42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Goldman Throws In The Towell: Slashes S&P Price Target To 3,600… Warns Of Recesion Crash To 3,150

Less then a week after Goldman slashed its 2022 GDP forecast to stagnation (i.e. 0% growth) hinting that a recession was on deck…

{kind=link}

…and just two days after we reported that Goldman’s chief equity strategist David Kostin launched a trial balloon, telling clients that even as he still has a 4300 year-end price target on the S&P500, he saw the broad index tumbling as low as 2,900 in a recession, when we commented that “and there is your bogey: within 2-3 months, right after the BLS discovers the “mistakes” it had been making in its labor model and rectifies them sending the US in a brutal recession, expect Goldman to slash its optimistic 4,300 price target to one at or below 3,000 as a recession now becomes the bank’s base case scenario”, overnight Goldman did just that, and while it has yet to cut to 3,000 – after all a recession is still not the bank’s base case, but it will be in a few weeks – David Kostin, who has been dead wrong about pretty much everything over the past year (his initial 2022 year-end forecast was 5,100 set last November) just slashed his year-end S&P target from 4,300 to a whopping 3,600, which is not just almost 20% lower but is below the market’s current price!

And while there is a lot of detail in the full pdf (available to pro subs in the usual place), detail which clearly wasn’t relevant as recently as yesterday when stocks were plunging and Goldman still was forecasting a bounce to 4300, the bottom line according to Kostin is that it’s all the surging interest rates’ fault and more specifically, real yields, to wit: “the expected path of interest rates is now higher than we previously assumed, which tilts the distribution of equity market outcomes below our prior forecast.” Here, laughably Kostin pretends he was actually right all along, saying that “the S&P 500 index actually reached our previous year-end target of 4300 in mid-August”, even though rather sadly Kostin never told clients to sell there.

In any case, since the rate complex subsequently shifted dramatically, the Goldman strategist now says that “the higher interest rate scenario that we now incorporate into our valuation model supports a P/E of 15x (vs. prior forecast of 18x) and implies a year-end (3-month) S&P 500 target of 3600 (-5%) and 6-month and 12-month forecasts of 3600 (-5%) and 4000 (+6%).“

Some more details from the Goldman report:

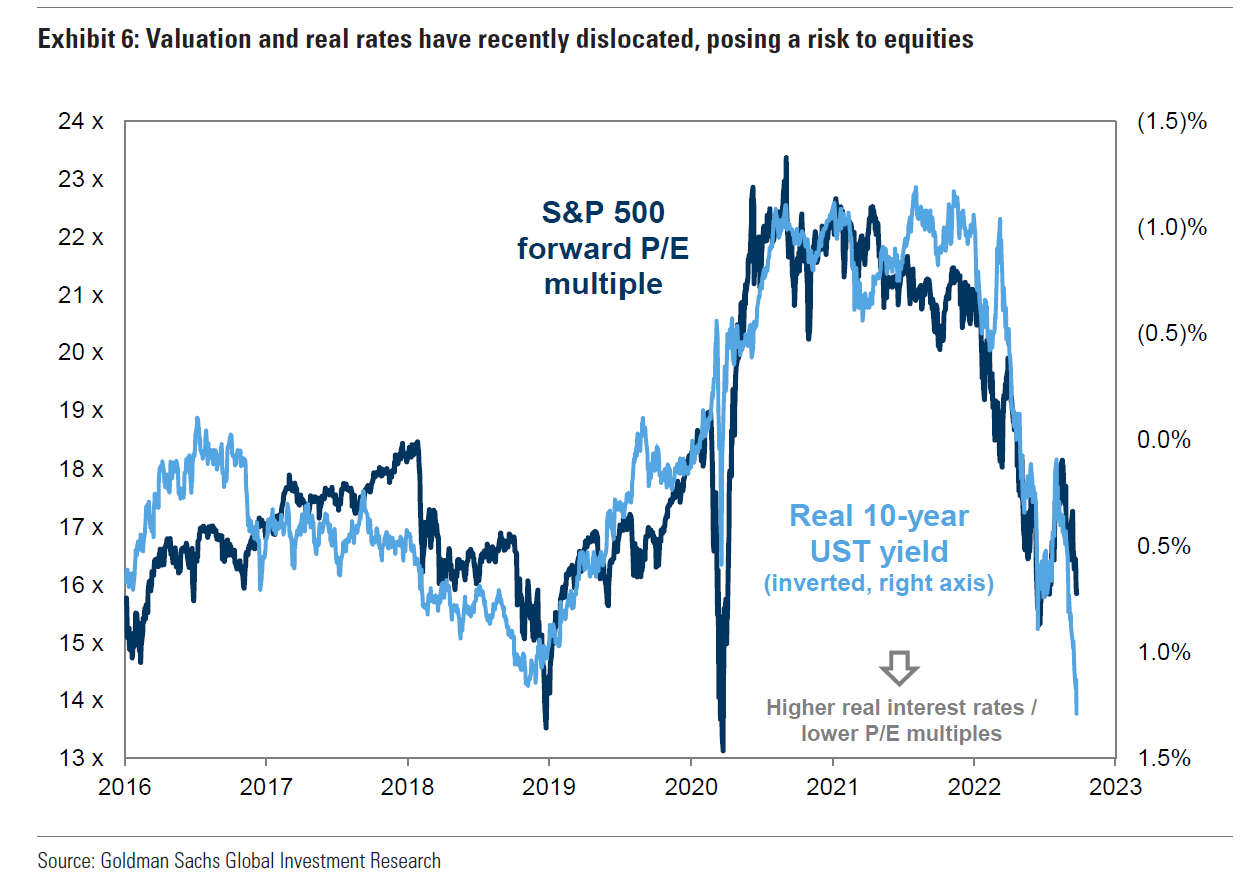

Equity valuations have closely tracked real interest rates until recently. Real yields have soared from 0.4% to 1.3% during the past month and could reach 1.5% by year-end. For context, real yields were negative 1% at the start of the year when the S&P 500 index hit an all-time high of 4800 and traded at a P/E of 21x. The tightest yield gap between equities and rates since the pandemic further tilts the balance of risks to the downside.

Indicatively, this is a chart we have shown frequently in recent weeks, and here is the latest incarnation. Needless to say, it suggests much more pain in store:

{kind=link}

Anyway, back to the Goldman report which looking ahead, says that “the outlook is unusually murky” and that most of the bank’s clients expect a hard-landing:

The forward paths of inflation, economic growth, interest rates, earnings, and valuations are all in flux more than usual with a wider distribution of potential outcomes. Based on our client discussions, a majority of equity investors have adopted the view that a hard landing scenario is inevitable and their focus is on the timing, magnitude, and duration of a potential recession and investment strategies for that outlook.

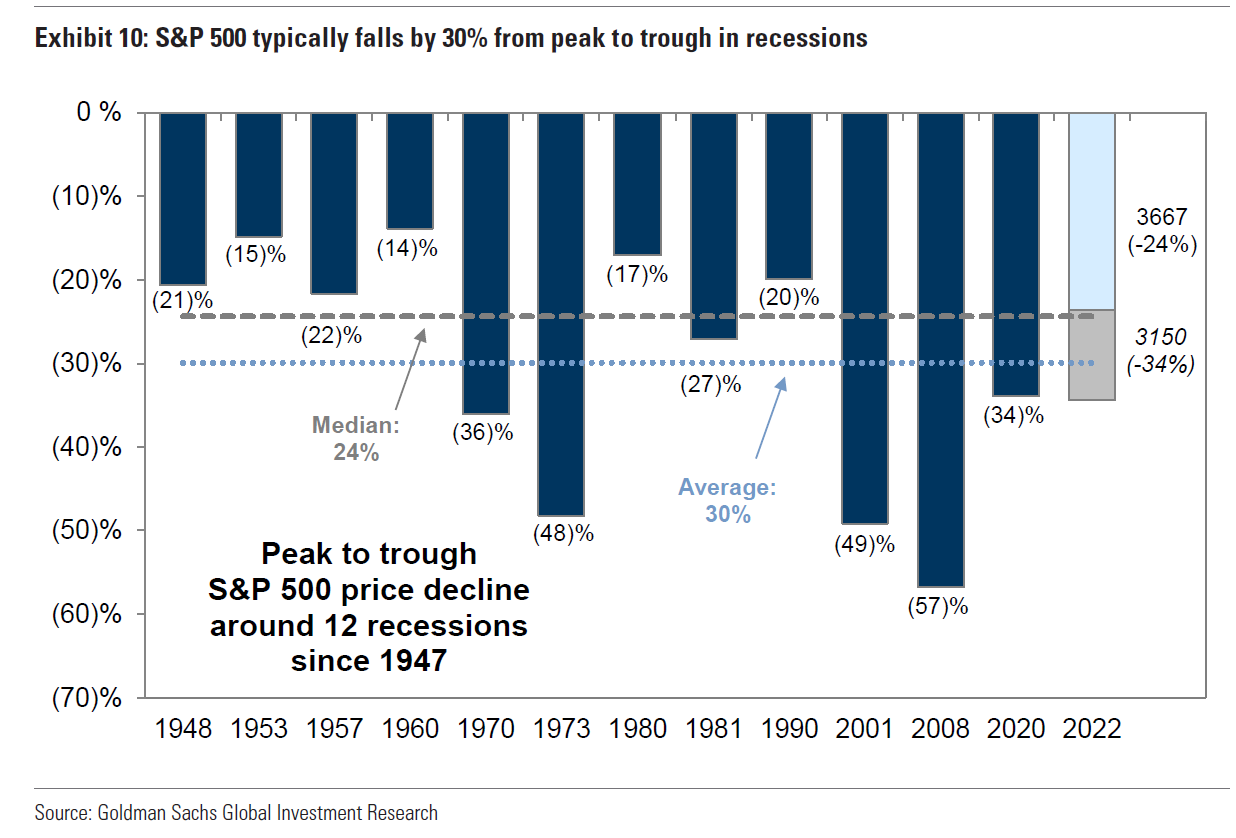

Finally, and as we warned earlier this week, Goldman once again very strongly hints that in a recession scenario – which is now inevitable and just a matter of Goldman flipping a switch once it gets the green light from the corner office – the S&P would tumble as low as 3,150:

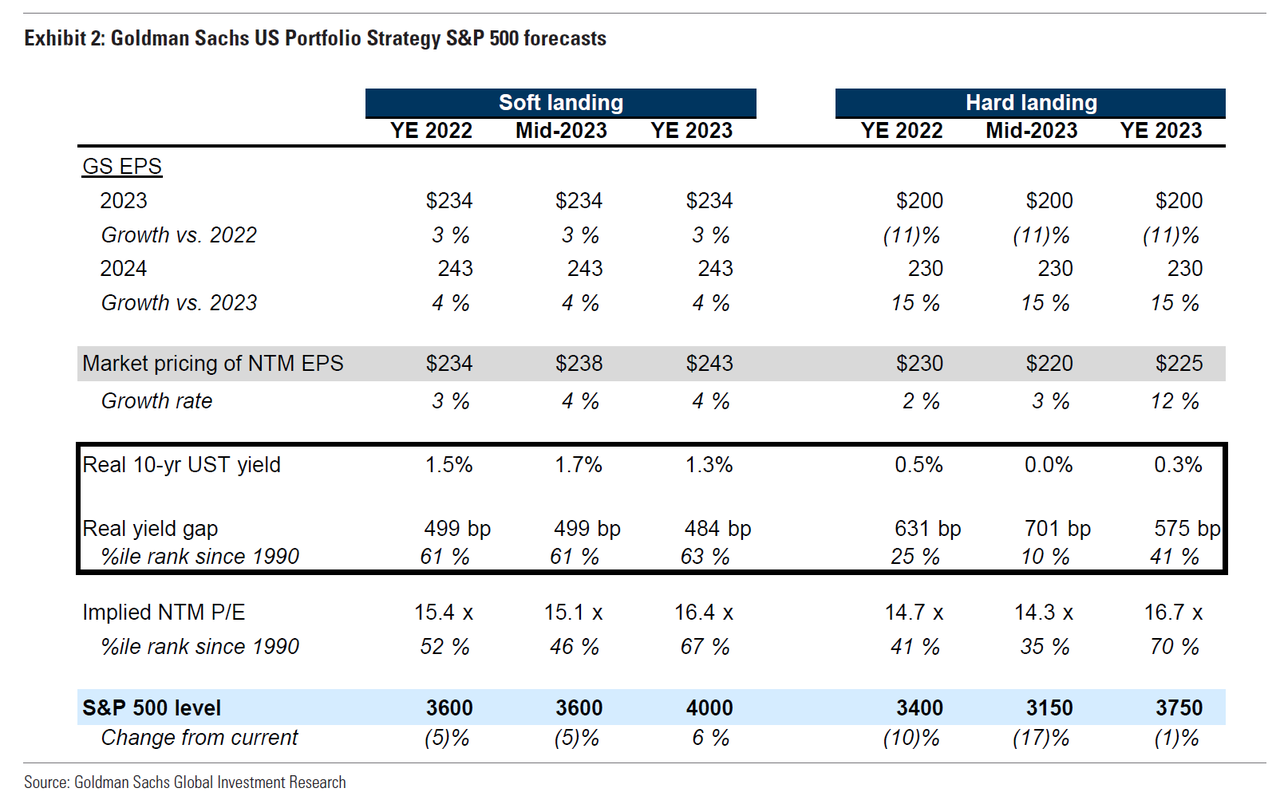

We previously published that in a recession falling S&P 500 EPS could cause the index to decline to 3150 (-17%). A 11% drop in EPS would be consistent with modestly negative real GDP growth and the 13% median EPS drop during prior recessions. Under a “hard landing” scenario, the yield gap would rise and the 3-, 6-, and 12-month S&P 500 targets would be 3400 (-10%) / 3150 (-17%) / 3750 (-1%).

Some more details on this “hard landing” scenario:

In a recession, we forecast earnings will fall and the yield gap will widen, pushing the index to a trough of 3150. Our economists assign a 35% probability of recession in the next 12 months and note that any recession would likely be mild given the lack of major financial imbalances in the economy. As we previously outlined, in the event of a moderate recession, our top-down model indicates EPS would fall by 11% to $200. However, prices move faster than analyst estimates, so we assume the market prices earnings of $220, halfway between consensus today and our recession earnings. Our 2024 EPS estimate assumes a 15% recovery in EPS to $230 which is similar to prior post-recession profit rebounds. From a valuation perspective, we assume real rates would fall to 0% as the Fed moves to cut rates and our yield gap model suggests a widening to 700 bp. The implied forward P/E multiple of the index would equal 14x.

For context, a 34% peak-to-trough decline in the S&P 500 index during a recession would only be slightly worse than the historical average of 30%. We see two risks that would create a more dramatic sell-off in equities during a recession. First, if inflation concerns were to limit the degree of monetary or fiscal policy support and interest rates did not fall, it could lead to even lower valuations or even larger economic and earnings growth declines than we model. Second, concentrated sector weakness, such as Information Technology in 2001 and Financials in 2008, could lead to an even sharper earnings and price decline.

{kind=link}

Actually, Kostin may not know, but one of his global equity strategist colleagues, Dominic Wilson has an even lower S&P target of as low as 2,900 in a global recession scenario, one is now inevitable, but as we said before, Goldman will wait the requisite 2 months until after the midterms before it tells the truth about what is coming.

Here is the full breakdown of Goldman’s soft and hard-landing scenarios…

{kind=link}

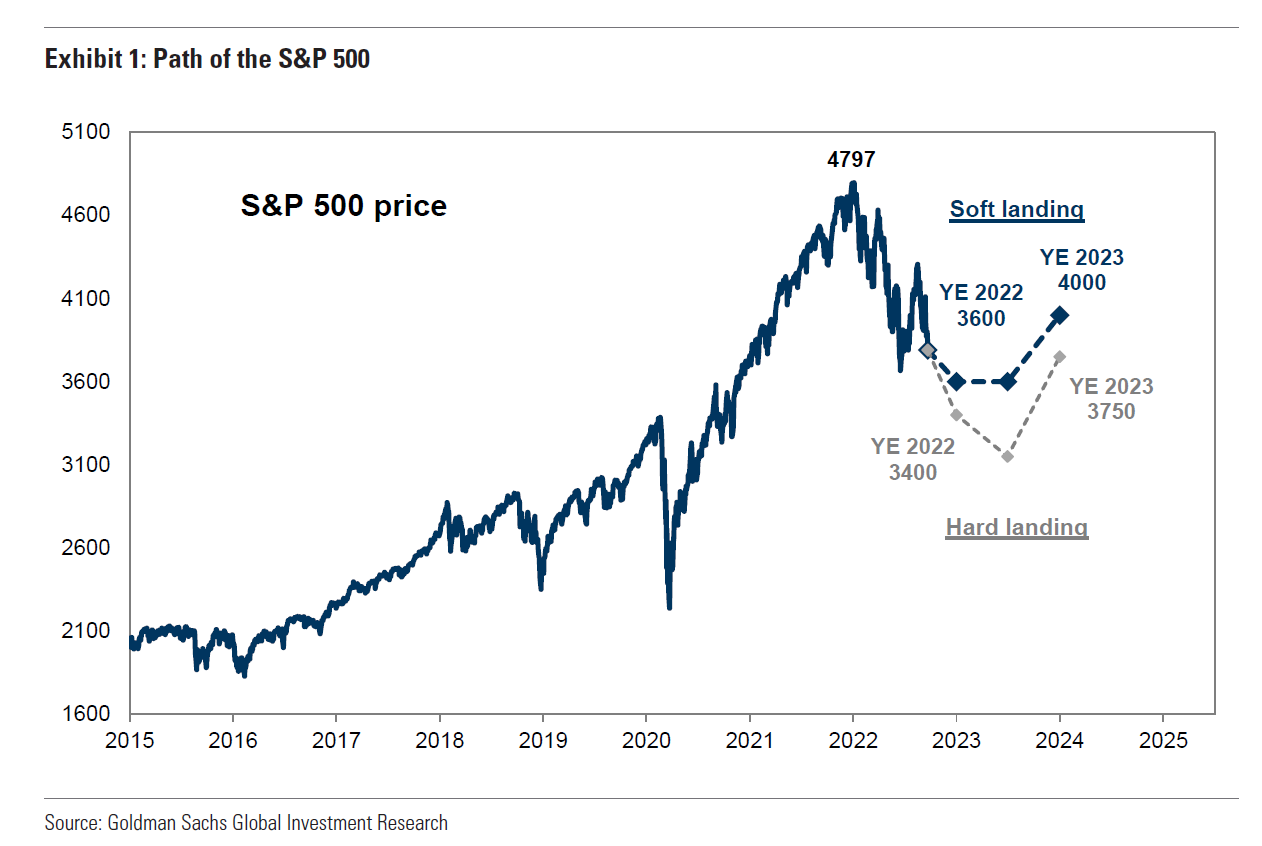

… as well as the visual breakdown of how the S&P’s “path” over the next year looks like according to Goldman:

{kind=link}

One final point: looking ahead, Kostin finally fully agrees with Morgan Stanley’s Michael Wilson – who long ago predicted the collapse in P/E multiples and has been focusing instead on the plunge in earnings – and writes that “in the near term, investor focus will soon turn from valuation to earnings. The surprisingly high August inflation reading was a pivotal event for macro investors regarding the path of Fed hikes. The analogue for stock investors is 3Q earnings season where record high profit margins will be under scrutiny.”

Couple final observations: while it will come as news to many that Goldman has flip-flopped from one of the most bullish to one of most bearish banks on Wall Street, those who had been reading the notes and comments that we publish from the bank’s Sales and Trading and flow desk, knew long ago that this bearish pivot was coming and none of this should come as a surprise. Perhaps more importantly, now that even Goldman has turned bull bear, the bottom may finally be in sight, because if Goldman’s base case is to urge all, not just a handful of its best clients, to sell, then the bank’s traders are officially buying everything that is thrown their way…

More in the full report available to pro subs.

Tyler Durden

Fri, 09/23/2022 – 06:40