42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Four Things Traders Will Be Watching For From The Fed Today

Authored by Ven Ram, Bloomberg cross-asset strategist,

Treasury traders will assess how hawkish the Federal Reserve really is when we get an update of its dot plot today.

{kind=link}

In particular, this is what they will be carefully parsing:

1. Size of increase & margin of vote:

Speculation has been rife about the size of increase we will get from the Fed. The faster-than-forecast inflation print for August spurred bets that the monetary authority may opt for a full percentage-point increase in its benchmark rate. However, it must be acknowledged that there is a world of difference between what the Fed should do and what it will do. Given that there have been zero rebuttals from the Fed in the form of media leaks in the run-up to the meeting to what may be thought of as the base case, it would make sense that the markets should be prepared for a 75-basis point increase today.

I don’t expect any hawkish dissent at today’s review, including from St. Louis Fed President James Bullard. He eschewed suggestions of a bigger increase in the run-up to the July meeting. However, a dissent vote calling for a smaller hike is possible. Esther George, who voted for a 50-basis point increase in June, may do an encore. Lisa Cook is also reputed to be a dove.

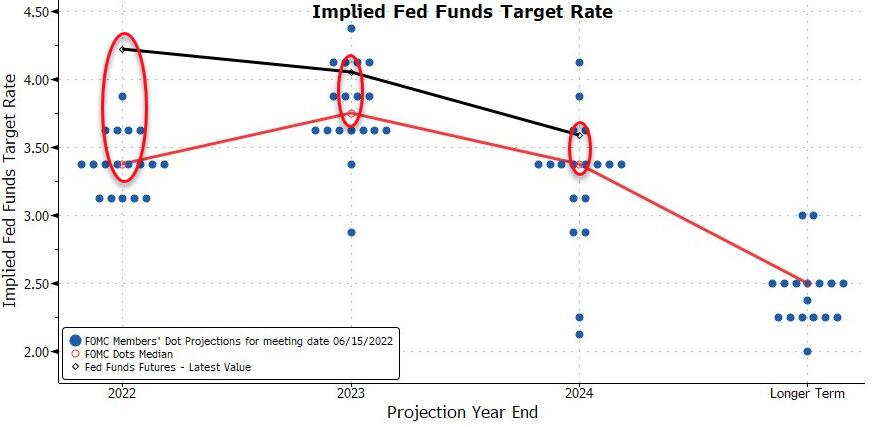

2. Dot plot & the terminal rate:

Market pricing since the release of those August inflation numbers has eclipsed the Fed’s June dot plot.

While the dot jigsaw plotted a rate of 3.80% next year, the markets have now priced in 4.50%.

{kind=link}

The latter is even higher than the most hawkish forecast made by a Fed member in the dot plot. The dot plot is in dire need of a fresh set of numbers — and traders will be keen to find out where the median lies beyond 2023 for clues on whether the Fed thinking is to “raise and cut” or to “raise and stay put.”

{kind=link}

Also of interest would be whether there is a shift in the Fed’s longer-run projection of its key rate. While the Fed insists that it has reached the neutral rate, evidence suggests that it may have been a touch overenthusiastic in making that claim. In other words, the theoretical equilibrium rate is higher — and it would take courage for the Fed’s dot plot to acknowledge that.

3. Economic projections:

We also get a revised outlook on how the Fed sees PCE inflation evolving, with an upward shift in the 2023 median likely. The monetary authority is likely to acknowledge a considerable increase in the unemployment rate both in 2023 and 2024 as tighter policy begins to bite.

The median forecast for US GDP growth next year is less than 1%. While it’s almost certain that the Fed will paint a more optimistic picture, there is little doubt that it will revise its outlook lower from the 1.7% expansion it estimated in June.

4. Powell-speak:

I expect the key takeaways from Chair Jerome Powell’s remarks to be two-fold: Sanctify the current market pricing as being broadly right; and reiterate that the Fed has made considerable progress in getting rates above the neutral rate, but that it is far from done.

Tyler Durden

Wed, 09/21/2022 – 08:00