42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

On The Path To Hyperinflation

Authored by Tuomas Malinen via The Epoch Times,

I have had a series of conversations lately on how did we, the world, get to this point? I think that it’s a valid question, considering how well things were in the 1990s after the Soviet Union had collapsed.

The really interesting follow-up question is: Has this deterioration been a series of mere random events, or have we been somehow guided to this point?

{kind=link}

I think there have been two major “game changers”: the 9/11 terrorist strikes and the global financial crisis of 2008–09 (GFC). If you really consider the aftermath of these events, it’s rather clear that we never really returned to the status quo after either.

The 9/11 terrorist attacks started an escalating series of conflicts around the world, which have now turned into a Russian–Ukrainian war. I have my own worries that the war in Ukraine is, in veritate, not proceeding as presented in the Western media, which is likely to rather strongly follow the Ukrainian propaganda. As the late California Republican Senator Hiram Johnson once said, in 1918: “The first casualty when war comes is truth.” I have detailed my doubts in my newsletter.

The global financial crisis, on the other hand, changed our economic landscape, rather permanently, which is now converging with the war-related costs to create an extremely precarious economic situation.

If someone had told me in the early 2000s that in in the 2010s, central banks, led by the Federal Reserve, would be buying hundreds of billions’ worth of government bonds each month, I would have wished him/her a nice trip to an asylum. The mere idea would have sounded so preposterous at the time. But after the financial crisis—there we were.

The Federal Reserve started the asset purchases on Nov. 25, 2008, and slowly but surely all major central banks followed. It became the biggest central bank money-conjuring operation in history!

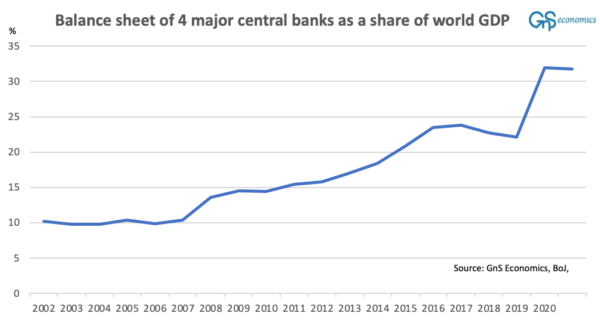

In 2020, the size of the combined balance sheet of the four largest central banks—the Bank of Japan, the Federal Reserve, the European Central Bank, and the People’s Bank of China—reached an insane 32 percent of the gross domestic product of the world.

{kind=link}

A figure presenting the balance sheet of the four largest central banks as a share of the gross domestic product of the world. (GnS Economics / Bank of Japan / European Central Bank / People’s Bank of China / Federal Reserve Bank of St. Louis / International Monetary Fund)

Like I have been detailing, this had some serious repercussions for the financial markets and the real economy (see, e.g., this, this and this).

However, the main point to understand is that if you artificially and vastly increase the amount of money in circulation, it will increase prices. This may occur with a lag, meaning that money may increase considerably without causing any noticeable increase in the price level. Then a supply-side shock, like an oil shock, hits and prices start to rise.

Combined with the greatly increased money in circulation, this shock, if it persists, will put in motion a process whereby prices increase but the demand will not come down, because it is supported by the vast amounts of money slushing around in the economy. When a sustained demand meets ailing supply, prices naturally continue rising. Then consumers will notice that the purchasing power of their wages is declining, and they start to demand higher salaries. At this point, fast inflation becomes self-sustaining. This process can be further supported by government subsidies and support.

This is the self-sustaining process of inflation central banks helped to create.

As I explained previously, this is not “President Putin’s inflation” but central bankers’ and governments’ inflation. The thing is that almost every Western government helped to create the inflation crisis by artificially sustaining demand during a time when supply was artificially constrained because of lockdowns through stimulus checks and other such schemes.

{kind=link}

A figure presenting the development of the M2 (broad money) money aggregate consisting of currency and coins held by the non-bank public, savings deposits (including money market deposit accounts), small time deposits under $100,000, and shares in retail money market mutual funds in the United States in billions of dollars. (GnS Economics / National Bureau of Economic Research / Federal Reserve Bank of St. Louis)

We in Europe are about to fulfill two preconditions for one of the most destructive economic phenomenon known to man: hyperinflation.

The ravaging inflations in the Weimar Republic during the early 1920s, in Russia in the early 1990s, and in Zimbabwe in 2007–15 taught us that the two preconditions for a rapid decline in the value of money—hyperinflation—were and are:

The creation of vast amounts of central bank credit (money). (Check!)

The diminution of production capabilities to a serious degree. (Almost there.)

At the end, hyperinflation is always, always, a political decision. While the diminution (or “destruction”) of production capabilities can be caused by a nonpolitical force (like an earthquake), usually it is caused by an abrupt political-induced shock, like war and/or sanctions.

There is also very little other than political reasons to keep printing—that is, creating vast amounts of central bank credit (money)—for an extended period of time.

During the Weimar Republic and in Russia during the early 1990s, both governments decided that instead of painful reforms and a likely default, they would try to uphold national demand and production by monetizing their budget deficits. In Zimbabwe, the reasons were a bit more numerous, but all the problems were met by more deficit financing by the government.

In the process of monetization, a central bank usually buys the debt issued by the finance ministry (or Treasury), and the central bank then nullifies the value of the bonds, which creates a loss, which is then covered by issuing new currency notes (physical or digital) to reconcile its balance sheet, which increases money in circulation. Government uses this newly created money to sustain its consumption, provide subsidies and different schemes, like job guarantees.

Then, sustained or even growing demand combined with increasing money in circulation meet declining production, leading to a very rapid pace of inflation. As inflation accelerates, consumers, firms, and workers start to expect ever-higher inflation, which, combined with the quickly increasing supply of money from the central bank, destroys public faith in the currency. A hyperinflation emerges, which is technically defined as a 50 percent monthly increase in consumer prices.

Central banks have already done their “job” on this path, by vastly increasing the money in circulation; but they could make it exponentially worse by ending monetary tightening. This especially is relevant as governments in Europe are pouring bailout money to households and governments, which will artificially sustain demand in a situation, where high prices would push down the demand. At the same time, industrial production in Europe is shutting down. Europe is effectively facing a process of deindustrialization.

This combination—excess money, growing government spending, and falling production—is the exact recipe for a ravaging inflation.

The real tragedy is that we have had all the knowledge necessary to avoid the creation of vast asset market bubbles and fast inflation, but our leaders have refused to listen to the (true) experts, economics and economic history. Now, if our policymakers in Europe, or elsewhere, push us into a hyperinflation, we don’t have to wonder anymore about the question I posed above.

Because in that case, our political leaders are either utterly incompetent or they are deliberately trying to destroy our living standards.

And if that point is reached, they all need to go.

Tyler Durden

Sat, 10/08/2022 – 16:45