bingeable release model helps drive substantial engagement, especially for newer titles.” It notes shows including Monster: The Jeffrey Dahmer Story have benefited from it, and that it would be difficult to imagine Squid Game becoming the global phenomenon that it did had subscribers not been able to binge it in one go.

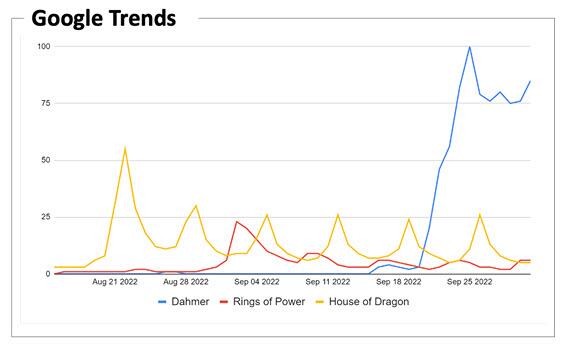

The company also repeated that its “bingeable release model” helps drive substantial engagement, especially for newer titles. This enables viewers to lose themselves in stories they love. As the Google Trends chart shows, the ability to watch all of Monster: The Jeffrey Dahmer Story helped drive significant interest in the show.

{kind=link}

Some more insights on its content from the NFLC letter:

It’s hard to imagine, for example, how a Korean title like Squid Game would have become a mega hit globally without the momentum that came from people being able to binge it. We believe the ability for our members to immerse themselves in a story from start to finish increases their enjoyment but also their likelihood to tell their friends, which then means more people watch, join and stay with Netflix.

Our Q3 content slate was especially strong. In English scripted TV, we kicked off the quarter with Stranger Things S4, which generated 1.35 billion hours viewed- our biggest season of an English 4 language series ever. This was followed in August by The Sandman (351 million hours viewed), which was loved by fans and critics alike. Near the end of the quarter, we launched season five of fan favorite Cobra Kai (270 million hours viewed) and limited series Monster: The Jeffrey Dahmer Story* (824 million hours viewed) from Ryan Murphy, which is now our second largest English series

A quick update on NFLX gaming:

We’re coming up on the one year anniversary of our gaming launch. As we’ve said, this will be a multi-year journey for us to learn how to please game players. Our first year was about establishing our gaming infrastructure and understanding how our members interact with games. We now have 35 games on service (all included in every Netflix subscription without in-game ads or in-app purchases) and we’re seeing some encouraging signs of gameplay leading to higher retention.

With 55 more games in development, including more games based on Netflix IP, we’re focused in the next few years on creating hit games that will take our game initiative to the next level. More generally, we see a big opportunity around content that crosses between TV or film and games. For example, after the launch of the anime Cyberpunk: Edgerunners (49 million hours viewed) in Q3 use of CD Projekt’s game surged on PCs.

Here is NFLX on the one thing everyone is looking for more information on, pricing and the new ad-supported tier, as well as “sharing” of accounts:

As we’ve been discussing over the past few quarters, improving our pricing strategy is an important near-term focus. Last week, we announced that we’ll be launching an ad-supported subscription plan on November 1 in Canada and Mexico; November 3 in Australia, Brazil, France, Germany, Italy, Japan, Korea, the UK, and the US; and November 10 in Spain. Cumulatively, these 12 markets account for ~$140 billion of brand advertising spend across TV and streaming, or over 75% of the global market.

To start, we’re keeping it simple by offering one low-priced ad plan – Basic with Ads – at a price that’s 20%-40% below our current starting price. So in the US, for example, Netflix will now start at $6.99 per month (compared to $9.99 today). The Basic with Ads plan will have ~5 minutes of advertising per hour, frequency capping and strong privacy protections.

The reaction from advertisers so far has been extremely positive and we believe that more choice, especially for more price conscious consumers, will translate into meaningful incremental revenue and operating profit over time. That said, it’s still very early days and, since we’re keeping our existing plans ad-free, it will take us time to build up our membership base and the associated ad revenue.

Finally, we’ve landed on a thoughtful approach to monetize account sharing and we’ll begin rolling this out more broadly starting in early 2023. After listening to consumer feedback, we are going to offer the ability for borrowers to transfer their Netflix profile into their own account, and for sharers to manage their devices more easily and to create sub-accounts (“extra member”), if they want to pay for family or friends. In countries with our lower-priced ad-supported plan, we expect the profile transfer option for borrowers to be especially popula

Some amusing math when it comes to competition, which NFLX says is not only not making money but is burning through billions:

As it’s become clear that streaming is the future of entertainment, our competitors – including media companies and tech players – are investing billions of dollars to scale their new services. But it’s hard to build a large and profitable streaming business – our best estimate is that all of these competitors are losing money on streaming, with aggregate annual direct operating losses this year alone that could be well in excess of $10 billion, compared with our +$5-$6 billion of annual operating profit. For incumbent entertainment companies, this high level of investment is understandable given the accelerating decline of linear TV, which currently generates the bulk of their profit.

Ultimately though, we believe some of our competitors will seek to build sustainable, profitable businesses in streaming – either on their own or through continued industry consolidation. While it’s early days, we’re starting to see this increased profit focus – with some raising prices for their streaming services, some reigning in content spending, and some retrenching around traditional operating models which may dilute their direct-to-consumer offering. Amidst this formidable, diverse set of competitors, we believe our focus as a pure-play streaming business is an advantage. Our aim remains to be the first choice in entertainment, and to continue to build an amazingly successful and profitable business.

Finally, looking at what had traditionally been NFLX’s weakest link, cash flow, it had this to say:

Net cash generated by operating activities in Q3 was $557 million vs. $82 million in the prior year period. Free cash flow (FCF) amounted to $472 million, compared with -$106 million in Q3’21. We continue to expect FCF of +$1 billion for the full year 2022, plus or minus a few hundred million dollars and substantial growth in FCF in 2023 (assuming no further material appreciation of the US dollar) . Gross debt at quarter end was $14 billion, within our $10-$15 billion target range. Cash increased $300 million sequentially to $6.1 billion. Net debt amounted to $7.9 billion at the end of Q3’22, or 1.2x LTM EBITDA. We have no debt maturities in 2023. In early October, we closed our previously announced acquisition of leading animation studio Animal Logic. We funded the transaction with cash, which will be reflected in our Q4’22 cash flow statement.

{kind=link}

In kneejerk reaction the stock, which had been pummeled in most recent quarters, pushing the stock 60% lower on the year, has soared as much as 15% higher on the solid subscriber beat and guide, and is back to the highest level since April, while also lifting Nasdaq futures and its peer group consisting of Walt Disney, Warner Bros, Discovery and Paramount.

{kind=link}

Tyler Durden

Tue, 10/18/2022 – 16:26