42 Attorneys General Demand Surgeon General Warnings On Social Media In a move that's undoubtedly going to be used to...

Read More

Watch Live: What’s Next For Stocks As “Drained Puts” Reawaken Into $3.2 Trillion OpEx After CPI Shock

Ahead of this morning’s hotter-than-expected CPI print, the world and their pet rabbit was convinced – and chasing – that ‘peak inflation’ was here, The Fed would pivot, and stonks would continue to rip higher into a utopian soft-landing.

That has all gone to hell today as every asset class shits the bed in response…

{kind=link}

…as rate-hike expectations are smashed hawkishly higher and the odds of a subsequent recession soar.

{kind=link}

While most were ready for the face-ripping short-squeeze to continue their was one group offering some ‘what if’ warnings and actionable levels should shit go sideways from consensus.

SpotGamma wrote in a note early this morning that for this week: 9/16 is now a call weighted exp as opposed to puts.

Huge put positions were a key driver of the rally.

These 9/16 puts have now drained off. Over 4200 the rally loses steam as dealers shift from expanding vol to suppressing vol.

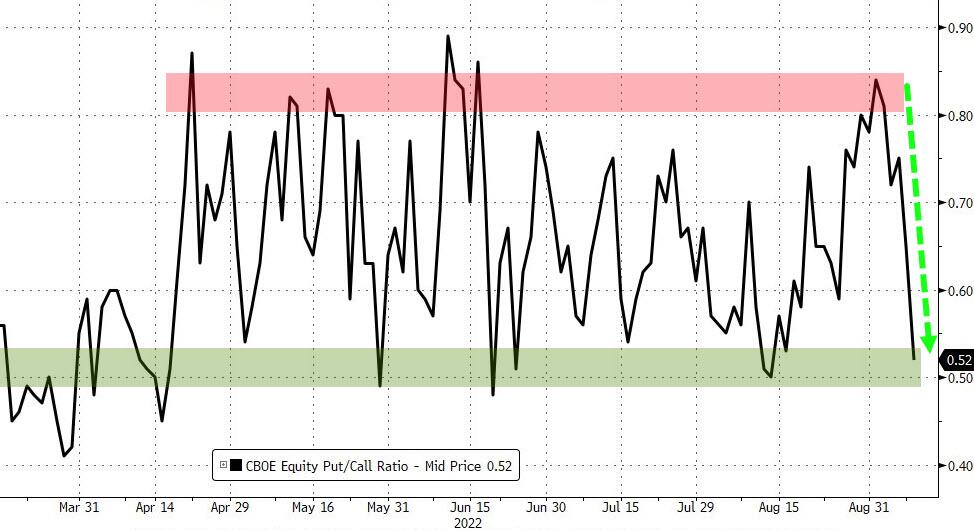

[ZH: As we detailed yesterday, the last couple of days has seen puts collapse relative to calls]

{kind=link}

A bad CPI could easily invoke 4000 as those “drained puts” reawaken.

As the adage goes – its not the number, but the reaction to the number that matters.

Options positioning is such that it will continue to support expanded volatility (i.e. bigger trading ranges), but this is most true to the downside.

First in regards to the downside.

A “bad” CPI print spikes IV & invokes negative gamma that spools up into OPEX. 9/16 put positions still exist, and while they are near worthless now, their pricing is “jumpy” and still potentially dangerous.

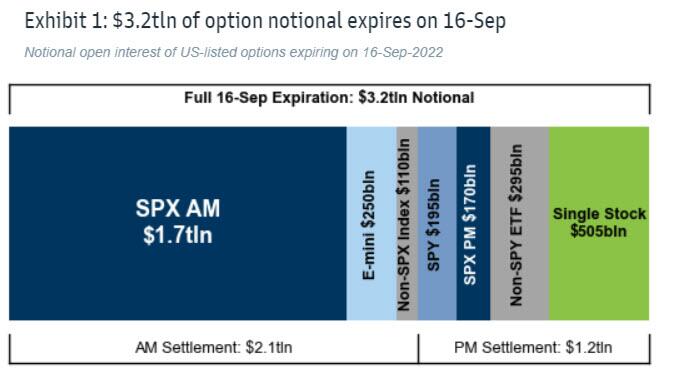

Notably, Friday’s expiration is larger than the last two Septembers, with the biggest concentration of SPX open interest is around the 4000 strike area.

{kind=link}

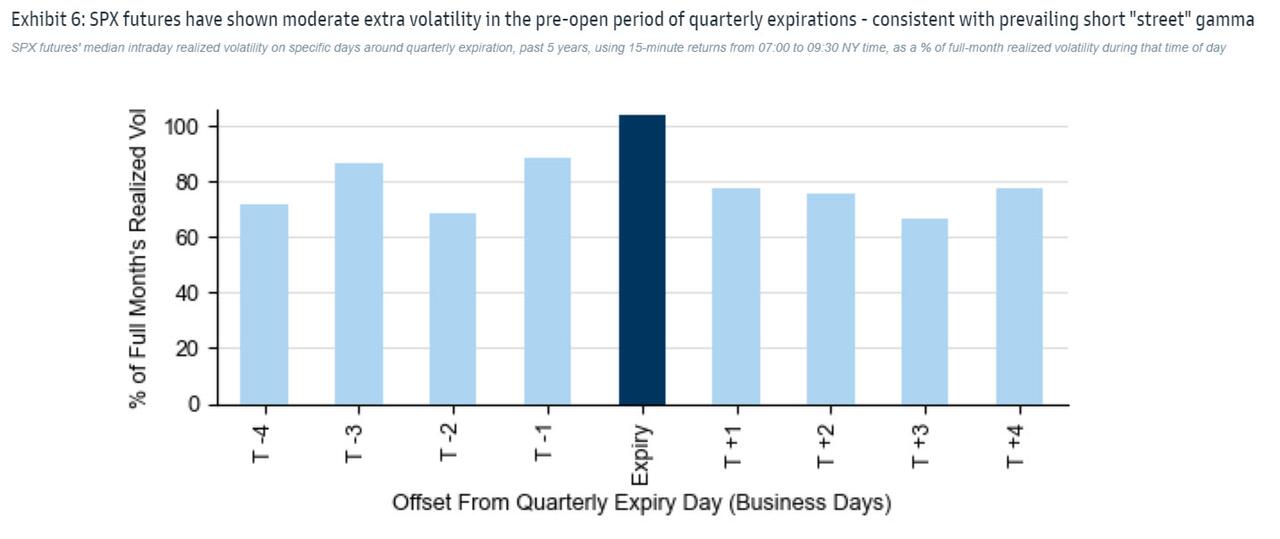

Additionally, Goldman’s Rocky Fishman notes that on recent quarterly expiration days, SPX futures have shown extra volatility prior to the cash market open.

{kind=link}

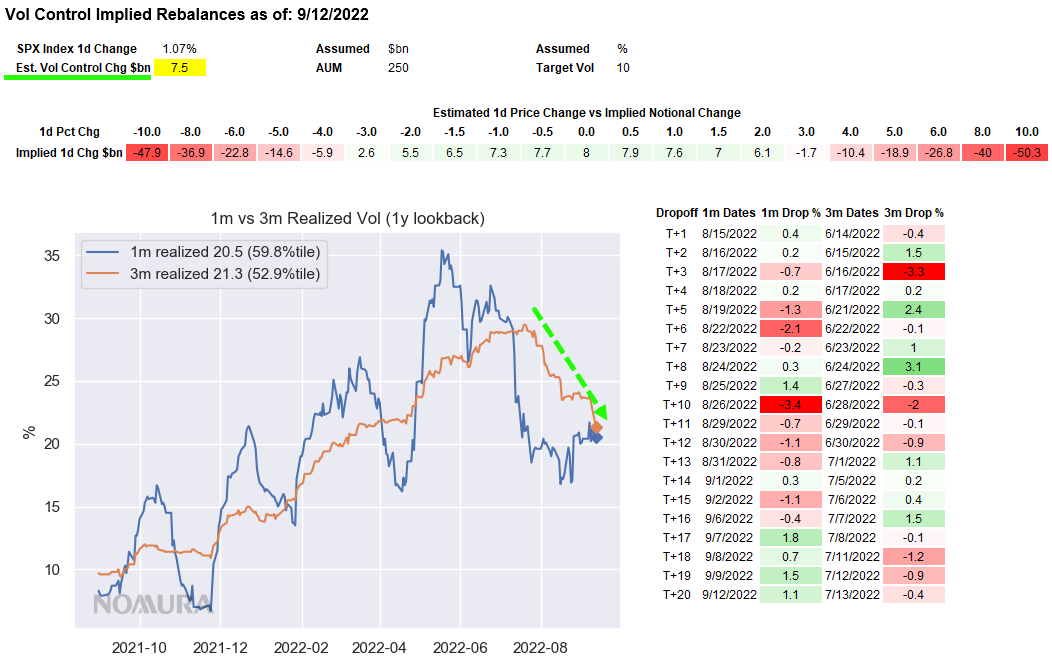

Finally, as if one needed another reason to worry, Nomura’s Charlie McElligott warned earlier that the post Sep Serial Op-Ex “window for Vol expansion” also gets interesting from the perspective of the Systematic and / or “passive” flows, because we are approaching the “cross” of 1m rVol (moving higher) above 3m rVol (moving lower), which could put a stop that Vol Control reallocate to BUY flow at the very least and even see potential to DE-allocate some of the recent reaccumulation of exposure (a not inconsequential +$33.5B over the past 3m)—and mind you, this would also sap a source of demand at the same time that the Corp buyback blackout will begin to accelerate into late September as well…

{kind=link}

In other words – Brace!

The S&P has broken below 4,000 and also back below its 50DMA…

{kind=link}

Watch SpotGamma’s detailed overview of how we got here today and what happens next (due to start at 1400ET):

Tyler Durden

Tue, 09/13/2022 – 13:56